Dividend Trends of Commercial Banks: Have the Golden Days Passed?

Mon, Jun 29, 2026 7:20 PM on Exclusive,

.png)

There was a time when investing in Nepal's stock market almost always meant holding commercial bank shares. With only a limited number of companies listed on NEPSE, commercial banks were considered the safest investment option due to strong regulatory oversight by the Nepal Rastra Bank (NRB), consistent financial performance, and promising prospects.

In addition, commercial banks had much smaller paid-up capital than they do today. As a result, even a modest increase in demand often led to significant price appreciation. These factors made commercial bank stocks one of the most preferred investment choices among all categories of investors.

Today, however, the situation has changed considerably. Commercial banks have become capital giants. Their growth appears to have stagnated, earnings capacity has gradually declined, and maintaining healthy financial indicators has become increasingly challenging.

So, where do commercial banks stand today compared to previous years in terms of shareholder returns? What do dividend trends indicate about the sector? Will the future remain the same, or is the banking industry undergoing a structural shift?

To answer these questions, we evaluate the dividend history of Nepal's commercial banks by categorizing them into three groups: a) Commercial banks that were later acquired by other banks; b) Commercial banks that merged and continue to operate as merged entities; and c) Existing commercial banks that continue to operate independently.

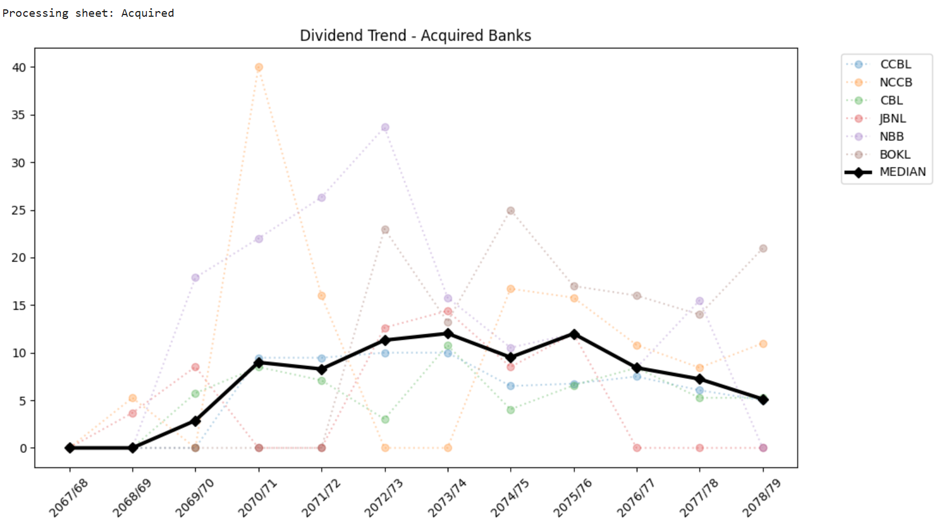

Acquired Commercial Banks

As part of the Nepal Rastra Bank's policy to promote mergers and acquisitions among Banks and Financial Institutions (BFIs), many institutions have lost their independent identities through acquisition. While some institutions have merged and continue to operate as new entities, others have been fully absorbed by larger banks.

To date, six Class 'A' commercial banks have been acquired:

- CCBL by PRVU

- NCCB by KBL

- CBL by HBL

- JBNL by GBIME

- NBB by NABIL

- BOKL by GBIME

This section examines the Class 'A' commercial banks that were eventually acquired and evaluates the returns they provided to shareholders during their independent operations. Before being acquired, none of these banks distributed dividends until fiscal year 2068/69. The first banks to declare dividends were Janata Bank Nepal Ltd. (JBNL) and Nepal Credit and Commerce Bank Ltd. (NCCB), distributing total dividends of 3.68 percent and 5.26 percent, respectively.

Collectively, these acquired banks distributed a median dividend of 2.87 percent in fiscal year 2069/70. Dividend distribution followed an increasing trend and reached its peak median value of 12.02 percent in fiscal year 2073/74. These banks maintained double-digit median dividend distributions for three consecutive fiscal years. However, dividend payouts began to decline from fiscal year 2075/76 onward. From fiscal year 2078/79, none of these banks distributed dividends as they had already undergone acquisition.

Among the acquired banks: BOKL recorded the highest median dividend at 17.00 percent. NBB followed with 15.79 percent. NCCB distributed a median dividend of 10.81 percent. CCBL recorded 7.50 percent. CBL distributed 6.16 percent. These figures represent the median dividend distributed throughout each bank's dividend-paying history.

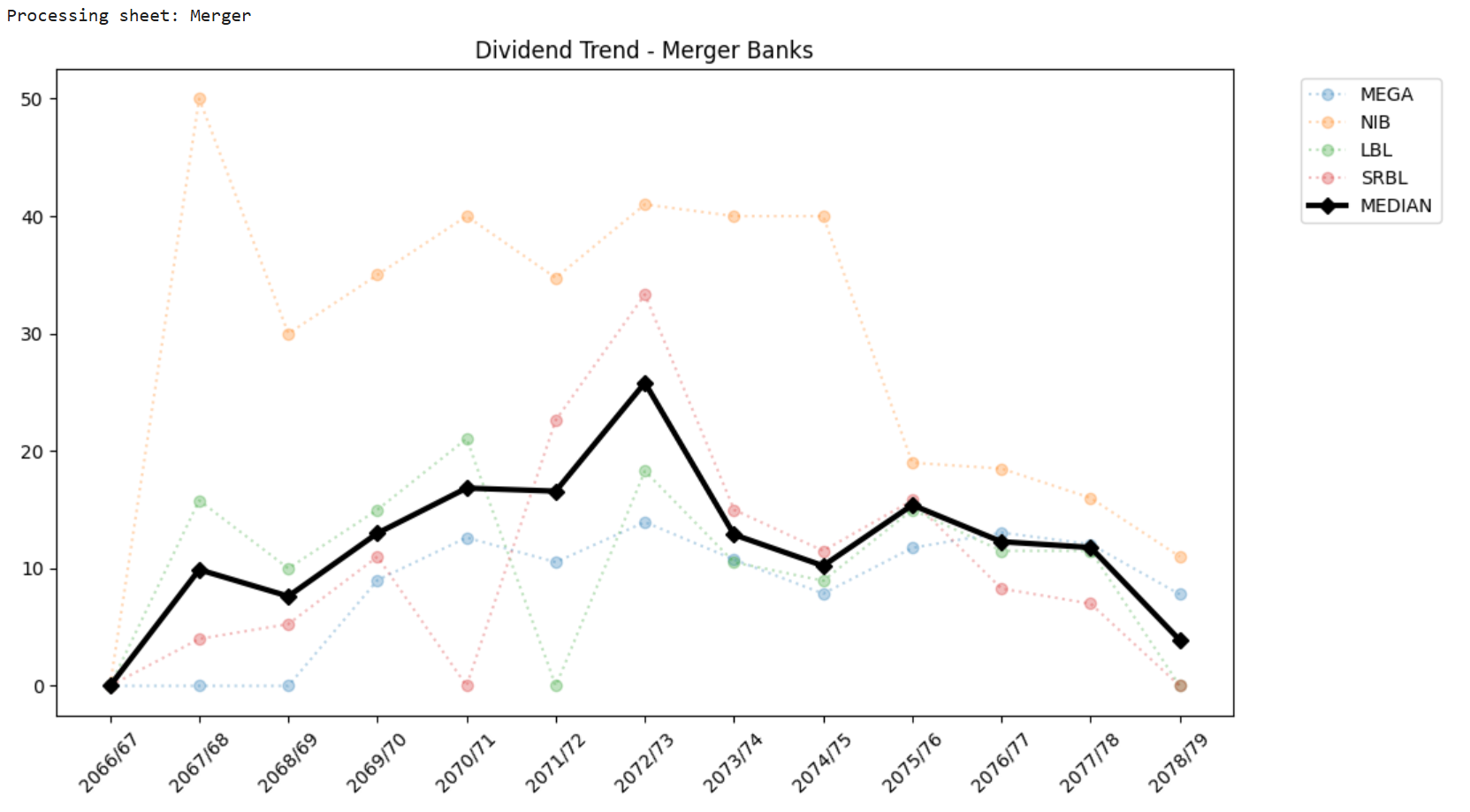

Merged Banks

Among Nepal's commercial banks, four banks underwent mergers, resulting in two surviving merged entities. Mega Bank Nepal Ltd. (MEGA) and Nepal Investment Bank Ltd. (NIB) merged to form Nepal Investment Mega Bank Ltd. (NIMB). Laxmi Bank Ltd. (LBL) and Sunrise Bank Ltd. (SRBL) merged to form Laxmi Sunrise Bank Ltd. (LSL).

This section evaluates the dividend performance of these banks before their mergers. Among them, NIB was the strongest dividend provider. Between fiscal years 2067/68 and 2078/79, it distributed a median dividend of 34.87 percent, making it one of the most sought-after banking stocks during that period.

Similarly, LBL distributed a median dividend of 11.50 percent, MEGA distributed 11.25 percent, and SRBL distributed 9.64 percent.

A longitudinal analysis of dividend distributions shows that merged banks consistently maintained stronger dividend performance than acquired banks. Out of the twelve fiscal years observed, these banks distributed double-digit dividends in more than nine fiscal years. In fiscal year 2072/73, the median dividend exceeded 25 percent.

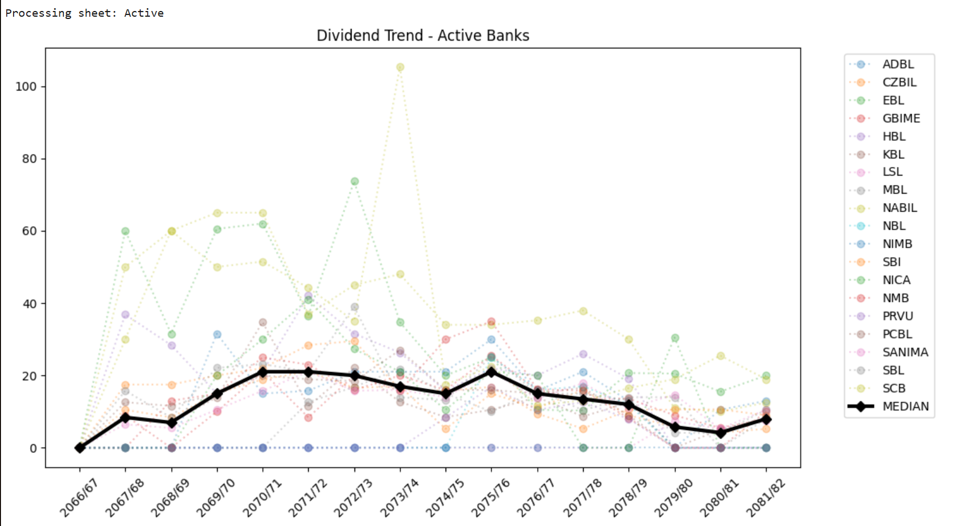

Active Banks

Based on the dividend distribution history, there is still no reason to be overly pessimistic about Nepal's commercial banking sector. Although the business of Class 'A' commercial banks has become increasingly saturated, the sector continues to offer opportunities through innovative banking products and services. In terms of customer enrollment, the total number of savings accounts held by Class 'A' banks is already more than twice Nepal's population, indicating that future growth through traditional customer acquisition is becoming increasingly limited.

Looking at the past 15 years of dividend history, Class 'A' commercial banks have consistently rewarded shareholders with attractive returns. Most banks have distributed dividends in double digits, particularly above 15 percent, over the period. On an individual bank basis, NABIL ranks first in terms of dividend distribution. From its first dividend declaration to the latest fiscal year, it has distributed a median dividend of 35.26 percent. It is followed by SCB, with a median dividend of 25.50 percent, while EBL ranks third with 25.00 percent. HBL holds the fourth position, with a median dividend of 21.05 percent. At the lower end of the spectrum, the newly formed merged banks LSL and PRVU have distributed median dividends of only 7.37 percent and 8.21 percent, respectively. All remaining commercial banks have maintained median dividend distributions in double digits, exceeding 10 percent.

Conclusion

Based on the historical dividend analysis, the banks that entered mergers were fundamentally strong institutions. Their dividend records justify their financial strength and support the rationale for co-existence through mergers. However, the post-merger performance has not yet matched investors' earlier expectations.

Increasingly stringent regulatory requirements have made it more challenging for commercial banks to generate higher profits despite mobilizing large volumes of deposits and taking on greater operational risks.

Sadly, mergers and acquisitions are expected to generate better results through synergy. However, based on dividend trends, the anticipated benefits have yet to materialize. Banks that have not undergone major mergers or acquisitions appear to have performed better and have delivered comparatively higher returns to their shareholders.

Nepal Rastra Bank's policy of maintaining lower interest rates, controlling the base rate, stabilizing market interest rates, and narrowing the interest spread has further limited banks' earnings capacity.

As a result, BFIs and their stakeholders need to rethink their business models and explore new strategies to maximize value for shareholders while supporting sustainable economic growth.

Looking ahead with optimism, major economic developments across key sectors could significantly improve banks' performance. If nation experiences stronger economic expansion in the coming years, the banking sector may once again deliver remarkable results. Hopefully, that better period is not too far away.