Which microfinance is in which position? A comparative study!

Tue, Nov 27, 2018 12:50 PM on Exclusive, Stock Market,

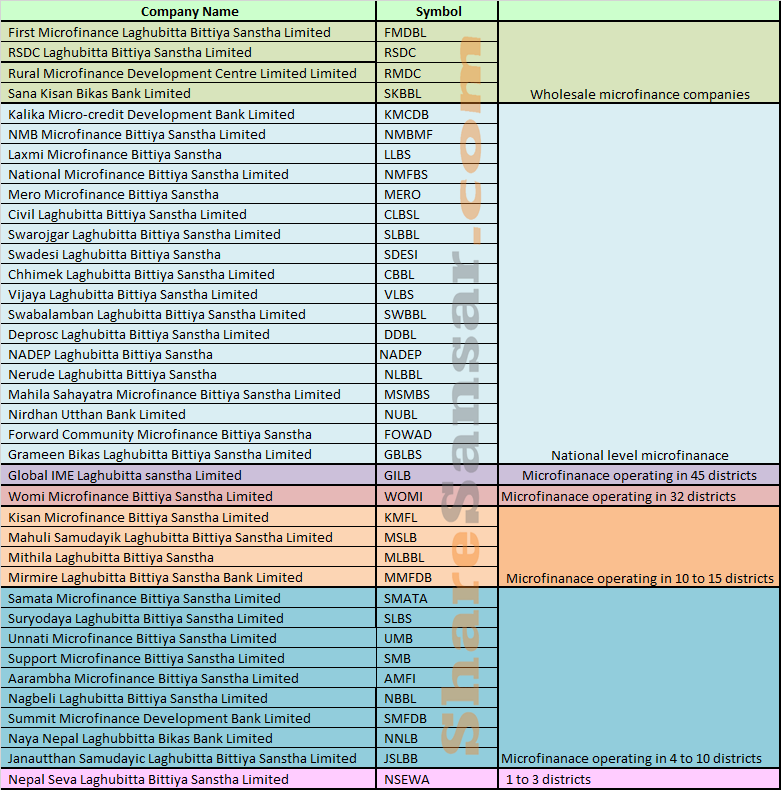

In a developing country like Nepal, where majority of population still lacks a proper access to finance, microfinance and co-operatives have been designed to fulfill the need of such population. In Nepal, there are 66 microfinance companies in operation. Out of these, 38 microfinance institutes are listed. The objective of microfinance institute of the country is to provide access of finance to the bankable poor and entrepreneurial poor. However, the dark side of microfinance sector in Nepal lies on the fact that most of these remain concentrated in urban areas of the country.

The majority of microfinance institutes have published their first quarter report as of 2075/76. The overall analysis of majority of indicators such as paid up capital, reserve and surplus, net profit, earning per share (EPS), PE ratio, Net worth per share, promotes investor’s understandings on performance assessment of these microfinance units.

The further analysis focuses only on the 38 listed microfinance institutes. The non-listed microfinance institutes are not compared with the listed microfinance institutes.

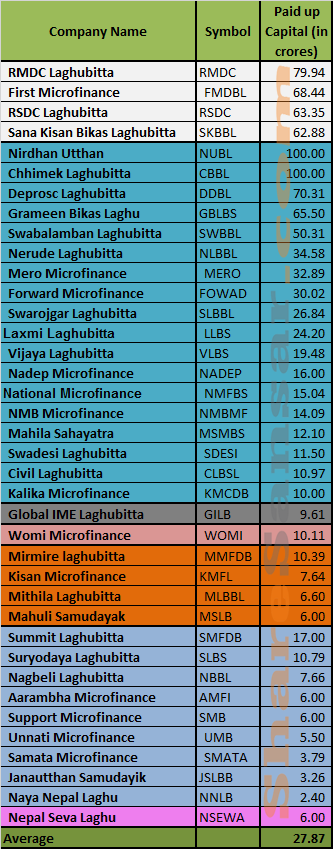

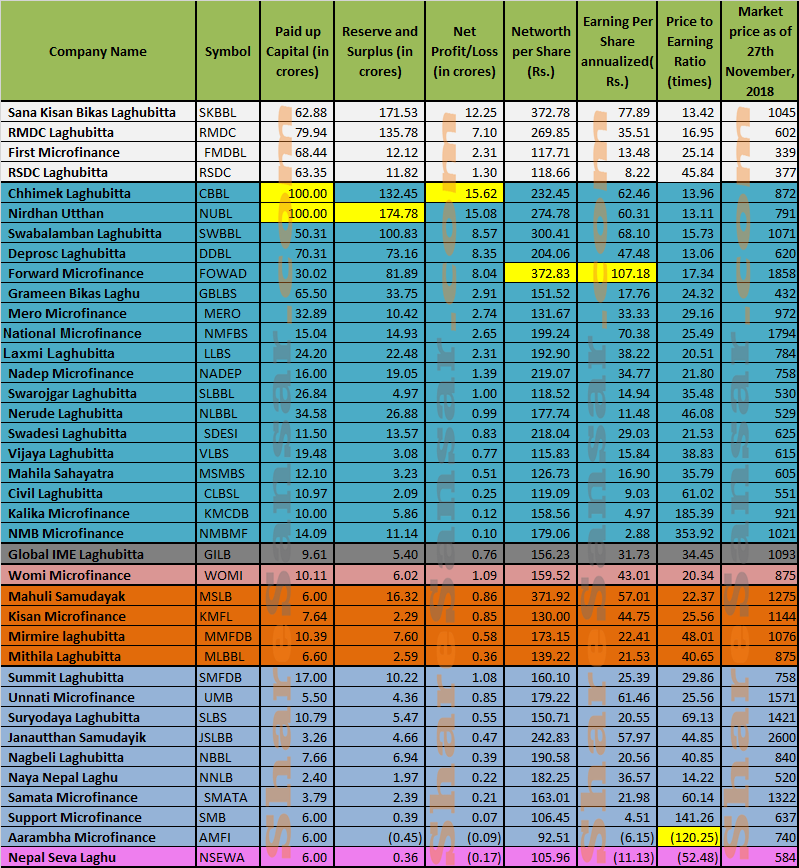

Paid-up capital: The central bank has directed national level, regional level and district level microfinance institutes to increase their paid up capital requirement. The wholesale level microfinance should meet the paid up capital of Rs 600 million. The national level microfinance institutes should have the paid up capital of Rs 100 million, regional level microfinance of Rs 60 million and finally, district level microfinance of Rs 10 million. The average paid up capital is Rs 27.29 crores. The microfinance institutes with highest paid up capital are:

- Chhimek Laghubitta Bittiya Sanstha Limited (CBBL) with a paid up capital worth Rs 1 arba

- Nirdhan Utthan Laghubitta Bittiya Sanstha Limited (NUBL) with a paid up capital worth Rs 1 arba

- RMDC Limited (RMDC) with a paid up capital worth Rs 79.94 crore

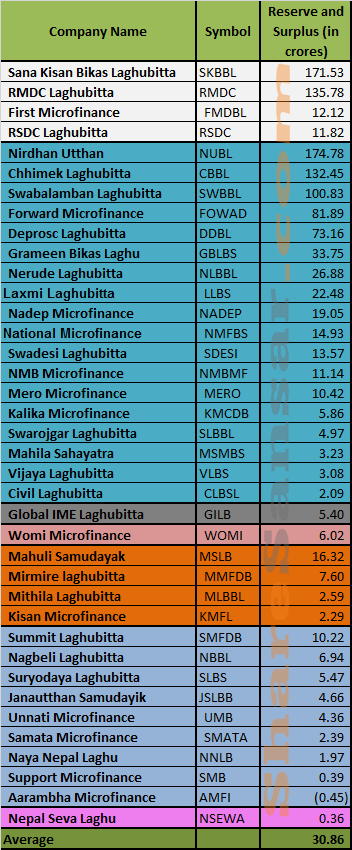

Reserve and surplus: The microfinance institutes are required to serve the riskiest category of the country. So, a reserve and surplus can be useful at times of crisis. The average reserve of the industry is Rs 30.06 crores. The microfinance institutes with highest amount of reserve fund are as follows:

- Nirdhan Utthan Bank Limited with a reserve of Rs 1.74 arba

- Sana Kisan Bikas Bank Limited (SKBBL) with a reserve of Rs 1.71 arba

- RMDC Laghubitta with a reserve of Rs 1.35 arba

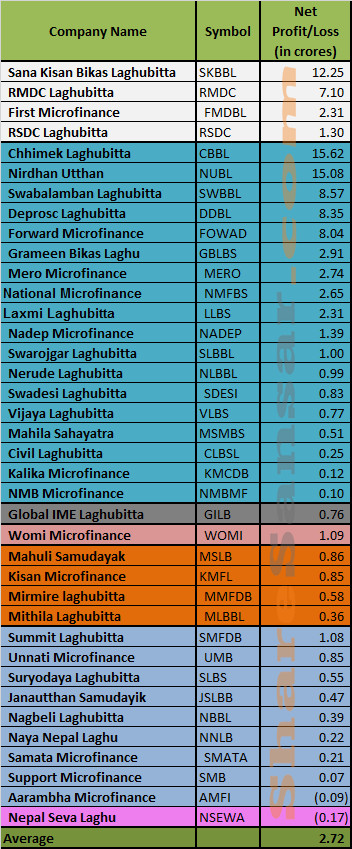

Net Profit: As of the first quarter report of FY 2075/76, the listed microfinance institutes with the highest net profit are:

- Chhimek Laghubitta Bittiya Sanstha Limited (CBBL) with a net profit of Rs 15.62 crores

- Nirdhan Utthan Bank Limited (NUBL) with a net profit of Rs 15.08 crores

- Sana Kisan Bikas Bank Limited (SKBBL) with a net profit of Rs 12.25 crores

The average net profit is Rs 2.72 crores of the overall industry. Nine microfinance institutes are above the average net profit.

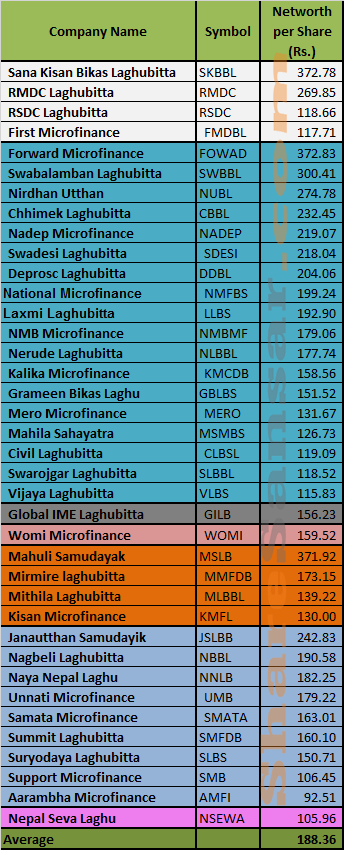

Net worth per share: Net worth per share is acritical tool to identify the worth of a company. The microfinance institutes with the highest net worth per share are as follows:

- Forward Community Microfinance Bittiya Sanstha (FOWAD) with a net worth of Rs 372.83

- Sana Kisan Bikas Bank Limited (SKBBL) with a net worth of Rs 372.78

- Mahuli Samudayak (MSLB) with a net worth of Rs 371.92

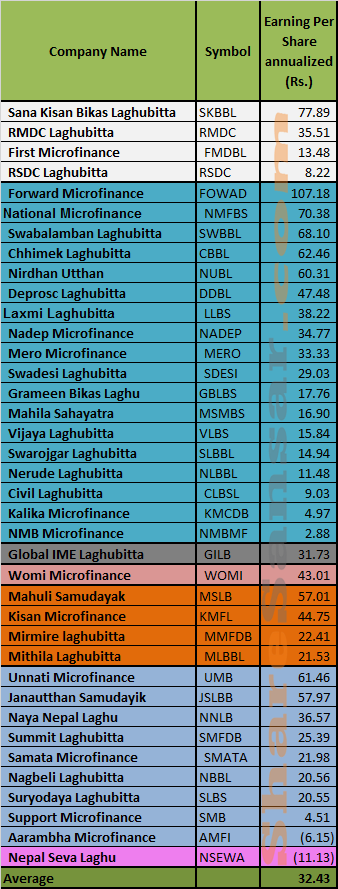

Earnings per share: The increment of paid up capital has influenced the EPS of majority of microfinance institutes. The industry average EPS stands at Rs 32.43. The microfinance institutes with highest level of EPS are:

- Forward Community Microfinance Bittiya Sanstha (FOWAD) with an EPS of Rs 107.18.

- Sana Kisan Bikas Laghubbita (SKBBL) with an EPS of Rs 77.89

- National Microfinance (NMFBS) with an EPS of Rs 70.38

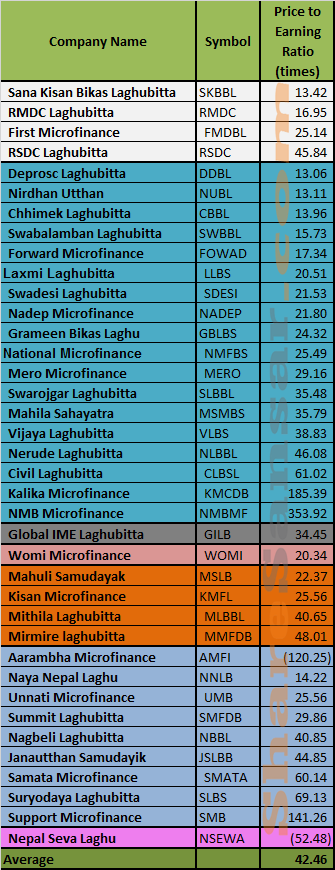

PE ratio: The general rule of thumb in finance believes the least PE ratio is better for investors. So, following the general rule, the microfinance institutes with least PE ratio are:

- Deprocs Laghubitta (DDBL) with PE of 13.06 times

- Nirdhan Utthan Laghubiita (NUBL) with a PE ratio of 13.11 times

- Sana Kishan Bikas Laghubitta (SKBBL) with a PE ratio os 13.42 times.

The industry average p/e ratio is 42.46 times.

In a nutshell:

The microfinance institutes have to face a trade off when it comes to their profitability and outreach to the bankable poor. Dear readers, do you think microfinance institutes in Nepal have the capability to develop innovative products for the bankable poor? Why do you think many people in rural areas still lack access to finance although the microfinance industry is rapidly mushrooming? Please write your opinions in the comment section below.

(Disclaimer: Any kind of information that is provided in the article should not be used as a sole advice or recommendation by investors in order to design their investment portfolio. So, before taking steps for any kind of the information, the investors are required to base their judgment on their own financial analysis, appropriateness of the information and seek independent financial advice. The information of the company has been taken from the authorized sources such as website of the company, NEPSE, financial reports and press releases of the companies so, any changes not updated in these may differ in the analysis.)