What is the absolute gain or loss of your investment? Look at the secondary market performance of commercial banks post revelation of capital increment

Mon, Dec 10, 2018 1:16 PM on Exclusive, Stock Market,

~Rishab Agrawal

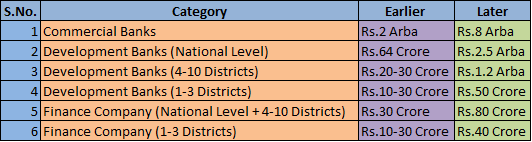

On 23rd July, 2015, Governor Dr. Chiranjibi Nepal announced the new monetary policy for the FY 2072/73. The policy contained regulations regarding the minimum capital requirement of Banks and Financial Institutions. This came as a surprise as only a handful of people knew about the new capital requirement. Although, this provision was to encourage BFI’s to go for merger and acquisitions, it didn’t work out as planned for A class commercial banks and BFI’s started distributing huge amounts of bonus and rights to meet the minimum paid up capital requirement. Since then, bonus and rights of BFI’s have influenced the securities market. After the revelation of the new policy, the market started absorbing the effects and after effects of the announcement.

Over the period since, NEPSE has behaved in different ways including hitting the all-time high of 1881 points from 960 index levels in a little over a year time period. NEPSE has gained and lost points, but what have the investors actually gained? Are they gaining or losing compared to the prices of shares after the revelation of the monetary policy and the all-time high closing prices? We are about to find out.

For the purpose of uniformity in comparison, the effects of right shares on the prices of the shares since the FY 2072/73 and bonus shares since FY 2071/72 have been nulled as per their book closures, as the new monetary policy was announced for FY 72/73 and bonus shares of FY 71/72 were due after that period. This was done by adding back the bonus and right adjustment to the share prices in order to have uniform comparison with share prices after the new monetary policy and the all-time high share prices. This kind of analysis is effective as it shows the actual gain or loss of an investor irrespective of the bonus shares or right shares offered.

The purpose of this article is to clear the picture regarding absolute gain or loss in commercial banks for investors who had invested in commercial banks in that period and are holding their investment since. The anticipation of bonus and rights since the mentioned period took the market to a new level of high, however, bonus and rights don’t always lead to appreciation in the prices of shares.

For example:

The LTP of Sunrise Bank (SRBL) as on 5th December 2018 is Rs.217 per share. Now, the bank had proposed bonus share of 15% and right share of 30% for FY 73/74, bonus share of 33.33% and right share of 15% for FY 72/73 and bonus share of 21.50% for FY 71/72. To achieve the unadjusted price, we add back the bonus and rights adjustment to the current price of the share as per their book closures:

15% bonus of FY 73/74: 217 + (15%*217) = 249.55

30% rights of FY 73/74: 249.55 + (30%*249.55) – 30 = 294.42

33.33% bonus of FY 72/73: 294.42 + (33.33%*294.42) = 392.55

15% rights of FY 72/73: 392.55 + (15%*392.55) – 15 = 436.43

21.50% bonus of FY 71/72: 436.43 + (21.50%*436.43) = 530.26

Hence, Rs.530.26 is the current unadjusted price of sunrise bank.

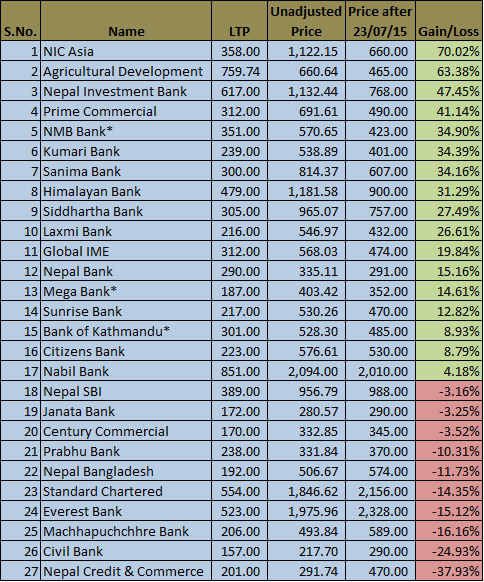

Similarly, the unadjusted prices of all the commercial banks have been calculated to know the actual gain or loss per share of an investor in commercial banks sector. First, we compare the current unadjusted prices of commercial banks with the prices right after the revelation of the monetary policy.

(*These banks were in the process of merger during that period due to which trading was suspended. Price mentioned has been calculated accordingly)

The unadjusted prices have been calculated on the basis of the share prices of 5th December 2018. As we can see, only 17 out of 27 listed commercial banks have gained since, gaining from 4% to 70%. As per comparison with unadjusted current price, NIC Asia Bank, Agricultural Development Bank and Nepal Investment Bank are the top three gainers since the mentioned period. Similarly, Machhapuchchhre Bank, Civil Bank and Nepal Credit and Commerce Bank have lost the most in this period with losses ranging from 3% to almost 40%.

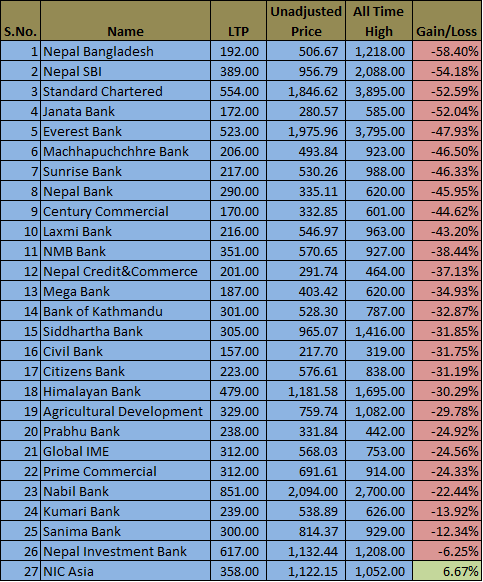

The unadjusted prices have also been compared with all-time high prices of shares from 23rd July, 2015 (Last Traded Price just before revelation of 2072/73 FY monetary policy to increase paid up capital of BFI’s) until 5th December, 2018 to know the extent of the actual gain or loss of an investor.

On comparison of unadjusted prices with the all-time high closing prices, the loss ranges from 6% to almost 60%, while only NIC Asia has showed a gain of 6.67%. That means if an investor had invested in commercial banks during that period, they would probably have lost at least 6.25% irrespective of the bonus share rewarded and right shares applied. Nepal Bangladesh Bank lost the most since that period, the actual loss standing at 58.40%.

Hence, from the analysis above we can say that most of the commercial bank investors had to deal with losses if they had invested during the mentioned period. Although, years have passed since the mentioned period, still minimal appreciation and depreciation in value of investment had to be realized by the investors. This is the true state of commercial bank investments in a market that considers investment in commercial banks to be a safe bet. Although, such massive fall in the share prices of commercial banks could be the correct time for new investors to enter the market and existing investors to redistribute their current portfolios.