Nabil Balanced Fund II opens from today; If you haven't applied yet, things to know before you do

Thu, Apr 18, 2019 4:48 PM on Exclusive, Mutual Fund, Stock Market,

Company profile

Nabil Balanced Fund II is a close-end mutual fund scheme with a corpus of Rs 1.2 arba for a period of 10 years. It being sponsored by Nabil Bank Limited and managed by Nabil Investment Banking Limited. Nabil Bank is "A" Class commercial bank. It was registered in 2041 BS under Company Registrar as a Public Limited Company. The promoters hold 70% of shares and the remaining 30% is floated to general public. It started commercial operations from July 1984 AD as Nepal Arab Bank Limited but the name was changed to Nabil Bank, following the withdrawal of its joint venture partner Emirates Bank International in 1997.

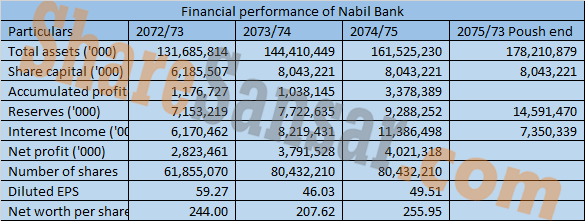

As per the report published by ICRA Nepal, Nabil has its presence throughout the country through its 74 branches, two extension counters and 126 ATMs. It has a market share of 5.65% in terms of deposit base and 5.54% of its total advances is in the Nepalese commercial banking industry, as on mid-Oct-2018. Nabil reported a profit after tax of ~NPR 4,055 million during 2017-18 over an asset base of NPR 157,486 million as of mid-July-2018.

Similarly, Nabil Invest is the subsidiary merchant bank of Nabil whose 52% ownership lies with Nabil Bank. It was registered under Company Act 2063 on 2066 BS. The various services provided by Nabil Invest are issue management, underwriting, share registrar, investment management and financial consultancy services. The company is also licensed to function as Mutual fund scheme manager and Depository since 2069 BS.

About the issue

Nabil Balance Fund II, managed by Nabil Investment Banking Limited and sponsored by Nabil Bank Limited is floating its public issue of 12 crore units mutual fund scheme worth Rs 1.2 arba from today (Baisakh 5, 2076). The mutual fund will be issuing a total of 12 crore unit of ordinary shares worth Rs 1.20 arba at face value of Rs 10 per unit.

Interested people must apply for a minimum of 100 units of share and they can apply for up to 1.2 crore units. Interested applicants can apply through ASBA-approved banks from all 77 districts across the country.

Nabil Balance Fund II is the Nabil Investment Banking Limited third mutual fund scheme, and is a 10-years closed-end fund. The scheme will be managed by Nabil Investment Banking Limited with Nabil Bank Limited as the fund sponsor. Under the current mutual fund regulation, 15% units i.e. 1.80 crore units are reserved for fund manager and fund sponsor. Remaining 10.20 crore units will be floated to the general public.

Dividend Payout

The dividend will be paid out of realized profits in proportion to investments made. The Retained Earnings (if any) will be re-invested.

Investment objective

To generate optimum returns by minimizing market risks by investing in a mix of securities comprising of equity and fixed income securities as allowed by prevailing rules/regulations on Mutual Fund.

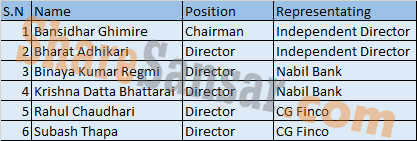

Supervisors of NBF II

The general asset allocation of the proposed Scheme's portfolio

Capital structure of Nabil Invest

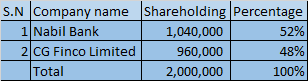

Shareholding structure of Nabil Invest

Board of Directors of Nabil Invest

Management team of Nabil Invest

Areas of investments

- Securities that are registered with SEBON

- Securities called for public offering

- Securities that are listed in NEPSE

- Debentures, Treasury Bills and other instruments of money market issued by Government of Nepal or Government Agencies receiving full guarantee or protection of GoN or NRB

- Bank deposits

- Money Market Instruments

- Other areas as prescribed by SEBON

ICRA Rating of Nabil Bank

ICRA Nepal has reaffirmed the rating of [ICRANP-IR] AA- (pronounced ICRA NP Issuer Rating Double A minus) to Nabil Bank Limited (Nabil). The entities with [ICRANP-IR] AA- rating are considered as high credit-quality ratings assigned by ICRA Nepal. The rated entity carries a low credit risk. The rating is only an opinion on the general creditworthiness of the rated entity and not specific to any particular debt instrument.

The rating reaffirmation factors in Nabil’s ability to maintain its competitive positioning in the industry; as reflected in the steady performance indicators of the bank. The bank’s strong competitive positioning coupled with its established track record and adequate presence across the country continues to support business growth and profitability.

Nonetheless, the rating concerns arise from the recent liquidity challenges faced by the Nepalese banking industry, including Nabil, because of higher growth in banking sector credit vis-à-vis deposit during the past four to five years. As a result, Nabil’s liquidity ratio has come down, with commensurate increase in the credit-to-deposit ratio. A higher credit-to-deposit ratio has helped Nabil offset the impact of the rising cost of fund, thereby stabilising net interest margin (NIMs) and supporting profitability.

Nabil’s average credit growth during the past three years, ending FY2018 stood at 19%, lower than the industry average of 24% over the period. Nabil’s credit growth has picked up during past 12-18 months (23% during FY2018 and 46% annualised during Q1 FY2019), leading to a marginal improvement in market share. Nabil’s credit portfolio of ~NPR 125 billion as of mid-October 2018, accounted for ~4.8% of Nepalese banking industry credit (vs. ~4.5% in mid-April 2017, when last rated).

Going forward, the low cost of fund and consequent pricing advantage under the ‘Base Rate plus’ regime is expected to support Nabil’s plan to penetrate along the SME and the retail segment. However, its ability to achieve the targeted SME and retail segment growth with relatively moderate franchise network across the country remains to be seen.

Nabil’s asset quality indicators have improved during the past 12-18 months, aided by interim credit growth, low fresh NPA generation rate and steady NPA recovery rate.

Nabil’s deposit profile has been affected by the liquidity shortage seen in the banking system since January 2017. The deposit price-war among the industry players (especially in the term deposits) has led to the decline in the CASA deposits for Nabil (from ~60% in mid-July 2017 to ~48% in mid-July 2018) with a corresponding increase in higher priced term deposits.

Nabil’s liquidity position has moderated during the past one to two years because of the ongoing shortage of lendable funds. Nabil’s liquid assets as a percentage of total liabilities stood at ~22% on mid-October 2018 vs. ~26% in mid-July 2018 and ~33% on mid-July 2017.

Nabil’s profitability indicators continue to remain strong because of healthy NIMs (~4% during past 12-18 months). The increase in credit to deposit ratio of the bank has helped maintain stable NIMs, offsetting the impact of rising cost of fund. Nabil’s return on assets during FY2018 stood at ~2.7% (similar to FY2017) with a return on net worth of ~25% and ~28% during those periods. Nabil’s profitability also remains supported by a healthy non-interest income level (~1.35% of ATA during FY2018), low operating expense ratio and low credit cost.

Source: (https://icranepal.com/releases.php)

ICRA Rating of Nabil Invest

ICRA Nepal has reaffirmed “[ICRANP] AMC Quality 3+ (AMC3+)” (pronounced ICRA NP Asset Management Company Quality Three Plus) fund management quality rating (FMQR) assigned to Nabil Investment Banking Limited (Nabil Invest), indicating adequate assurance on management quality.

The adequate assurance on management quality factors in the ownership and continued technical support of Nabil Bank Limited along with established organisational structure, system and processes for current level of operations. The FMQR also factors in satisfactory investor service practices of Nabil Invest & the processes followed by it in generating healthy returns for first scheme managed by it while the second scheme has remained impacted by significant downturn in market index since its launch. The rating action also derives comfort from experienced senior management and fund supervisors involved in the management and supervision of the current mutual fund schemes under the company. However, the requisite extent of involvement of supervisors in managing the schemes is not clearly mandated by strong legal framework and hence remains a rating concern.

The FMQR is nonetheless constrained by the divestment of a chunk of stake by Nabil Bank (from ~74% earlier to 52% as of now with concomitant increase in stake of CG Finco); however, extent of support from the sponsor has remained similar which provides some comfort. The rating is also constrained by the company’s moderate track record in Nepalese Capital market as merchant banker, portfolio manager and fund manager along with uncertain operating environment amidst volatility in the market, evolving risk management framework with respect to fund management, absence of separate risk management committee, unviability of hedging tools for investment in the market, evolving nature of mutual fund industry and low awareness about the mutual fund among general investor.

Source: (https://icranepal.com/releases.php)

Financial performance of Nabil Bank

Financial performance of Nabil Invest

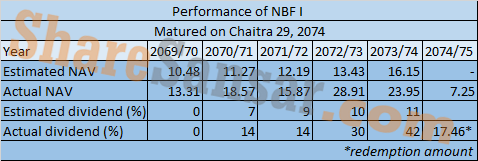

Performance of Nabil Balanced Fund I (NBF I)

Nabil Balance Fund-1 was a closed end 5 years mutual fund scheme of Rs 75 crore managed by Nabil Investment Banking Limited and sponsored by Nabil Bank Limited. The mutual fund scheme was started on Chaitra 30, 2069 and matured on Chaitra 29, 2074.

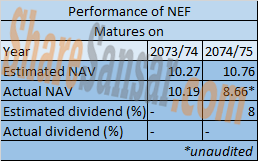

Performance of Nabil Equity Fund (NEF)

Nabil Equity Fund (NEF), a closed-end 7 years mutual fund scheme managed by Nabil Investment Limited with Nabil Bank Limited as the fund sponsor. The fund began with a corpus of Rs 1.25 arba.

Projected performance of NBF II on major indicators

Conclusion

All the information stated above might have shed some light on what to expect from NBF II. The issue has opened from Baisakh 05, 2076 (today) and interested investors can apply from any C-ASBA approved banks or Mero Share.

Based on the previously managed Mutual Funds Schemes, Nabil Invest has given more than fair return to NBF I but the ongoing NEF's performance is not so good. The internal factor are surely there, but a huge factor is MARKET RISK. NBF I operated from 2069 to 2074, so it got to see the bull of 1800. However, the market is in bearish trend now, because of which not only NEF but almost all of 13 mutual funds are having a hard time increasing their NAV to par of Rs 10.

Many experts say, now the bull is near and some say the bear will last some more and everyone and a reasoning about what and how they are estimating. Thus, the projected returns of NBF II is given in earlier section now you have the decision to make whether or not to invest.