Mutual Fund- A Boon Or A Bane In Nepalese Context

Wed, Nov 8, 2023 9:46 AM on Exclusive, Mutual Fund, Stock Market, Featured,

A mutual fund is a financial intermediary that pools the savings of investors for collective investments in a diversified portfolio of securities. A fund is said to be mutual as all of its returns, minus its expenses are shared by the fund investors. A mutual fund serves as a link between the investor and the securities market by mobilizing savings from the investors and investing them in the securities market so as to generate returns. Thus, a mutual fund is a kin to Portfolio Management Services (PMS). The government of Nepal has made mandatory provisions to allocate 5% of the total initial public offerings(IPO) for mutual funds. The mutual fund plays a vital role in the securities market and has its own importance/benefits.

Mutual funds in Nepal are a relatively new investment option, but they have quickly become popular among investors. Some of the major reasons for this include Professional management, Portfolio Diversification, Reduction in transaction costs, transparency, affordability, liquidity, Convenience and flexibility, and so on.

- Professional management:

An average investor lacks the knowledge of capital market operations and doesn't have large resources to reap the benefits of investment. Hence, one requires the help of an expert. It is not only expensive to “hire the services of an expert” but much more difficult to identify the real expert. Mutual funds are managed by professional managers who have the requisite skills, knowledge, and experience to analyze the performance and prospectus of companies. They make possible an organized investment strategy, which is hardly possible for an individual investor.

- Portfolio Diversification:

An investor undertakes risks if one invests all of his funds in a single script. Mutual fund invests in a number of companies across various industries and sectors. This diversification reduces the riskiness of the investments. One doesn't invest in a mutual fund but rather invests through a mutual fund. Thus one can invest in diversified sectors with a small fund as low as Rs.1000, where s/he gets 100Units of Face Value Rs.10.

- Reduction in transaction costs:

Compared to direct investing in the capital market, investing through mutual funds is relatively less expensive as the benefits of economies of scale are passed onto the investors.

- Liquidity:

Often, investors cannot sell the securities held easily, while in the case of mutual funds, they can easily encash their investment by selling their units to the fund if it is an open-handed scheme or selling them on a stock exchange if it is a close-ended scheme.

- Convenience:

Investing in mutual funds reduces paperwork, saves time, and makes investment easy.

- Transparency:

Mutual funds are highly regulated and transparent investments. Investors can easily track detailed information about the fund's holdings, performances, and fees. Performances can be easily traced through their NAV(Net Assets Value). NAV per share can be obtained by dividing net assets( total market value of assets minus liability ) by the number of shares or units outstanding.

Besides this, there are also some challenges associated with mutual fund investing in Nepal. Some are discussed below:-

- Lack of awareness:

Investors in Nepal are not aware of mutual funds or the benefits they offer. One of the major reasons behind this is the lack of knowledge and training classes that are provided by the merchant bankers, especially for mutual funds. Even today, the majority of the classes seem to run only inside the Kathmandu Valley.

- Limited investment options:

The number of mutual funds available in Nepal is still very limited. Currently, there are 7 open-ended schemes and 35 close-ended schemes.

- High fees:-

Mutual funds charge high fees, which reduces the investors' overall returns. One of the major reasons behind this is to high costs involved. Investors incur several costs when they invest their money through mutual funds such as:- load charges, management fees, 12B-1 fees, transaction costs, accounting, and other miscellaneous costs.

- Risks:

A popular saying “Mutual Fund investments are subject to market risks, read all scheme-related documents carefully”. The NAVs of the schemes may go up or down depending upon the factors and forces affecting the securities market including the fluctuations in the interest rates. The past performance of the mutual funds is not necessarily indicative of the future performance of the schemes.

History of Mutual Funds in Nepal

Mutual funds work by pooling money together from many investors. That money then gets used to purchase stocks, bonds, and other securities. Because mutual funds invest in a collection of companies, they offer instant diversification (thus lower risk) to investors.

With the flotation of the NCM mutual fund in 2050 B.S. (1993A.D.), the Nepali financial market entered into a new era of mutual funds. It was an open-ended scheme with a collected fund of just Rs. 100 million. These days, merchant bankers are coming up with funds 5 to 10 times larger than that, which have become a pivot part of the Nepalese financial market. In Nepal, NCM mutual fund 2050 was established by NIDC Capital market as the first mutual fund in 2050 B.S. It floated units of Rs. 10 par value in the beginning. The fund was of an open-ended type. The performed well in the beginning, but its performance deteriorated in 2052 B.S. and was restricted as a closed-ended fund. Similarly, the Citizen Unit Scheme (CUS) was operated by Citizen Investment Trust (CIT) as a second collective investment scheme in 2052 B.S. CIT has been managing this scheme. It was established as an open-ended scheme with a face value of Rs. 100 per unit. Security Board of Nepal (SEBON) is a regulatory body of mutual funds in Nepal. It has issued Mutual Fund Regulation, 2067 in order to regulate the mutual fund industry. The regulation has specified various terms and conditions of mutual fund operation. The regulation has provisioned the qualities of fund sponsors, fund managers, and fund supervisors. Likewise, investment criteria for mutual funds are also clearly specified in the regulation. Mutual funds in Nepal are managed by merchant bankers (fund managers) and sponsored by 'A' class commercial bank licensed by Nepal Rastra Bank. Only those merchant bankers who are direct subsidiaries of commercial banks can float and manage mutual funds. As such, mutual fund companies are full subsidiaries of commercial banks.

Present Context of Mutual Funds in Nepal

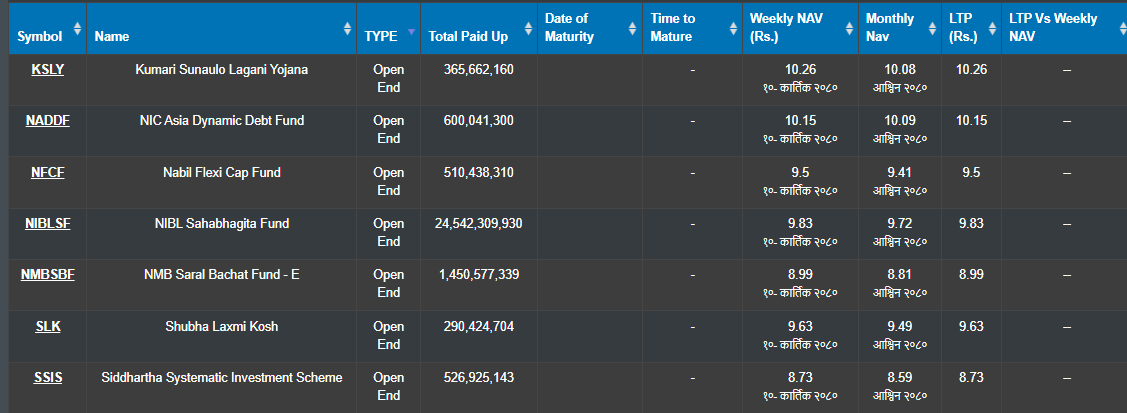

Currently, there are 42 mutual fund schemes running in the Nepalese financial market. Mutual funds have to be approved by SEBON first to publish the offer letter and accept the funds as initial public offerings. When the fund units are allotted, they are listed in NEPSE. Among these 42 schemes, 35 are close-ended while 7 are open-ended and people are only interested in close-ended schemes rather than open-ended schemes. One of the major reason behind this is that open-ended funds seems declining in terms of their NAV value especially those that are brought during the bull phase of the market.

In the above figure, all of the 7 open-ended schemes are shown. We can clearly see that out of all 7, only 2 open-ended schemes seem to be successful in maintaining their NAVs above their par value I.e.Rs.10. Even in such a bearish phase, KSLY( Kumari Sunaulo Lagani yojana) and NADDF( Nic Asia dynamic debt fund) are able to maintain their NAV above par value. By this, we can expect that with the increase in NEPSE in the coming days, these mutual funds will outperform all other open-ended schemes.

In the above figure, the H80-20 close-ended scheme has not been listed in NEPSE yet. Similarly, GIMES1, NEF, and NMBHF1 have been recently delisted from NEPSE as these funds have matured. Now, on comparing the remaining 35 close-ended schemes only 13 close-ended schemes are able to maintain their NAV above their par value. For a long-term investor, it is the best time to accumulate the shares of mutual funds at a discounted price. C30MF fund seems to be the best stock to buy for the long term as its NAV seems to be higher than others. Also, this fund has been recently listed in NEPSE during the bearish phase. Fund managers of C30MF seem to be able to buy the stocks at the lowest price in NEPSE and also to put their other funds in respective places at the right time. Besides this, there are many other mutual funds that are trading in the secondary market at a discounted price. It is also seen that many experienced players buy the stocks of mutual funds some days ago of their maturity and get handsome returns on their investments within a short period of time. After the funds mature, they are delisted from NEPSE and no trading is done. Fundholders get their amounts returned to their respective bank accounts within 3 months of their maturity at the monthly NAV. Now, NIBLPF seems to have matured within 2 months. If we compare the mutual funds return with the fixed deposit rate, only some mutual funds can compete with them. In our Nepalese market, we can see a large number of mutual fund companies don't provide any dividends to their fundholders. So, before investing in any mutual fund we should understand the company and the fund managers and their performance in past mutual funds and their returns too.

Conclusion:-

The mutual fund sector in Nepal is the most dominant sector in Nepal. Despite the challenges, mutual funds can be a valuable investment tool for investors in Nepal who are looking to diversify their portfolios and achieve financial goals. Overall, mutual funds can be both a boon and a bane in the Nepalese context, depending on the investor's perspective and investment goals. Investors should carefully consider the risks and rewards involved in mutual fund investing before making any investment decisions. So, one must do his/her own research to diversify their portfolio and also track the previous funds managed by the fund managers and their returns. Investors should re-balance their portfolio, especially in the bearish market so as to ensure that it remains aligned with their investment goals and risk tolerance.

(Disclaimer: The aforementioned information in this article is the writer’s own opinion. All the readers are advised to make investment decisions based on their study and analysis. The name of some companies stated in this article is for instance not any buy or sell recommendation.)

Article By:- Suraj Agrawal (Research Analyst)

Birtamod-4, Jhapa