Have you applied for Himalaya Urja's IPO? Take a quick look at its fundamentals before deciding

Thu, Apr 4, 2019 2:21 PM on Exclusive, IPO/FPO News, Stock Market, Latest,

Company profile

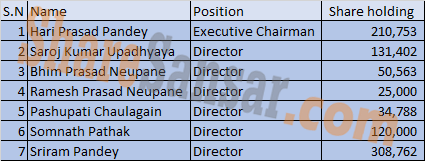

Himalayan Urja Bikas Company was incorporated in 1999 as a private limited company, and converted into a public company on November, 2014. The major promoters of Himalayan Urja are Arun Valley Hydropower Development, Ms. Tulsa Pandey, Mr. Shree Ram Pandey, Mr. Hari Prasad Pandey, Mr. Saroj Kumar Upadhyay and so on.

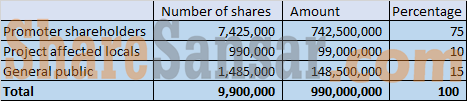

The ongoing IPO of Himalayan Urja Bikas Company will dilute its promoter ownership to 75%.

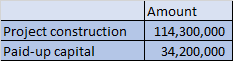

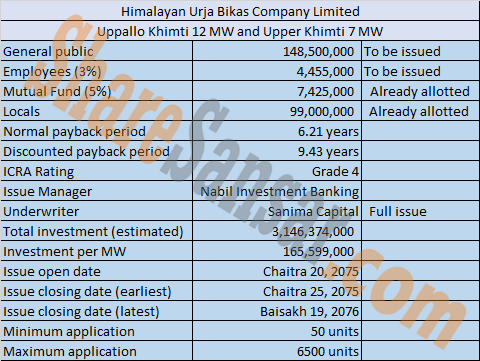

The company has been constructing a 12 MW hydropower project in Ramechhap district which has an estimated cost of Rs.3.14 Arba where the company has adopted 75:25 debt equity ratio. The Per Megawatt cost of the Company is Rs.16.55 Crore. The simple payback period of this project is 6.21 years.

Objective of the issue

About the issue

Himalaya Urja Bikas Company Limited is issuing 1,485,000 units ordinary shares worth Rs.14.85 Crore to the general public from (today) Chaitra 20, 2075. The early closing date of this IPO issue is Chaitra 25, 2075 and if the issue is not subscribed till Chaitra 25 then this issue can be extended up to Baisakh 19, 2076.

Out of the offered 1,485,000 units, 3% i.e. 44,550 units have been set aside for the employees of the company and 5% i.e. 74,250 units have been allotted for the mutual funds. The remaining 1,366,200 units are for the general public. The issue capital of the company is Rs.99 Crore and 15% share of issue capital is being offered to general public.

Nabil Investment Banking Limited has been appointed as the issue manager for the IPO issuance.

Applications can be place for minimum 50 units and maximum 6,500 units.

Recently, the company had completed the allotment of IPO issued to the locals of Ramechhap district. For the offered 9.90 Lakh units, the issue received a total of 7,040 applicants who had applied for almost 12 Lakh units of shares.

ICRA Nepal had assigned Grade 4 rating to the IPO issue of Himalayan Urja which indicates below average fundamentals.

The company has been constructing a 12 MW hydropower project in Ramechhap district which has an estimated cost of Rs.3.14 Arba where the company has adopted 75:25 debt equity ratio. The Per Megawatt cost of the Company is Rs.16.55 Crore. The simple payback period of this project is 6.21 years.

Shareholding composition

Debt structure

Primary Shareholders

Board of Directors

Credit Rating

ICRA Nepal has assigned an “[ICRANP] IPO Grade 4”, indicating below average fundamentals to the proposed Initial Public Offering (IPO) of Himalaya Urja Bikas Company Limited.

The assigned grading considers the moderate return potential from the hydro-electric projects (HEPs) being developed by HUBCL mainly due to low tariff rates for the 12 MW project (out of total project capacity of 19 MW including semi-cascade project of 7 MW). The grading also remains constrained by the evacuation risk arising out of possible delay in construction of proposed 132 kV Garjyang-Khimti transmission line by NEA which can potentially delay the commercial operation date (COD) of the project. Any delays in COD could result in cost escalations through incremental IDC and hence could further impact project earnings. Absence of deemed generation clause in Power Purchase Agreement (PPA) exposes the potential earnings to hydrological risks. Grading concerns also emanate from the interest rate volatility in the market that can have a bearing over the project return indicators. The project is also exposed to counterparty credit risks arising out of exposure to loss-making Nepal Electricity Authority (NEA) for the energy supplied, although the same is partly mitigated by the fact that NEA is fully owned by the Government and has been making timely payments to Independent Power Producers (IPPs) so far which provides some comfort.

Nonetheless, the grading considers relatively moderate project costs (~NPR 166 million per MW) and the construction progress achieved in the projects so far (~55-60% complete as of mid-Apr-18). The projects are being planned to be in operation from the Required Commercial Operation Date (RCOD) which however would remain contingent upon the timely completion of evacuation structure of NEA. With a firm PPA in place with pre-determined tariff rates and positive demand outlook owing to supply-demand gap in the power sector, the tariff and off-take risks are minimal. Going forward, ability of the company to commission the projects at current cost and timeline estimates and the ability to achieve its design operating parameters will be key driver for project returns.

Source: ICRA Nepal (https://icranepal.com/releases.php)

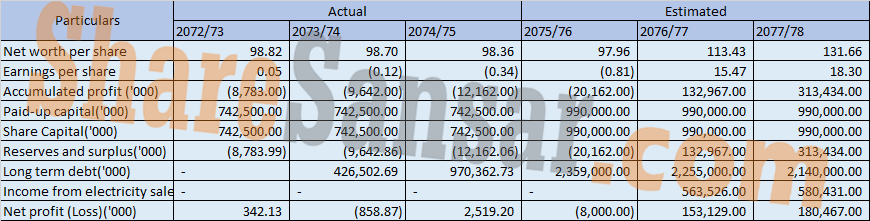

Financial performance

Conclusion

The IPO of Himalaya Urja had received good response from the project-affected locals and even from the general public side, 47% of the issue has been subscribed on the first day itself.

The issue is ongoing and if you're interested you can apply via Mero Share or from your corresponding banks.