Financial Analysis of Unilever Nepal Limited: Challenging Road Ahead

Thu, Feb 11, 2016 3:43 AM on Latest, Exclusive, Financial Analysis, Featured, Economy,

Editor's Note: Nischay Shrestha analyzes financials of Unilever Nepal Ltd. for six quarters which includes duration before and after the earthquake, unrest in Terai region and undeclared blockade of India.

Unilever Nepal Ltd. (UNL) is the part of Unilever with operations in more than 150 countries globally. It is the largest multinational FMCG company operating successfully in Nepal for more than 20 years. The registered office of UNL is at Basamadi, Makwanpur. Its factory represents the largest manufacturing investment in our country. The UNL factory manufactures products like Soaps, Detergents and Personal Products both for the domestic market and exports to India.

Terai based manufacturing and production sector have taken a heavy toll on their profit due to the unrest and the blockade from India.This short analysis on the performance of UNL has been done using the data of 6 quarterly reports published by the company since Q1 2071/72.

Unilever Nepal Ltd. (UNL) is the part of Unilever with operations in more than 150 countries globally. It is the largest multinational FMCG company operating successfully in Nepal for more than 20 years. The registered office of UNL is at Basamadi, Makwanpur. Its factory represents the largest manufacturing investment in our country. The UNL factory manufactures products like Soaps, Detergents and Personal Products both for the domestic market and exports to India.

Terai based manufacturing and production sector have taken a heavy toll on their profit due to the unrest and the blockade from India.This short analysis on the performance of UNL has been done using the data of 6 quarterly reports published by the company since Q1 2071/72.

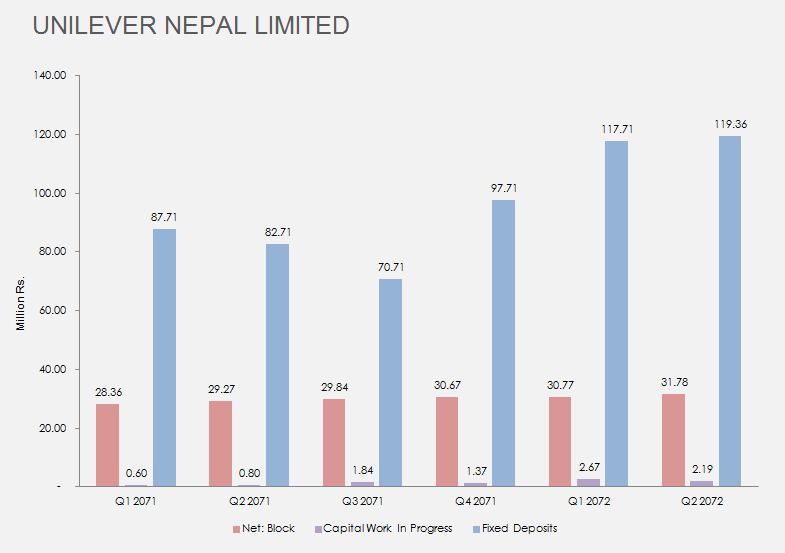

The company’s capital and reserves have remained largely unchanged. Assets under construction or not yet in service have increased by 173% and have added to the company’s unproductive assets. But this could be considered an obvious outcome of the situation generated by the April earthquake and the blockade that followed. The fact that this amount has decreased compared to the previous quarter is a positive sign.

The company, strangely, has increased its investments in fixed deposits. Its fixed deposits have increased from Rs.83 million in Q2 2071 to Rs.119 million in Q2 2072. This is an increase of 44%. Companies try to hold on to liquidity under the kind of adverse situations seen presently, but given the rock bottom interest rates and the fact that fixed deposits have limited accessibility, the company would be better off holding on to liquidity (cash).

The company’s capital and reserves have remained largely unchanged. Assets under construction or not yet in service have increased by 173% and have added to the company’s unproductive assets. But this could be considered an obvious outcome of the situation generated by the April earthquake and the blockade that followed. The fact that this amount has decreased compared to the previous quarter is a positive sign.

The company, strangely, has increased its investments in fixed deposits. Its fixed deposits have increased from Rs.83 million in Q2 2071 to Rs.119 million in Q2 2072. This is an increase of 44%. Companies try to hold on to liquidity under the kind of adverse situations seen presently, but given the rock bottom interest rates and the fact that fixed deposits have limited accessibility, the company would be better off holding on to liquidity (cash).

A significant reduction in the company’s sundry debtors is a significant step in the right direction. By decreasing collectables and increasing cash collection the company has taken the appropriate steps to deal with the situation as best it can. The total current assets of the company has decreased by 28% compared to the same quarter last year and is the lowest it has been in our review period.

A significant reduction in the company’s sundry debtors is a significant step in the right direction. By decreasing collectables and increasing cash collection the company has taken the appropriate steps to deal with the situation as best it can. The total current assets of the company has decreased by 28% compared to the same quarter last year and is the lowest it has been in our review period.

However, this has caused the company’s net current assets to become negative. This would be considered extremely bad under normal circumstances, but given the extraordinary circumstances that face the company (in the form of the effects of the earthquake and blockade), this should not be considered very bad. The fact that the company has less money stuck as assets and has levered its position through the use of debt plays in favor of the company. As the situation improves, the net current assets can be expected to become positive again.

However, this low liquidity can pose a problem for the company. The company has only enough current assets to meet 76% of its immediate liabilities.

However, this has caused the company’s net current assets to become negative. This would be considered extremely bad under normal circumstances, but given the extraordinary circumstances that face the company (in the form of the effects of the earthquake and blockade), this should not be considered very bad. The fact that the company has less money stuck as assets and has levered its position through the use of debt plays in favor of the company. As the situation improves, the net current assets can be expected to become positive again.

However, this low liquidity can pose a problem for the company. The company has only enough current assets to meet 76% of its immediate liabilities.

The company’s sales have dropped down to half of what it was during the same period last year. It has dropped to Rs.53 million in Q2 2072 from Rs.117 million in Q2 2071. In the first quarter this year, the company sold goods worth Rs.97 million. The company’s other incomes have also dropped significantly. The portion of other incomes on the company’s total income has increased to a never before seen level of 19%.

The company has done quite well in reducing its expenses. The company’s total expenses have reduced by 56% compared to the same period last year.

The company’s sales have dropped down to half of what it was during the same period last year. It has dropped to Rs.53 million in Q2 2072 from Rs.117 million in Q2 2071. In the first quarter this year, the company sold goods worth Rs.97 million. The company’s other incomes have also dropped significantly. The portion of other incomes on the company’s total income has increased to a never before seen level of 19%.

The company has done quite well in reducing its expenses. The company’s total expenses have reduced by 56% compared to the same period last year.

The company’s operating and net profits have decreased by 37% and 29% respectively. When compared to a reduction in sales of more than 50%, the fall in net profits of only 29% can be considered an accomplishment.

The company’s operating and net profits have decreased by 37% and 29% respectively. When compared to a reduction in sales of more than 50%, the fall in net profits of only 29% can be considered an accomplishment.

The company’s quarterly earnings per share (EPS) has dropped from Rs.227 to Rs.161. This is a reduction of 29%. The company’s networth has remained constant at Rs.1270.

The company’s quarterly earnings per share (EPS) has dropped from Rs.227 to Rs.161. This is a reduction of 29%. The company’s networth has remained constant at Rs.1270.

The company’s return on equity has dropped from 18% in Q2 2071 to 13% in Q2 2072. This is largely due to the reduction in the company’s asset turnover. The asset turnover ratio has reduced to half from 0.41 times in Q2 2071 to 0.20 times in Q2 2072. The increase in the company’s profit margin from 18% to 28% has helped keep the ROE afloat.

The company’s return on equity has dropped from 18% in Q2 2071 to 13% in Q2 2072. This is largely due to the reduction in the company’s asset turnover. The asset turnover ratio has reduced to half from 0.41 times in Q2 2071 to 0.20 times in Q2 2072. The increase in the company’s profit margin from 18% to 28% has helped keep the ROE afloat.

Company’s bargaining power over suppliers and creditors will be a major determinant in overcoming the challenges it currently faces.

The data shown is non-cumulated i.e. the data for Q2 is for Q2 alone and not an accumulation of Q1 and Q2. The same applies for data of Q3 and Q4.

Author can be contacted at nischay.shrestha@gmail.com.

Company’s bargaining power over suppliers and creditors will be a major determinant in overcoming the challenges it currently faces.

The data shown is non-cumulated i.e. the data for Q2 is for Q2 alone and not an accumulation of Q1 and Q2. The same applies for data of Q3 and Q4.

Author can be contacted at nischay.shrestha@gmail.com.

Unilever Nepal Ltd. (UNL) is the part of Unilever with operations in more than 150 countries globally. It is the largest multinational FMCG company operating successfully in Nepal for more than 20 years. The registered office of UNL is at Basamadi, Makwanpur. Its factory represents the largest manufacturing investment in our country. The UNL factory manufactures products like Soaps, Detergents and Personal Products both for the domestic market and exports to India.

Terai based manufacturing and production sector have taken a heavy toll on their profit due to the unrest and the blockade from India.This short analysis on the performance of UNL has been done using the data of 6 quarterly reports published by the company since Q1 2071/72.

The company’s capital and reserves have remained largely unchanged. Assets under construction or not yet in service have increased by 173% and have added to the company’s unproductive assets. But this could be considered an obvious outcome of the situation generated by the April earthquake and the blockade that followed. The fact that this amount has decreased compared to the previous quarter is a positive sign.

The company, strangely, has increased its investments in fixed deposits. Its fixed deposits have increased from Rs.83 million in Q2 2071 to Rs.119 million in Q2 2072. This is an increase of 44%. Companies try to hold on to liquidity under the kind of adverse situations seen presently, but given the rock bottom interest rates and the fact that fixed deposits have limited accessibility, the company would be better off holding on to liquidity (cash).

A significant reduction in the company’s sundry debtors is a significant step in the right direction. By decreasing collectables and increasing cash collection the company has taken the appropriate steps to deal with the situation as best it can. The total current assets of the company has decreased by 28% compared to the same quarter last year and is the lowest it has been in our review period.

However, this has caused the company’s net current assets to become negative. This would be considered extremely bad under normal circumstances, but given the extraordinary circumstances that face the company (in the form of the effects of the earthquake and blockade), this should not be considered very bad. The fact that the company has less money stuck as assets and has levered its position through the use of debt plays in favor of the company. As the situation improves, the net current assets can be expected to become positive again.

However, this low liquidity can pose a problem for the company. The company has only enough current assets to meet 76% of its immediate liabilities.

The company’s sales have dropped down to half of what it was during the same period last year. It has dropped to Rs.53 million in Q2 2072 from Rs.117 million in Q2 2071. In the first quarter this year, the company sold goods worth Rs.97 million. The company’s other incomes have also dropped significantly. The portion of other incomes on the company’s total income has increased to a never before seen level of 19%.

The company has done quite well in reducing its expenses. The company’s total expenses have reduced by 56% compared to the same period last year.

The company’s operating and net profits have decreased by 37% and 29% respectively. When compared to a reduction in sales of more than 50%, the fall in net profits of only 29% can be considered an accomplishment.

The company’s quarterly earnings per share (EPS) has dropped from Rs.227 to Rs.161. This is a reduction of 29%. The company’s networth has remained constant at Rs.1270.

The company’s return on equity has dropped from 18% in Q2 2071 to 13% in Q2 2072. This is largely due to the reduction in the company’s asset turnover. The asset turnover ratio has reduced to half from 0.41 times in Q2 2071 to 0.20 times in Q2 2072. The increase in the company’s profit margin from 18% to 28% has helped keep the ROE afloat.

Company’s bargaining power over suppliers and creditors will be a major determinant in overcoming the challenges it currently faces.

The data shown is non-cumulated i.e. the data for Q2 is for Q2 alone and not an accumulation of Q1 and Q2. The same applies for data of Q3 and Q4.

Author can be contacted at nischay.shrestha@gmail.com.