Your ride is just about to begin! Four reasons why you should consider buying commercial bank’s stocks

Sun, Jul 8, 2018 9:56 AM on Exclusive, Financial Analysis, Stock Market, Latest,

What a roller coaster ride it has been to investors of the commercial banks! Ever wondered how your first roller coaster ride experience in the amusement park was like?

Just like the coaster ride comes with your heart pounding, a lot of screaming and fear of losing your life, the recent years have been full of anticipations, excitement and fear of loss to the commercial banks’ shareholders. Then, right when you are getting used to the roller coaster ride, the time is up and all the excitement is gone. The present context for the investors of commercial bank is similar. All these mixed emotions will probably come to an end as most of the banks have now met their paid up capital plan.

The exact time to put on the safety belts and take this roller coaster ride was back when investors came across the NRB’s directive to meet a paid up capital of Rs 8 arba. But, what about the time to experience the thrill?

The experience of thrill came with the announcement of capital plan of these “A” graded commercial banks. Every single time the announcement of bonus share was done, investors got an opportunity to speculate. For instance, news of bonus share would hike the price due to the increase in demand and right there was the thrill- the thrill to grab the profit. Remember, how the market reacted to Standard Chartered’s 100% bonus share and how smart players speculated so well?

But there were also the time when we rechecked if our safety belt was locked properly just as we do during a roller coaster ride. For instance, we looked for the merger and acquisition news and sold our shares if we got a clue that our trading would be halted for a long period of time. Remember, The MEGA’s mega mysterious merger with Tourism Development Bank which took a year to be resolved?

However, as you read these above paragraphs, did you feel you have missed so many opportunities to earn? It’s just that you don’t belong to the group of friends who enjoy the thrill, the excitement and the fear. You are just one of those friends who stay down waiting for your friends to complete the roller coaster ride so that you can go and join some other games that are less risky. Meaning: you just did not wanted to be a part of the speculation of commercial banks scrips and stood buying and selling nothing. Well, this exact time is for you- the long term investors. If you are the investor looking forward for less risk and a maximized value of wealth after a certain years, then this might be exactly the best time to enter the market. For some of you with a long term vision, your ride is just about to begin!

Commercial banks hold the highest portion of market capitalization in the Nepalese secondary market when compared to other eight sectors. Commercial banks, as defined, are the A class financial institutes of the country. These banks are relied upon by other smaller banks and financial institutes for several motives. Nepal Rastra Bank usually prioritizes its effort to facilitate the development of these commercial banks.

As of today, the stocks of commercial banks are considered to be better than the other sectorial stocks for a long term investor. Several reasons that can be attributed are:

1. The declining price of commercial banks’ stocks:

With the increasing number of listed shares through right and bonus of the commercial banks, the supply of the shares in this sector has increased immensely. The macroeconomic aspects of the country such as Communist government, the fiscal budget announcement and liquidity crisis in banks have decreased the demand of these shares. As a result of the mismatch between demand and supply of these shares, the prices of the shares of commercial banks have declined. If we compare the price of these stocks as of 3rd July, 2018 and 29th March, 2012 (when NEPSE index had reached least to 292), the price of most of the stocks are in the similar range. The current price of scrips such as SCB is lower than the price when NEPSE index was at 292 by Rs 636. Similarly, EBL has a difference of only Rs 2 if we compare the price on that day and today. Similarly, stocks such as CZBIL, KBL, NABIL, SBI have a difference below 100.

Besides, the average P/E ratio of commercial bank was at 35 times when the market was in Bull Run two years before with a NEPSE index of 1888. If we observe the average P/E ratio today, it is just below 15 times. This suggests the current price of commercial bank’s stocks I relatively low and P/E below 15 is a buying price for the commercial banks.

.png)

If we compare the price of stocks in commercial bank’s sectors to sectors such as insurance and microfinance, the stocks are far cheaper so, if the investors are looking for less volatile scrips, commercial banks might be their choice of investment.

So, wouldn’t you take that roller coaster ride which guarantees a less speed and a cheaper price?

2. The upcoming announcement on bonus shares and cash dividend:

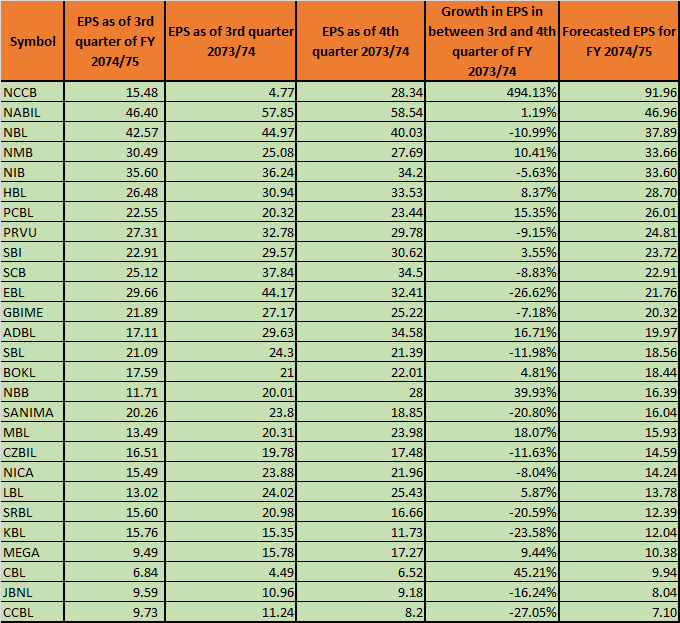

In the months of Ashar and Shrawan, all the commercial banks publish their fourth quarter report and conduct an AGM to propose dividend to shareholders either in the form of cash or bonus. Once the announcement is made, the stock price usually increases in a skyrocketing way. Thus, investors can estimate the overall performance of commercial banks analyzing the third quarter reports. The smart players usually buy the shares at the lower price such as now and sell it off when the price increases post the announcement of dividend. But how do the smart players estimate the returns? Are they right every single time? They probably might not be right every single time but here is a glimpse of how smart players estimate the returns.

Now, here is a catch. Just because NCCB had an aggressive growth in the last year leading to a tremendous increase in EPS, does not mean investors can expect the same this year. Similarly, there are certain things that have been observed in the past such as most of the big banks with high EPS prefer to provide fewer dividends to shareholders and transfer the return in the reserve fund. So, it is not necessary that the table provides an accurate prediction but it all depends on investors as how they will analyze the numbers. Also, this year commercial banks had faced CCD ratio crunch so, EPS and net profit might not see the same impact this year.

So, wouldn’t you put an extra effort to find the roller coaster ride with more fun and less risk?

3. Publication of annual reports of commercial banks:

Majority of commercial banks further publish their annual reports in Asar and Shrawan. With merely 28 commercial banks, investors base their assumptions on third quarterly unaudited reports and make a prediction what net profit can be expected from each of them. Usually, the market will react according to the annual reports published or make investment decision prior to the publication of these reports. Thus, investors can buy the stocks now on the basis of third quarter reports and hold their stocks for a longer period of time.

The net profit for third quarter of commercial banks are:

.png)

4. The opened gateways for commercial banks:

All the commercial banks are in the same range of Rs 8 arba. The segment of customers is the same for all commercial banks. So, the winners will be those who will be able to cater the new segment and find new avenues of customers. NRB has directed commercial banks for foreign loans. Thus, the concentration of investors should be on those commercial banks which can bring foreign loans being cost efficient. Similarly, the banks which can invest in highly productive sectors rather than less productive sectors should be on the priority list. Thus, long term investors seeking to invest in commercial banks should be up to date with the MOA signed by commercial banks with the foreign banks and other agriculture and manufacturing sectors. The commercial banks are further directed to open branches in inaccessible rural places. Thus, the banks that expand their outreach among rural population will be able to expand their loan and deposit portfolio. Further, with the certificate collateralized loan policy, banks than concentrate to motivate entrepreneurship will be seen to be the winner in the upcoming years.

The long term strategy might not appeal for every single investor. However, if you are one of those who don’t want to be the part of the herd, its high time; you bring in stocks of commercial banks in your portfolio. Let the slow ride begin!