What does the article cover?

-Management

-Operational efficiency

-Financial overview

-Gap between new and old life insurance companies

The increased paid up capital of all BFIs is said to resemble the initiation for stronger foundation of the economy. However, on the other side of the story, this increment can also be attributed to the decreasing threat of barrier of entry of the new entrants in the industry. While the establishment of new financial institutions has been discouraged by the regulatory bodies, the insurance sector is still enthusiastic to serve the general public. Although it has been more than two years since the dreading earthquake of 2015, the impact of this event is still significant in the insurance sector. Besides, the rising awareness among people and their increasing living standard has further benefited the life insurance industry. Despite the financial barriers, the newly established life insurance companies are proof that these companies carry a praiseworthy motivation to serve the public.

Among the licensed new life insurance companies, the nine life insurance companies that have published their financial statements are:

- Sun Nepal Life Insurance Company

- SANIMA Life Insurance Company

- Citizen Life Insurance Company

- Reliance life Insurance Company

- IME Life Insurance Company

- Union Life Insurance Company

- Jyoti Life Insurance Company

- Prabhu Life Insurance Company (STAR Life Insurance Company)

- Reliable Nepal Life Insurance Limited

It is of no wonder that these new insurance companies might soon require funding from public either in the form of IPO or FPO. Thus, to facilitate the enthusiasts in the primary market, the article has been prepared beforehand accumulating the analysis of these new life insurance companies.

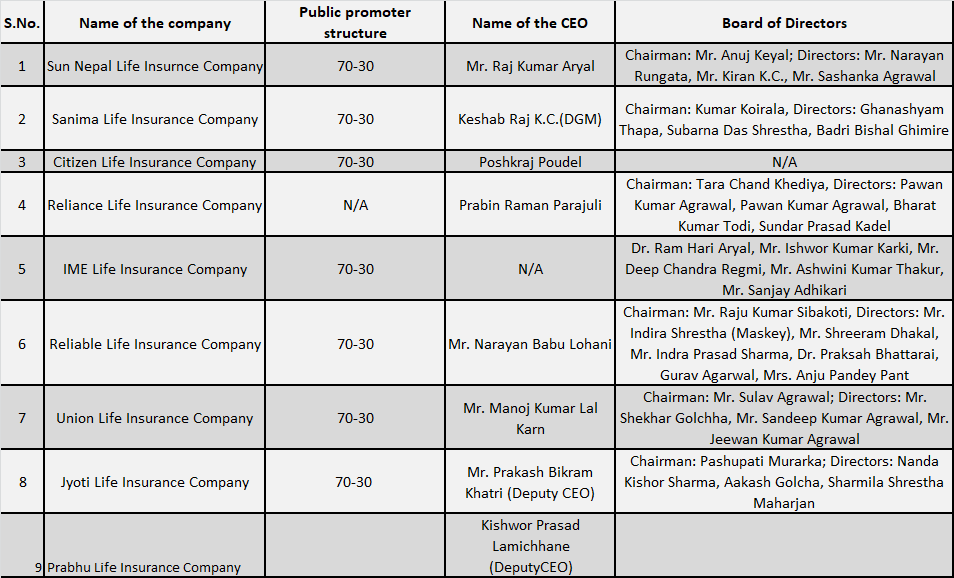

I. Management: Public promoter share structure, CEO and BODs:

Most of the new life insurance companies have decided to form 70:30 public promoter share structure. The aspiring investors in the primary market can therefore, look forward a number of investment opportunities in the insurance sector. In order to determine, whether these insurance companies are in the hand of good management or not, the names of Chief Executive Officer (CEO)s and Board of Directors (BODs) have been attached hereby in the table:

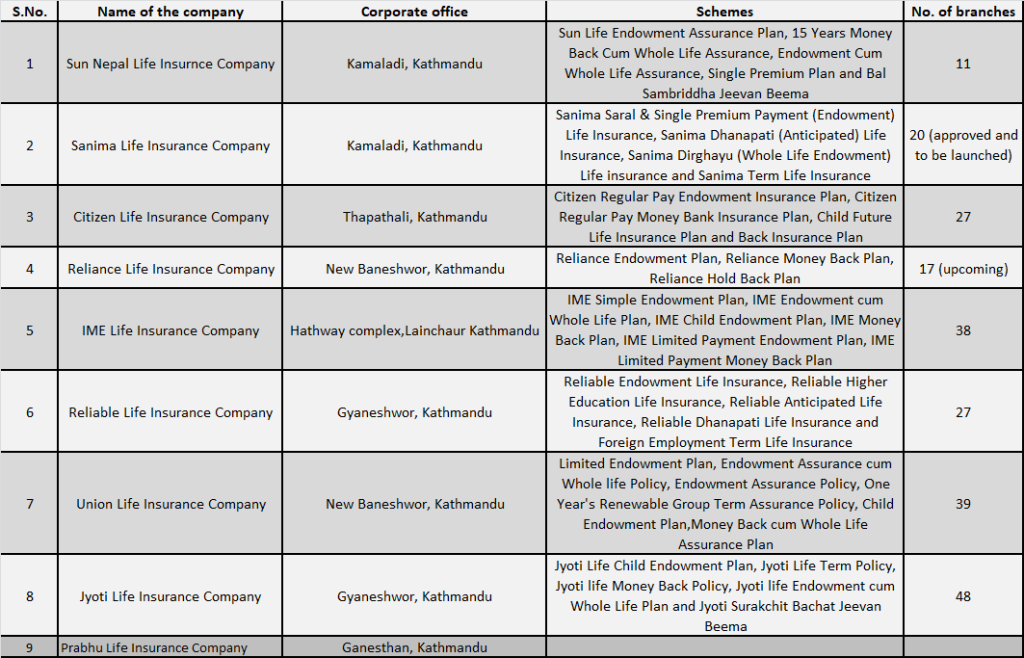

II. Operational Efficiency: Corporate office, schemes and branches:

II. Operational Efficiency: Corporate office, schemes and branches:

The operational efficiency of these new insurance companies can be measured in terms of branches and schemes introduced. The companies have been selling products such as Endowment, Money Back, Whole Life, Anticipated, Child Future, Regular Pay Back and many more.

III. Financial overview:

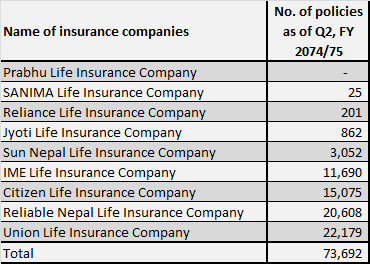

A. Number of policies:

III. Financial overview:

A. Number of policies:

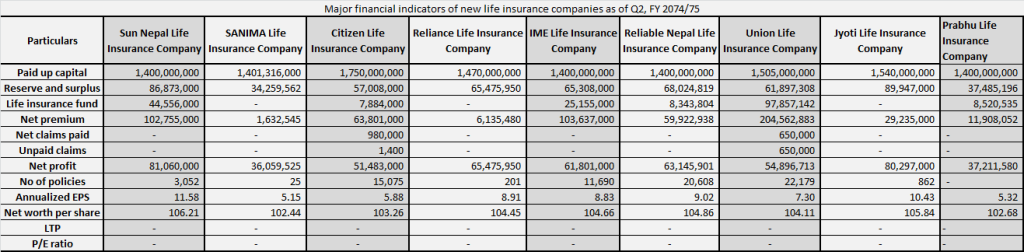

Even in the short duration of establishment, life insurance companies have been able to collect a total of 73,692 numbers of insurance policies. Union Life Insurance Company has been maintaining a lead position with 22,179 policies followed by Reliable Life Insurance (20,608) and Citizen Life Insurance (15,075) as of second quarter of FY 2074/75.

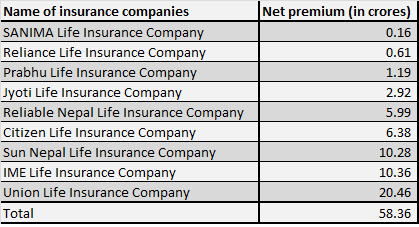

B. Net Premium

B. Net Premium

As of second quarter of this fiscal year, the infant insurance companies have been able to collect Rs 58.36 crores of net premiums. Union Life Insurance Company has the highest net premium collected worth Rs 20.46 crore. The company is followed by IME Life Insurance (Rs 10.36 crores) and Sun Nepal Life Insurance (Rs 10.28 crores).

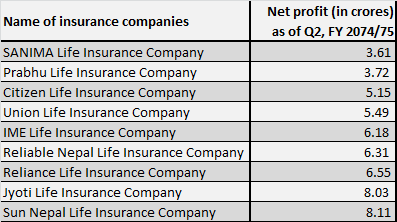

C. Net profit:

C. Net profit:

Among the newly established life insurance companies, the second quarter report shows that Sun Nepal Life Insurance has earned the highest net profit of Rs 8.11 crores. It is further followed by Jyoti Life Insurance Company with net profit of Rs 8.03 crores and Reliance Life Insurance Company with Rs 6.31 crores. SANIMA Life Insurance Company has the least amount of net profit that amounts to Rs 3.61 crores.

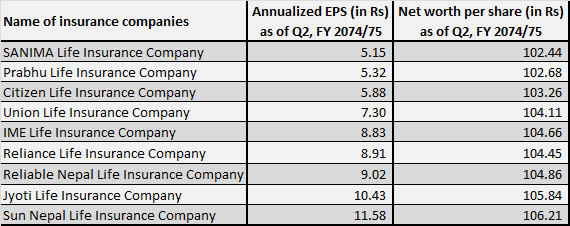

D. Annualized EPS and Net worth per share:

D. Annualized EPS and Net worth per share:

The insurance company that has won the race of annualized EPS and net worth per share is Sun Nepal Life insurance Company. The company’s annualized EPS stands at Rs 11.58 while net worth per share at Rs 106.21. It is further followed by Jyoti Life Insurance Company with an EPS of Rs 10.43 and net worth per share of Rs 105.84. Finally, Reliable Nepal Life Insurance Company has an EPS of Rs 9.02 and net worth per share of Rs 104.86. SANIMA Life Insurance Company takes the last position with Rs 5.15 as annualized EPS and Rs 102.44 as net worth per share.

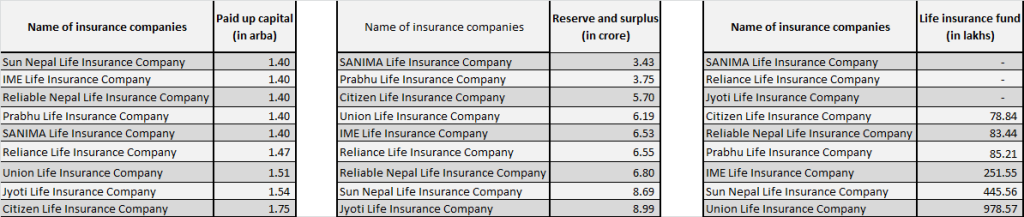

E. Paid up capital, reserves and surplus and life insurance fund:

E. Paid up capital, reserves and surplus and life insurance fund:

Each of these new life insurance companies have paid up capital either 1.40 arba or above. Citizen life Insurance Company has the highest paid up capital (Rs 1.75 arba), followed by Jyoti Life Insurance Company (Rs 1.54 arba), Union Life Insurance Company (Rs 1.51 arba) and Reliance Life Insurance Company (Rs 1.47 arba). All the remaining five companies have a paid up capital of Rs 1.40 arba.

Jyoti Life Insurance Company has the highest reserve of Rs 8.99 crore. It is further followed by Sun Nepal Life Insurance Company with a reserve fund of Rs 8.69 crore. Finally, Reliable Nepal Life Insurance Company is seen in the third position with a reserve of Rs 6.80 crore. SANIMA Life Insurance Company has a reserve of Rs 3.43 crore which is the least among the new life insurance companies.

Six among the nine new life insurance companies have announced their life insurance fund in the second quarter. Union Life Insurance has created highest fund with an amount of Rs 978.57 lakhs. Sun Nepal Life Insurance Company stands at the second position with a fund of Rs 445.56 lakhs. IME Life Insurance Company is seen in the third position with Rs 251.55 lakhs in insurance fund.

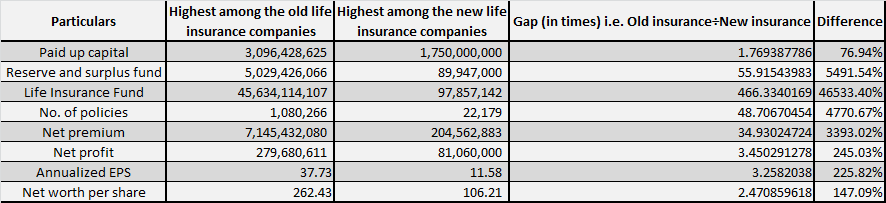

IV. Gap between new and existing life insurance companies:

IV. Gap between new and existing life insurance companies:

The existing life insurance companies have grown their business in an aggressive manner. Provided this, the new entrants will face a tough time trying to match the pace of these dominant players in the life insurance industry. The following table includes the highest amount of both new and old life insurance companies with respect to major indicators along with the difference:

The highest amount for the old companies represents Nepal Life Insurance Company (NLIC) in terms of paid up capital, Reserve and surplus, life insurance fund, no. of policies, net premium, net profit and net worth per share. Similarly, the highest amount for the old companies represents Prime Life Insurance Company (PLIC) in terms of EPS.

Attached is the complete detail of the major indicators of new life insurance companies:

Given the study on these new life insurance companies, what strengths and opportunities do you think they have in the highly dominated insurance industry? Do you think these insurance companies will match the pace of the big giant insurance companies? Would you prefer investing in these new insurance companies if the opportunity of investment is granted? Also, if you have any specific topics or industry that you want Sharesansar to cover exclusively, please write in the comment section below.

Disclaimer: The sources of provided information are quarterly reports, website and spokesperson. Any misinterpretation from the sources might be not adjusted in the analysis.