Sector-Wise Trends in NEPSE Listings: A Two-Decade Analysis

Sun, May 3, 2026 8:23 AM on NEPSE News, Exclusive,

As most of us talk about the Nepal Stock Exchange (NEPSE) index, listed companies, its capitalization, and the weightage of capitalization, we know and think about BFIs (Bank and Financial Institutions), including insurance. Are things still supporting this perspective, or showing any signal for future trends? Then, which sector is taking the lead? What is the trend in the number of listed companies? What is the weightage of market capitalization sector wise? The provided data reveals a significant transformation in the capital market over the last two decades. The market has evolved from a bank-dominated landscape to a more diversified ecosystem with a massive surge in total valuation.

Data of every year’s Mid-March (or eight months of every fiscal year)

Base year is 2007 for this article’s data

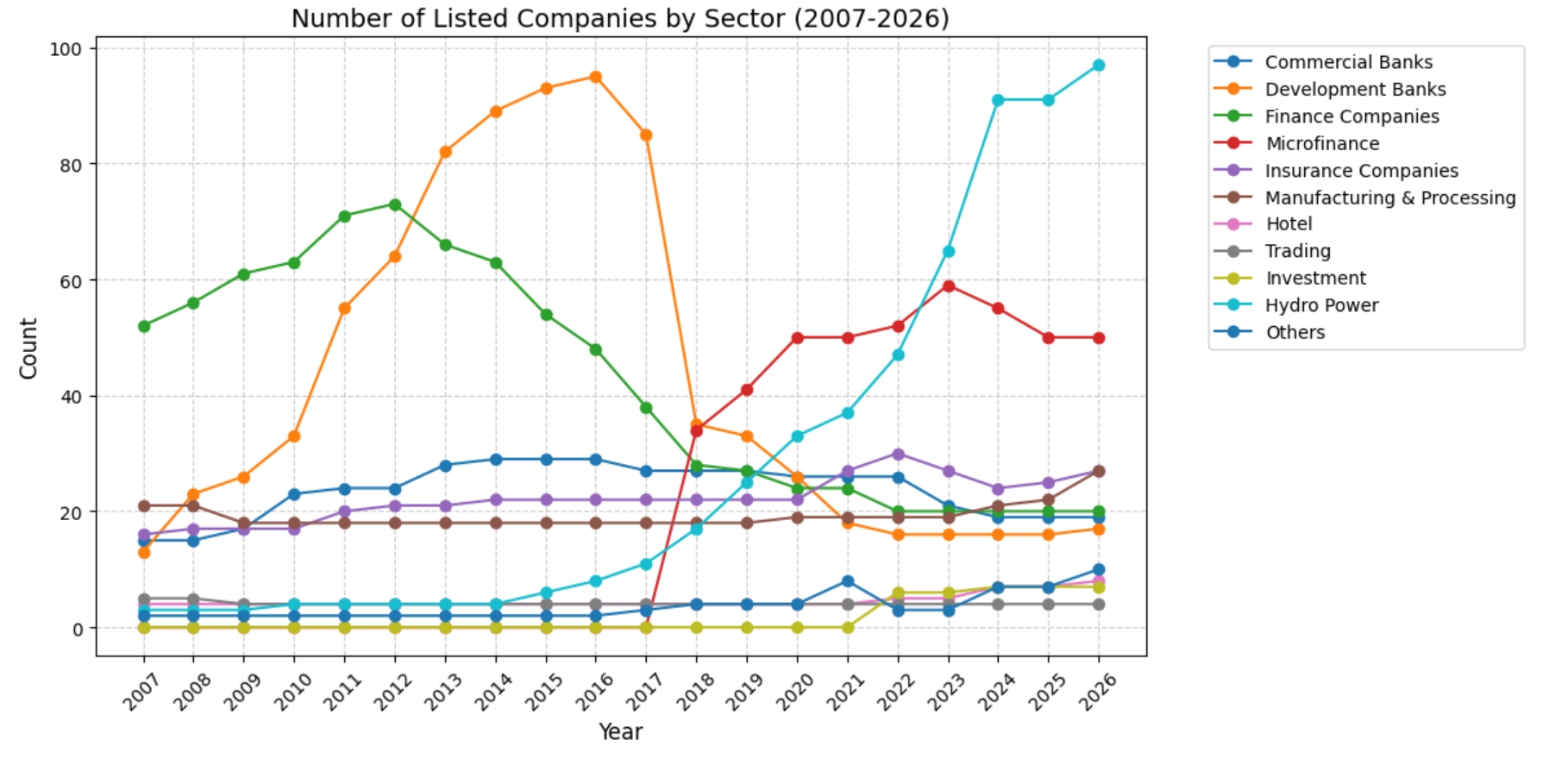

As of 2007, 131 companies were listed in NEPSE. At that time, NRB-licensed BFIs of class “A”, “B”, and “C” were 15, 13, and 52 respectively, and 16 insurance companies were listed. At that time, microfinance did not have a separate sub-index. Additionally, Manufacturing & Processing had 21 companies, Hotel 4, Trading 5, Hydropower 3, and the Others sub-index had 2 companies.

Chart Results:

- Commercial Banks

The trend of commercial bank listings is comparatively stable in the overall index. At the start of the data study (A.D. 2007), there were 15 commercial banks. The number of commercial banks kept increasing until 2014, reaching 29 listed class “A” banks. This number stayed the same until 2016, then started to decline onward. In the years 2022 to 2023, 5 commercial banks were delisted, which is the highest number of delistings in a one-year review period. Now, 19 commercial banks are listed in NEPSE.

- Development Banks

The trend of development bank listings seems highly skewed. In the initial year of this study’s data, there were 13 development banks, which is the lowest in number. On a year-on-year (YoY) basis, the highest number of added development banks was in the year 2010 to 2011. In that year, 22 class “B” banks were added to the list. Then, in the year 2012 to 2013, 18 development banks were added. Listed development banks reached a peak in 2016 with 95 banks. Afterward, the number started to decline. From the peak of 95 banks in 2016, it decreased by 10 by 2017. From 2017 to 2018, 50 class “B” banks were delisted in a year because many of them were microfinances. Microfinance index was created separately then listed accordingly. Now it stays constant at 17 in number.

- Finance Companies

The trend of class “C” institutions is one of the most price-fluctuating indices in NEPSE. It also has a story of fluctuations in the number of listed companies. In 2007, there were 52 finance companies. It peaked at 73 in the year 2012, then steadily declined to 20 by mid-March 2026.

- Microfinance

Based on the data revealed by NRB, class “D” financial institutions did not have a separate sub-index in NEPSE. Microfinance got a separate sub-index in November 2017. Currently, there are 50 listed microfinances in NEPSE.

- Insurance Companies

There were 16 listed companies (life and non-life) in 2007 in NEPSE. This number kept increasing at a slow pace. This sector’s listed companies peaked at 30 in the year 2022. Then existing major companies underwent mergers and acquisitions. Meanwhile, new micro-insurance companies are being added to the list. Now, as of mid-March 2026, 27 insurance companies are listed in NEPSE.

- Manufacturing & Processing

Manufacturing and Processing, also known as the real sector, has another trendline story. In the year 2007, there were 21 companies listed in this sector. This number declined to 18 in 2009. For a decade, no company was interested or dared to issue shares and get listed on the stock market until 2019. In the year 2020, this sector got 1 new member, then stayed almost constant for half a decade. Now, as of mid-March 2026, this sub-index has 27 members.

- Hotel & Tourism

After a period of stagnation, from 2007 to 2021, there were only 4 companies listed in this sector. There is a visible uptick in listings toward the 2024–2026 period, signaling a recovery and expansion in the hospitality industry.

- Trading

The most stagnated sector in NEPSE, from the perspective of listed companies, is Trading. In 2007, there were 5 listed companies in this sector, and 4 companies remain as of mid-March 2026. The number has changed in between this period.

- Investment

This sub-index was created in 2022. In that year, there were 6 companies. Previously, those companies were listed under the Others sector. Now, as of mid-March 2026, there are 7 companies.

- Hydro Power

The number of listed hydropower companies skyrocketed from 3 in 2007 to 97 by 2026. This sector is the primary driver behind the diversification of the stock exchange. This sector has a positive growth rate and has not observed mergers and acquisitions in practice.

- Others

This sector includes telecommunication, media, reinsurance, alternative renewable energy, and agriculture-based companies. Listed companies in this sector are steadily increasing with diverse types of businesses. In the future, this could be a leading and highly growing sector.

Conclusion & Strategic Outlook

For Investors:

The data suggests a shift in the market’s risk profile. The market is no longer solely dependent on the performance of the banking sector. The significant influx of hydropower and investment companies has created new avenues for portfolio diversification.

At the same time, the increasing number of listed companies may make the decision-making process less efficient. Investors may face decision dilemmas due to the wider range of choices. It also requires more time and effort to screen, study, evaluate, and execute investment decisions as the number of companies grows.

For Policy Makers:

The rapid increase in the number of listings particularly in the energy sector indicates a successful transition toward utilizing the capital market for infrastructure financing. However, allowing many companies to raise capital and enter the market may also lead to unintended consequences if not properly monitored.

The evolution of the banking sector provides an important lesson. The sector experienced both rapid expansion and subsequent consolidation in terms of listed entities. Currently, the banking sector appears more stable and healthier, which can be attributed to the collective responsibility and coordinated efforts of regulators, institutions, and other stakeholders.