Relaxation of regulation surges profit of Nabil Bank; Nabil bank uses double standard in calculations of Q1 report

Nabil bank’s profits surge in first quarter due to relaxation of banking rules by the Nepal Rastra bank (NRB) rather than increase in core banking business.

A closer look at the Q1 report does not give a pleasant picture. The bank has taken full advantage of the recent relaxation of regulation pertaining to the loan loss provision.

As the stock dividend of 30% declared by NABIL is yet to be approved by the NRB, it classified this declared bonus as reserve while calculating the EPS. However, while mentioning the paid up capital it took liberty of including 30% bonus share which is yet to be approved by the NRB. So, in Q1 report, the Nabil bank has used double standard to include numbers that is favorable to the bank.

In other words, when Nabil Bank included the 30% bonus in its paid up capital, ethically it should have used the same paid up capital to calculate the EPS. However, to increase its EPS the bank conveniently used paid up capital from Q4 of last fiscal year. So, if the increased paid up capital is used to calculate the annualized EPS of Nabil bank, it stands at Rs.55.84. If 30% bonus share is not included then its annualized EPS stands at Rs.72.60. (The total number of shares of a company is used to calculate the EPS. In this case the total number of shares of Nabil bank can be calculated by dividing it’s paid up capital by 100).

As per the NRB relaxation of loan loss provision, If a borrower is able to pay principal, interest or installment of a loan by the end of Poush 2072, then such loan can be categorized as good loan. The loan loss for such loans should be provisioned accordingly. No penalty or additional fees can be collected from loans categorized as good loans using this section. These relaxations will only apply to loans which were at good standing during the end of Chaitra 2072.”

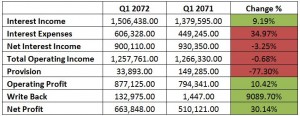

Using the above relaxation, Nabil bank has only provisioned Rs 3.38 crore for the loan loss while it had provisioned Rs 16.88 crore and Rs 14.98 crore in Q4 and Q1 respectively of last fiscal year. This is a whopping 77.30% decrease in loan loss provision as compared to the corresponding quarter of the last fiscal year.

Furthermore, the net interest income of the bank has decreased by 3.25 % as compared to the corresponding quarter of the last fiscal year.This decrease in net interest income is due to big rise in interest expenses by 34.97 % compared to the same quarter last fiscal year.

The bank’s Non-Performing Loan (NPL) has decreased by 26.67 % which can also be attributed to the relaxation granted by the NRB.

As per the NRB relaxation of loan loss provision, If a borrower is able to pay principal, interest or installment of a loan by the end of Poush 2072, then such loan can be categorized as good loan. The loan loss for such loans should be provisioned accordingly. No penalty or additional fees can be collected from loans categorized as good loans using this section. These relaxations will only apply to loans which were at good standing during the end of Chaitra 2072.”

Using the above relaxation, Nabil bank has only provisioned Rs 3.38 crore for the loan loss while it had provisioned Rs 16.88 crore and Rs 14.98 crore in Q4 and Q1 respectively of last fiscal year. This is a whopping 77.30% decrease in loan loss provision as compared to the corresponding quarter of the last fiscal year.

Furthermore, the net interest income of the bank has decreased by 3.25 % as compared to the corresponding quarter of the last fiscal year.This decrease in net interest income is due to big rise in interest expenses by 34.97 % compared to the same quarter last fiscal year.

The bank’s Non-Performing Loan (NPL) has decreased by 26.67 % which can also be attributed to the relaxation granted by the NRB.

If the NRB had not introduced the credit relaxation regulation the profit growth of Nabil bank would have been well below 10% for the first quarter of this fiscal year. If that relaxation was not in place, the loan loss provision of Nabil bank would have been well above Rs.10crore as it had provisioned Rs.14.92 crore in the corresponding quarter of the last fiscal year.

Overall, the bank and financial institutions will be publishing the Q1 report with huge surge in profits due to the relaxation provided by the NRB. These Q1 reports will only serve as mirage to the investors. So, investors must not just rely on the headlines of Q1 reports as those waived loan loss provisions will come to haunt the balance sheets by the end of the current fiscal year.

If the NRB had not introduced the credit relaxation regulation the profit growth of Nabil bank would have been well below 10% for the first quarter of this fiscal year. If that relaxation was not in place, the loan loss provision of Nabil bank would have been well above Rs.10crore as it had provisioned Rs.14.92 crore in the corresponding quarter of the last fiscal year.

Overall, the bank and financial institutions will be publishing the Q1 report with huge surge in profits due to the relaxation provided by the NRB. These Q1 reports will only serve as mirage to the investors. So, investors must not just rely on the headlines of Q1 reports as those waived loan loss provisions will come to haunt the balance sheets by the end of the current fiscal year.

As per the NRB relaxation of loan loss provision, If a borrower is able to pay principal, interest or installment of a loan by the end of Poush 2072, then such loan can be categorized as good loan. The loan loss for such loans should be provisioned accordingly. No penalty or additional fees can be collected from loans categorized as good loans using this section. These relaxations will only apply to loans which were at good standing during the end of Chaitra 2072.”

Using the above relaxation, Nabil bank has only provisioned Rs 3.38 crore for the loan loss while it had provisioned Rs 16.88 crore and Rs 14.98 crore in Q4 and Q1 respectively of last fiscal year. This is a whopping 77.30% decrease in loan loss provision as compared to the corresponding quarter of the last fiscal year.

Furthermore, the net interest income of the bank has decreased by 3.25 % as compared to the corresponding quarter of the last fiscal year.This decrease in net interest income is due to big rise in interest expenses by 34.97 % compared to the same quarter last fiscal year.

The bank’s Non-Performing Loan (NPL) has decreased by 26.67 % which can also be attributed to the relaxation granted by the NRB.

If the NRB had not introduced the credit relaxation regulation the profit growth of Nabil bank would have been well below 10% for the first quarter of this fiscal year. If that relaxation was not in place, the loan loss provision of Nabil bank would have been well above Rs.10crore as it had provisioned Rs.14.92 crore in the corresponding quarter of the last fiscal year.

Overall, the bank and financial institutions will be publishing the Q1 report with huge surge in profits due to the relaxation provided by the NRB. These Q1 reports will only serve as mirage to the investors. So, investors must not just rely on the headlines of Q1 reports as those waived loan loss provisions will come to haunt the balance sheets by the end of the current fiscal year.