Palpa Cement Limited Issues IPO for General People From Today; In Depth Analysis of Company Performance

Tue, Feb 24, 2026 10:44 AM on Company Analysis, Latest,

Company Profile:

Palpa Cement Industries Ltd., a subsidiary of RMC Group, Nepal, which manufactures Tansen Cement. Palpa Cement Industries Ltd. started its operations in 2019 and manufactures Clinker, OPC Cement & PPC cement in the brand of Tansen Cement. It also owns limestone mines that have an estimated deposit of 24 million MT. This factory is based in Sunwal, Nawalparsi, Nepal and has a capacity of 1800 MT per day of Clinker and 2200 MT per day for Cement.

Board of Directors

|

Name |

Position |

|---|---|

|

Mr. Rajesh Kumar Agrawal |

Chairman |

|

Mr. Vishnu Kumar Agrawal |

Managing Director |

|

Ms. Sweety Kumari Agrawal |

Director |

|

Mr. Yash Agrawal |

Director |

About the Issue and Rating

|

Particulars |

Details |

|---|---|

|

Total IPO Issue |

7,500,000 Units (Rs. 750 Million) |

|

Face Value |

Rs. 100 per share |

|

Percentage of Capital |

20% of issued capital (Total Capital: Rs. 3.75 Billion) |

|

Issue Manager |

Nabil Investment Banking Limited |

|

Credit Rating |

IRN BB+ (Infomerics Nepal) - Indicates moderate risk in meeting financial obligations |

The issued capital of the company is Rs. 3.75 Arba. Of this, 20%, i.e., 75,00,000 unit shares, will be issued to the public. Out of the total issue capital, 5%, which amounts to 18,75,000 unit shares worth Rs. 18.75 Crores, were allotted to project-affected locals of West Nawalparasi (Former Nawalparasi District). The remaining 15% of the issued capital, i.e., 56,25,000 unit shares, are for the general public. Of this general public issue, 10% of 56,25,000, a total of 5,62,500 unit shares, were already allotted for the Nepalese citizens working abroad.

Of the general public issue, 5%, i.e., 2,81,250 units, have been set aside for the company's employees, and 5% of the total offered shares, i.e., 2,81,250 units, have been reserved for mutual funds. The remaining 45,00,000 units will be issued for the general public and opened from today. With an IRN BB+ rating indicating moderate risk, the company plans to use the proceeds to reduce debt and boost working capital for its high-tech, export-oriented operations.

|

Category |

Status |

Opening Date |

Closing Date (Early) |

|---|---|---|---|

|

General Public |

Opening Soon |

Feb 24, 2026 (Falgun 12) |

Feb 27, 2026 (Falgun 15) |

|

Project Affected Locals |

Closed |

Jan 9, 2026 |

Feb 4, 2026 |

|

Foreign Migrant Workers |

Closed |

Dec 30, 2025 |

Jan 14, 2026 |

Financial Ratio:

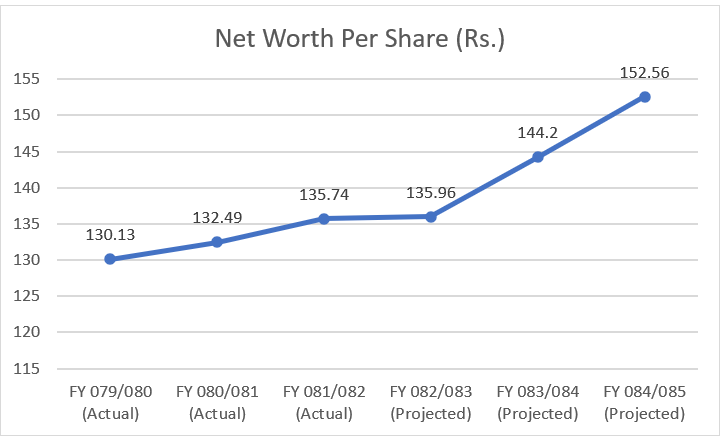

- Net Worth Per Share:

Palpa Cement Industries Limited demonstrates a stable and strengthening financial foundation, with its Net Worth per Share projected to grow from Rs. 130.13 to Rs. 152.56 by FY 084/85. This upward trend indicates the company will do well in future if everything goes as planned.

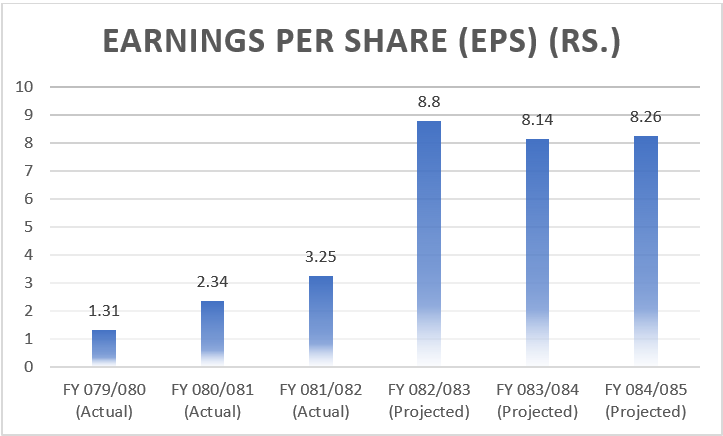

2. EPS Per Share

The company’s actual EPS for the F.Y. 81/82 is Rs. 3.25, and its projection is three times bigger than the current EPS. The company project it’s EPS Rs. 8.26 for the F.Y. 84/85. If the company is able to fulfil it’s short term obligation and maintain liquidity, then it can grow it’s profit which will lead to the increase in EPS.

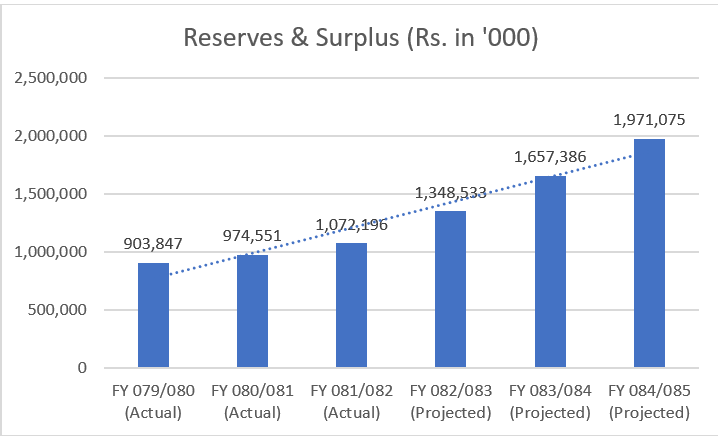

3. Reserve & Surplus

The charts reveal a company with a rock solid foundation but highly ambitious future targets. While the actual data shows steady, reliable growth in Net Worth (climbing to Rs. 135.74), the projected figures anticipate a massive performance leap, with profits (EPS) expected to jump from Rs. 3.25 to Rs. 8.80 almost immediately after the IPO and Reserves to surge toward Rs. 1.97 billion, a massive projection. This gap suggests that while the company is currently stable and asset-rich, its future value depends on successfully using the new IPO funds to scale operations and capture more market share as planned.

Risk Vs. Return:

The Palpa Cement IPO offers a high value return potential balanced against significant industry-specific risks. The primary "Return" hook is the valuation: with an actual net worth of Rs. 132.49, investors are buying into an asset rich company at a 25% discount relative to its par value (Rs. 100). However, the "Risk" lies in the aggressive profit projections and the current "cement glut" in Nepal, where oversupply has squeezed margins for many. The IRN BB+ rating highlights moderate credit risk and stretched liquidity, meaning the company’s success and your return depend heavily on their ability to scale exports to India to meet their ambitious Rs. 8.80 EPS target.