Ongoing debenture issue of "10.25% Global IME debenture 2080/81"; Information that you need to decide whether to invest

Sun, Mar 24, 2019 3:18 PM on Bonds & Debentures, Exclusive, Stock Market,

Company profile

Global Bank Limited was incorporated in 2007 as a “Class A” commercial bank. Today it is known as Global IME Bank (GBIME) after small mergers with seven banking and financial institutions of various classes. GBIME is currently serving Nepali customers through a network of 131 branches, 100 branchless banking units and 133 ATMs as of mid-October 2018. About 51% of the bank’s shares are held by the promoters while the rest (~49%) is held by the public. GBIME’s registered and corporate office is in Kamaladi, Kathmandu. Mr. Mahesh Sharma Dhakal is the Acting Chief Executive Officer of the bank.

GBIME is currently in process of acquiring Hathaway Finance. Their current status is here.

According the unaudited report published for second quarter of FY 2075/75, the bank has reported a rise in the net profit by 25.46% in the second quarter of the fiscal year 2075/76. See the full report here.

Global IME Bank is the joint organization after merger of Global Bank with following Banks and Financial Institutions:

- Reliable Development Bank

- Pacific Development Bank

- IME Finance Limited

- Lord Buddha Finance

- Social Development Limited

- Gulmi Bikas Bank

- Commerz and Trust Bank

According to ICRA Nepal’s assessment, GBIME’s market share was 4.39%, in terms of deposit base, and 4.42%, in terms of credit portfolio, of commercial banks as of mid-October 2018.

Subsidiary companies

- Global IME Capital Limited

- Global IME Laghubitta Bittiya Sanstha Limited

Objectives of the issue:

- Collecting capital necessary for business expansion and increasing investment

- Increasing Supplementary capital of the company

- Fulfilling the goals of the company

About the issue

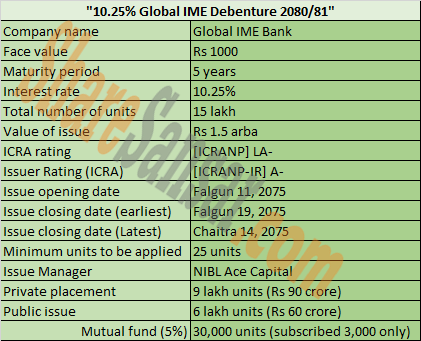

Global IME Bank Limited (GBIME) has issued a debenture scheme, “Global IME Bank Debenture”, with 10.25% into the market. The 15 lakh unit debentures that will mature in 5 years have been floating for the interested investors since Falgun 11, 2075.

General public were able to apply for 5,70,000 unit debentures, 30,000 units for mutual funds and remaining 9 lakh units (60%) for institutional investors. However, the mutual funds applied for 3,000 units only. So the rest is also available for the general investors making it a total of 5,97,000 units.

The general public can apply for minimum 25 units to maximum 75 thousand unit debentures where the per unit cost stands at Rs 1000. The earliest closing date for the issue was set at Falgun 19, 2075 which can be extended till Chaitra 14, 2075.

As a perk of their investment, investors will receive 10.25% semi-annually which will be paid to them from all the branches of the bank. The interested investors can submit their applications from all the branches of the bank as well as from any ASBA member institutions.

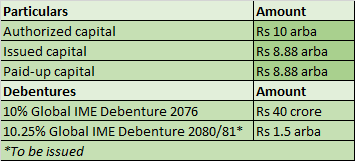

Capital structure

Shareholding composition

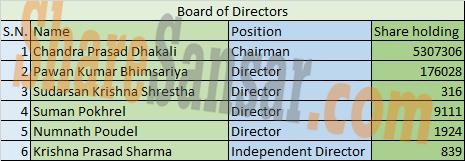

Board of Directors

Management Head

Acting CEO – Mahesh Sharma Dhakal

Academic Qualification – Chartered Accountant

Experience – Nepal Bank Limited

Commerz and trust Bank

Siddhartha Development Bank

Tourism Development Bank

Mega Bank

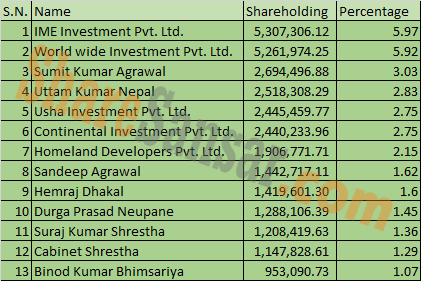

Primary Shareholders

Credit rating

ICRA Nepal has assigned a rating of [ICRANP] LA- (pronounced ICRA NP L A minus) to the proposed NPR 1,500-million subordinated debenture program of Global IME Bank Limited (GBIME). Rating indicates adequate degree of safety regarding the timely servicing of financial obligations. ICRA Nepal has also reaffirmed the rating of [ICRANP-IR] A- (pronounced ICRA NP issuer rating A minus) to the bank, indicating adequate credit quality. The rated entity carries average credit risk.

Strengths and opportunities:

- Adequate track record since 2007 and healthy pace of growth which is partly aided by a series of mergers and acquisitions.

- Good position in the market with a share of ~4.4% in industry credit and deposits as of mid-October 2018.

- Stand-alone growth in the last three years (ending mid-July 2018) was slightly below that of the industry (~19% against ~21%), with a focus on following prudent risk management practices and ensuring adequate controls. This remains a positive from a rating perspective.

- Gradually improving asset quality as well as the sizeable share of retail/SME loans (~58%)

- Adequate earnings profile on an increased asset base, notwithstanding some moderation in recent periods due to the rising cost of deposits.

- Incremental growth prospects could be driven by its diversified franchise and experienced management team along with requisite support from the proposed capital enhancement.

- Portfolio growth of ~23% in the three years ending mid-July 2018, against the industry average of ~21%. However, this was partly supported by multiple acquisitions during this period.

- The yields remained supported by a good proportion of retail/SME loans (~58% as of mid-October 2018) with the rest being corporate loans. This resulted in relatively low credit concentration risks with the top 20 borrower groups accounting for ~16% of the portfolio as on mid-October 2018.

Weaknesses and Threats

- Increase in cost of funds compared to the industry with a sharp spike in recent periods.

- In terms of deposit mix and cost in the last two years, GBIME witnessed a relatively higher spike in deposit costs than industry.

- High share of term deposits compared to the industry reflected in its cost of deposits of 7.23% for Q1 FY 2019 (6.53% for industry). This could impact the bank’s competitive positioning, apart from pressurizing its net interest margins (NIMs).

- High deposit concentration, despite some recent moderation.

- Systemic risks emanating from the mismatch in credit and deposit growth in the industry over the last few years along with the aggressive growth strategy followed by some banks after the regulations induced sharp capital increment from FY 2016 to FY 2017.

- Current capitalization profile (CRAR of 11.27% as of mid-October 2018) is just marginally above the regulatory minimum of 11%. This, however, would be supported after the proposed issue.

- Declining industry deposit growth rate in recent periods and the bank’s tightening CCD ratio.

Source: ICRA Nepal (https://icranepal.com/releases.php)

Financial performance

Conclusion

The issue for Global IME debenture had opened from Falgun 11, 2075. The early closing date was on Falgun 19 but due to under-subscription, the date has been extended till Chaitra 14, 2075.

According to the assessments we have done, apart for the risks inherent in the industry Global IME seems to be in a fairly comfortable position. Given the current volatile interest rates market debentures can be a way to hedge interest rate risks.

The banks are raising and declining the rates in frequent intervals and in such situation the debentures provides stable return. Along with Global IME, the NMB bank is also currently issuing 10 years’ debenture. Similarly, Sunrise Bank has also received approval from Securities Board of Nepal (SEBON) and will soon be opening applications.

Source: Company Prospectus and ICRA Nepal