National development banks touch the mark of 2 kharba in deposit and loan portfolio; Muktinath Bikas Bank leads in six out of ten indicators

Sun, Nov 18, 2018 11:12 AM on Exclusive, Stock Market, Latest,

Highlights:

- Muktinath Bikas Bank Limited leads among the national level development banks

- The overall deposit collection exceeds loan portfolio of national level development banking industry by 1.13 times

- The overall industry marks a net profit of Rs 90.29 crores in the first quarter

There are 11 National level B categorized development banks in the country. In the previous fiscal year, the number of national level development banks remained inconsistent throughout the year. Banks such as Tourism Development Bank Limited, NIDC Development Bank Limited, Kamana Bikas Bank, Sewa Bikas Bank, Mahalaxmi Bikas Bank, Yeti Development Bank, Gandaki iks Bank, Fewa Bikas Bank, Lumbini Bikas Bank, Vibor Society Development Bank, Om Development Bank, etc either went into merger or acquisition or initiated a joint transaction.

All these banks have published their first quarter financial reports and thus, the article provides an analysis on their financial status.

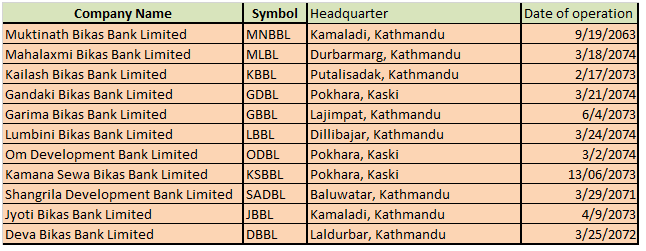

The listed national level development banks are:

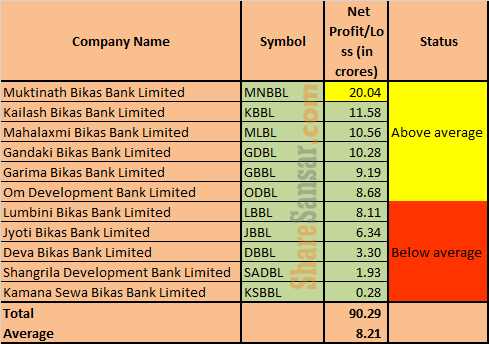

Net profit:

As per the net profit of first quarter of 2075/76, Muktinath Bikas Bank Limited (MNBBL) is in the lead with a profit of Rs 20.04 crores. Similarly, Kailash Bikas Bank Limited (KBBL) has the second highest net profit of Rs 11.58 crores in the same quarter. In the third position, Mahalaxmi Bikas Bank Limited (MLBL) has the net profit of Rs 10.56 crores. The bank with the least net profit is Kamana Sewa Bikas Bank (KSBBL) whose net profit amounts to Rs 28 lakhs.

The industry average net profit of national level development bank stands at Rs 8.21 crore. Six of these banks have net profit above industry average whereas five of them have below average. The national development banking industry made a net profit of Rs 90.29 crores in the first quarter.

(Please download and study the image in case of difficulty upon studying).

Paid up capital:

The central bank of the country has directed these national level “B” categorized banks to meet the paid up capital requirement of at least 2.50 arba. Among the eleven national level banks, Lumbini Bikas Bank Limited (LBBL) is yet to meet the paid up capital requirement. The bank with highest paid up capital are Mahalaxmi Bikas Bank Limited (MLBL) with Rs 2.84 arba capital, Garima Bikas Bank Limited (GBBL) with Rs 2.79 arba paid up capital and Gandaki Bikas Bank Limited (GDBL) with Rs 2.75 arba paid up capital.

As for Lumbini Bikas Bank Limited (LBBL), the bank has paid up capital of Rs 2.17 arba paid up capital. The bank issued auction of an amount worth Rs 3.62 crores for promoter shares. After adjustment of 10% right shares, it will reach to Rs 2.21 arba. To meet the capital requirement of Rs 2.50 arba, it should further hike its capital by Rs 29 crores (around 13%).Thus, investors are in an expectation of bonus shares from the bank. The paid up capital structure of Jyoti Bikas Bank Limited (JBBL) might change after acquiring Hamro Bikas Bank Limited. Similarly, the paid up capital of Deva Bikas Bank Limited (DBBL) might also change after acquiring Western Development Bank Limited and Sahara Bikas Bank Limited.

(Please download and study the image in case of difficulty upon studying).

Reserve and surplus:

As each and every development bank adopted different paid up strategy, the impact is seen in the reserve and surplus fund of these banks. In terms of reserves and surplus, Lumbini Bikas Bank Limited (LBBL) has maintained its lead with a reserve and surplus of Rs 1.23 arba. Kailash Bikas Bank Limited (KBBL) has maintained second position with Rs 1.21 arba reserve and surplus fund. Muktinath Bikas Bank Limited (MNBBL) has a reserve of Rs 1.15 arba. The bank with least reserve and surplus is Jyoti Bikas Bank Limited (JBBL) having a reserve of Rs 35 crores.

The industry average for reserve and surplus is Rs 84 crores.

(Please download and study the image in case of difficulty upon studying).

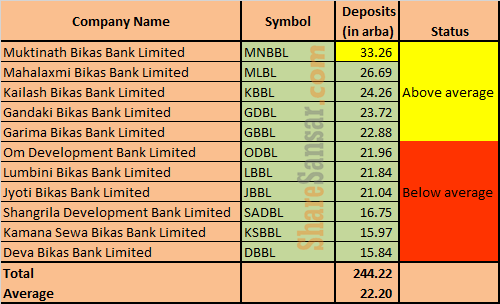

Deposit collection:

In the banking sector, the deposit collection will play a major role in the upcoming days. All the banks except Lumbini Bikas Bank have the same range of paid up capital which is equal or above Rs 2.50 arba. So, the national level development banks will go through a severe competition with each other in order to attract the deposit clients. As of the first quarter of FY 2075/76, Muktinath Bikas Bank Limited (MNBBL) stands on top with total deposits worth Rs 33.26 arba. Similarly, the bank is followed Mahalaxmi Bikas Bank Limited (MLBL) and Kailash Bikas Bank Limited (KBBL) with the collected deposit of Rs 26.69 arba and Rs 24.26 arba respectively. Deva Bikas Bank (DBBL) has the lowest deposit collection of Rs. 15.84 arba only.

The average deposit collected by national development banking industry stands at Rs 22.20 arba. The effect of liquidity crisis is seen among these banks as well since six of the banks have their deposit below industry average.

(Please download and study the image in case of difficulty upon studying).

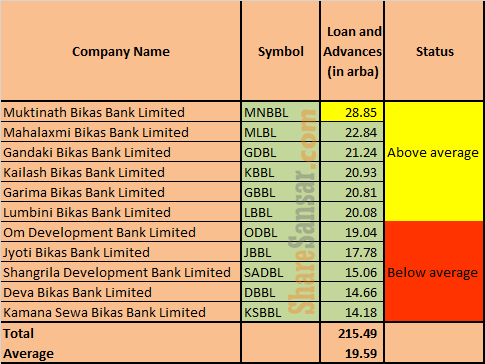

Loans and advances:

With paid up capital of almost same ranges, competition among development banks implies even in bringing the loan clients. As shown in the figure, the top position in loans and advances is occupied by Muktinath Bikas Bank (MNBBL) with credit disbursement worth Rs 28.25 arba. Mahalaxmi Bikas Bank (MLBL) has a loan and advances portfolio of Rs. 22.84 arba. Gandaki Bikas Bank Limited (GDBL) has the loan portfolio of Rs 21.24 arba. Similarly on the other end of the rope, stands Kamana Sewa Bikas Bank (KSBBL) with the lowest loan and advances portfolio of Rs. 14.18 arba.

The industry average loan portfolio of national level development banks stands at Rs 19.59 arba. Six of the national level development banks have their loan portfolio above industry average whereas remining have below average. While the deposits of the overall national level development banking industry lies at Rs 2.44 kharba, the overall industry’s loan portfolio is at Rs 2.15 kharba.

(Please download and study the image in case of difficulty upon studying).

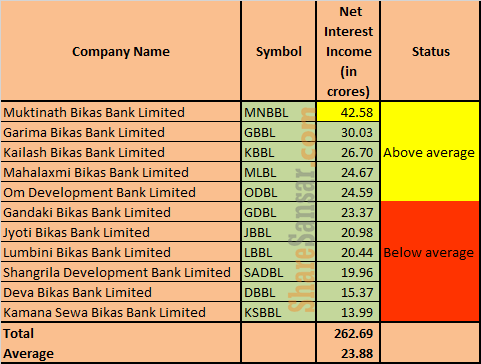

Net interest income:

One of the major source of revenue for banks is its interest income. Muktinath Bikas Bank Limited (MNBBL) has the highest net interest income of Rs 42.58 crores. It is followed by Garima Bikas Bank Limited (GBBL) and Kailash Bikas Bank Limited (KBBL) with net interest income of Rs 30.03 crores and Rs 26.70 crores respectively. The industry average stands at Rs 23.88 crores.

(Please download and study the image in case of difficulty upon studying).

Major indicators:

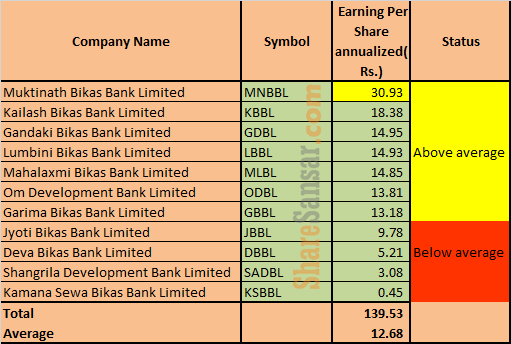

Earnings per share (Annualized):

Earnings per share is presumed to be one of the key factors while undertaking investment decision. Muktinath Bikas Bank (MNBBL) becomes the bank to serve investors with highest annualized EPS of Rs 30.93 per share. Kailash Bikas Bank Limited (KBBL) stands in the second position with annualized EPS of Rs 18.38 per share. Gandaki Bikas Bank Limited (GDBL) has an EPS of Rs 14.95. Kamana Sewa Bikas Bank (KSBBL) stays at the bottom with an earning of Rs. 0.45 per share.

(Please download and study the image in case of difficulty upon studying).

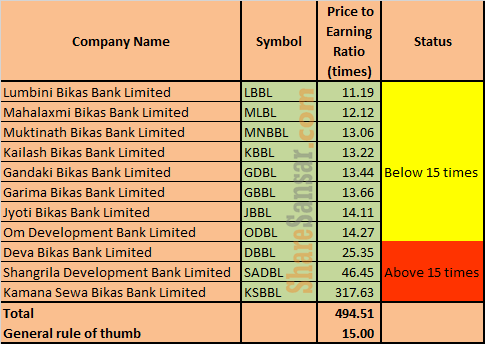

P/E Ratio:

Given that Lumbini Bikas Bank Limited (LBBL) has not met the paid up capital, it has lowest P/E ratio as of 15th November, 2018 i.e. 11.19 times. Among the banks whose paid up capital are met, Mahalaxmi Bikas Bank Limited (MLBL) has least P/E ratio which stands at 12.12 times. Similarly, bank with the next least P/E ratio is Muktinath Bikas Bank limited (MNBBL) i.e. 13.06 times. The P/E ratio of all the national level development banks except three (DBBL, SADBL and KSBBL) are below 15. Since, the general rule of thumb in finance suggest, a P/E ratio below 15 is an adequate price, the national level development banks with P/E ratio below 15 are being traded in the market at a far cheaper price than expected.

(Please download and study the image in case of difficulty upon studying).

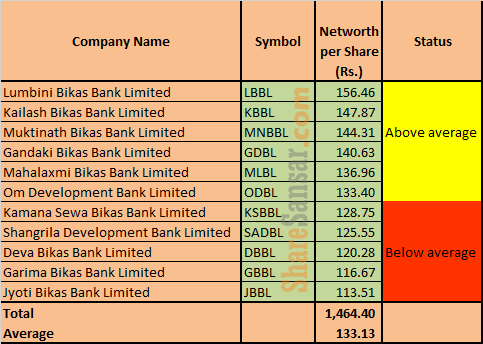

Net worth per share:

The highest net worth per share among these development banks is Rs 156.46 of Lumbini Bikas Bank Limited (LBBL) which has an unmet paid up capital. Kailash Bikas Bank (KBBL) has the second highest net worth per share as of Q1 of FY 2075/76 i.e. Rs 147.87. Jyoti Bikas Bank Limited (JBBL) has the least net worth of Rs 113.51 per share.

The average net worth of national level development banking industry stands at Rs 133.13 where six banks have net worth above average.

(Please download and study the image in case of difficulty upon studying).

Market price:

As of the Last Traded Price (LTP) on 15th November, 2018, Muktinath Bikas Bank Limited (MNBBL) has the highest LTP of Rs 404. It is further followed by Kailash Bikas Bank (KBBL) with a market price of Rs 243. Mahalaxmi Bikas Bank Limited (MLBL) has the market price of Rs 180. Deva Bikas Bank Limited (DBBL) has the least market price of Rs 132.

(Please download and study the image in case of difficulty upon studying).

A full picture:

Finally the table below provides a full picture with major indicators of the 11 national development banks as of the first quarter of FY 2075/76:

(Please download and study the image in case of difficulty upon studying).

From the table above, we can see that Muktinath Bikas Bank (MNBBL) has been able to occupy the top space for 6 indicators out of 10. However, this doesn’t capture the entire picture as there are numerous exogenous factors that must be kept on mind before making any investment decision.

The other issue that needs to come into the light is the fact that Development banks’ paid up capital has been hiked to Rs 2.5 arba, but on the same picture their area of operation is still restricted. Even the monetary policy did not address new provisions for the development banks. Do you think this scenario needs rectification, or do you believe the current area of operations should be enough for the national level development bank? How would you like these banks to perform in the upcoming fiscal year? Which is your choice of investment? Please feel free to drop a comment.