Over view

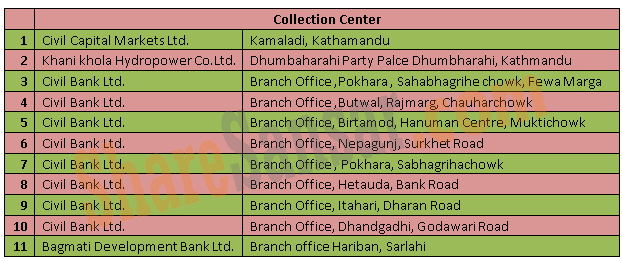

Collection Centre

Company Profile

Khanikhola Hydro power was established in October 2012 by 9 promoters (4 institutional and 5 individual promoters) as a private limited company, Khanikhola Hydropower Company Limited (KHCL) was later converted into public limited company on March 2013 with the objective of facilitating public participation.

The company is developing 4.36 MW Tungun-Thosne Hydropower Project and a 2 MW cascade project namely Khanikhola Hydropower project in Bhattedanda,Sankhu and Ikudol VDCs of Lalitpur district, Central Development Region of Nepal. The project is being developed on Build Own Operate Transfer (BOOT) basis. The project cost estimated at time of financial closure was ~NPR 1079 million to be funded in debt to equity ratio of 70:30.The Company has got a generation license for 35 years which also includes the period of construction.

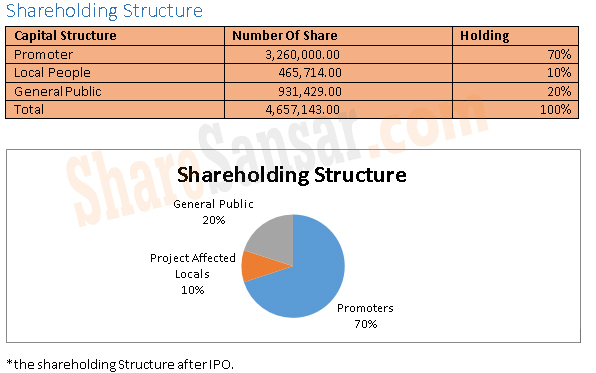

Major promoters include Pashupati Energy Development Company P. Ltd (51.79%), Baidik Hydro Investment Company P. Ltd. (19.80%), Prabhu Bank Limited (11.63%), Swachha Investment P. Ltd (8.97%) and Mr. Mijas Bhattachan(7.67%). Promoters hold 100% of share capital as of now which is planned to be diluted to 70% post the proposed IPO.

A Power Purchase Agreement (PPA) was signed on B.S 2069/04/05(20th July2012) with the Nepal Electricity Authority (NEA). As per the terms of the PPA, the tariff for wet season is NPR 4.8 per kWhr and for dry season is NPR 8.4 per KWhr with 3% escalation for 5 years.

The Power Generation License has been obtained from the Ministry of Energy. Initial Environmental Examination (IEE) report has been approved by the same Ministry

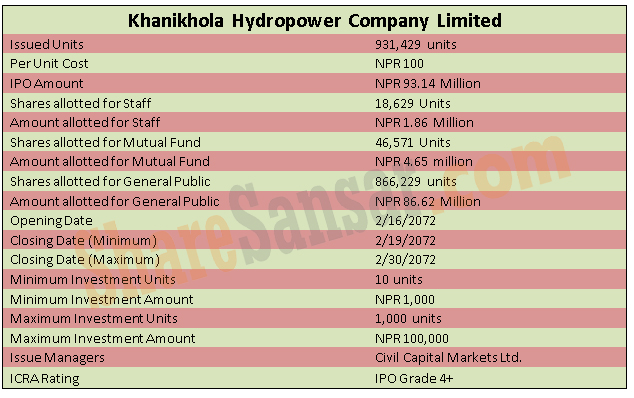

As a part of the IPO process, the company already issued 10% of its post issue paid-up capital amounting to NPR 46.57 million to the local inhabitants of project location in the first tranche and now the company is issuing 20% of the post issue paid up capital amounting to NPR 93.15 million to general public at par value of NPR 100 per share.

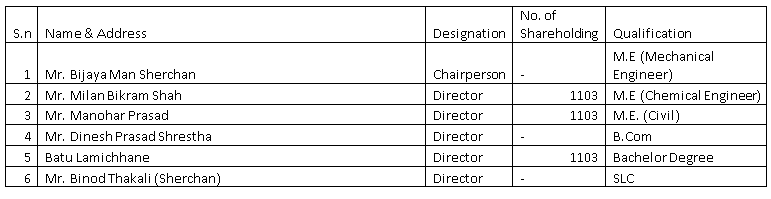

Board of Directors

Financial Analysis

Overall Analysis

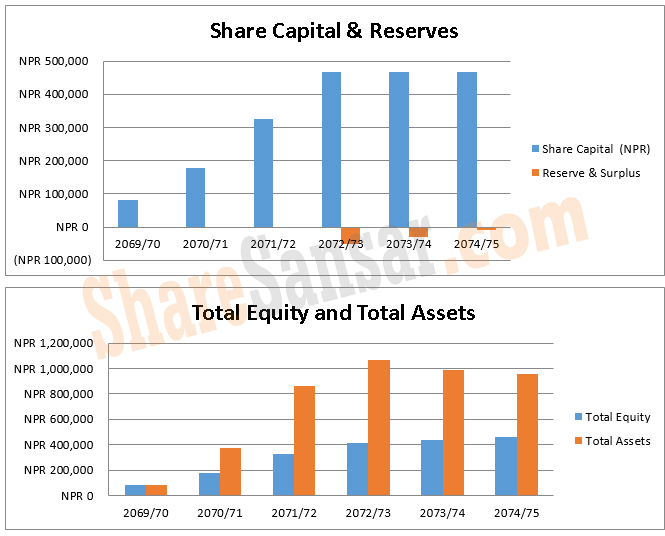

The cost of the project is around NPR 1,178million which is being funded by bank loan of NPR 755 million and balanced through equity of NPR 423 million. Promoters of the hydropower project have already collected NPR 326 million and intend to raise additional NPR 140 million through an IPO. The equity capital is in excess and surplus amount will be utilized to invest in upcoming 14.9 MW project (Mayakhola Hydropower Project) in Sankhuwasabha District. The project is currently under financial closure phase with other initial activities being terminated.

Thus, timely completion within estimated time frame and cost estimate are key factor while assessing the returns generated by this projects. Typically, hydro-power projects entail significant project execution risks as they are located in difficult terrain and hence adverse climatic conditions during the construction period and also geological surprises can disrupt construction schedule of any project. Hence, over the foreseeable future, the return to the shareholders of KHCL is likely to accrue only from the revenue generated by current project.

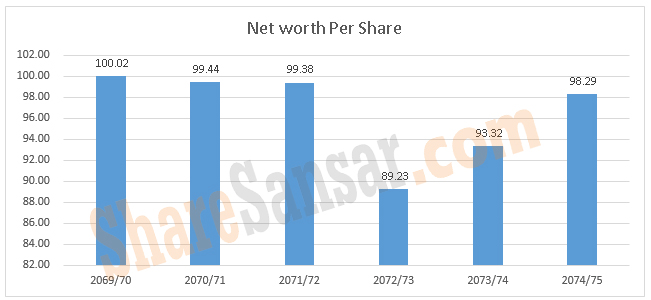

Some stagesof hydroproject construction is still in progress resulting fundamental indicators of the company as substandard as compared to other existing companies. However the financial statements performance indicate favorable and improved results in upcoming year.

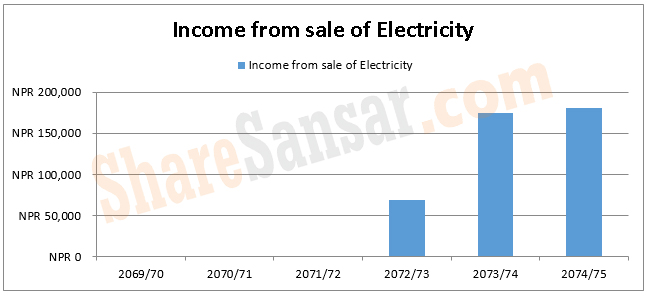

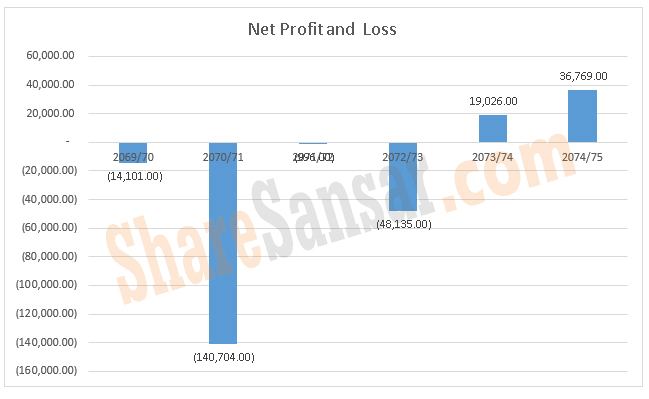

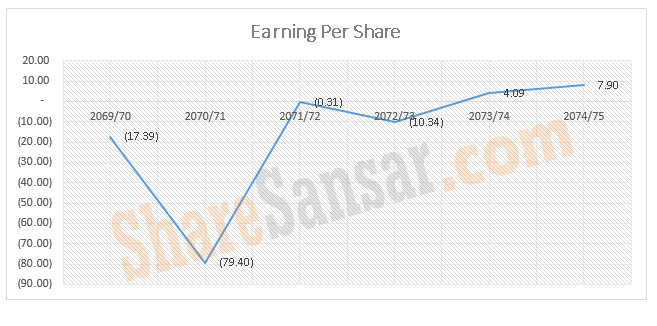

The net profit margin of the hydro project till the end of current FY 2072/73 is negative.But forthcoming years show positive result in net profit.

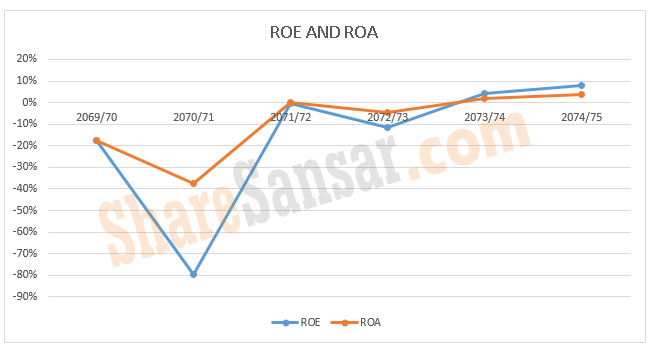

In the FY 2071/72, Return on Equity(ROE) was negative. But it surged to 4.37%in FY 2072/73 and tends to increase by 8.55% in FY 2074/75.The forecasted ROE of the company is still found to be below 10% which is below industry average.

Return on Assets (ROA) till FY 2072-73 is negative. It is expected to reach1.87% and 4.01% in FY 2073/74 and FY2074/75 respectively.

The project is nearing completion and most of the civil works have been completed.

In addition, with a firm PPA in place and positive demand outlook owing to supply-demand gap in the power sector, the tariff and off-take risks are also minimal.In addition, promoters (Including Prabhu Bank among others) have invested substantial equity worth NPR 326 million which is expected to help the company save on its IDC (interest during construction) costs. The project is also entitled to a capital subsidy of NPR 5 million per MW from Government and an additional 10% of the same if it is able to connect to national grid by FY 2017/18.

Going forward, the ability of the company to commission within the time frame and estimated budget and also availability of sufficient hydrology and evacuation infrastructure will be the key parameters which can impact returns of the project.