With price shooting up to circuit level on last trading day over the news of issuance of Further Public Offering of the company, investors are quite confused about what next to do as the trading has been paused with process getting more tangled. What will really happen now is still unknown apart from the abstract opinion. But we definitely know that those investors who have bought shares worth Rs 24 crores approximately will certainly be in panic situation. Though the circumstances aren’t complicated as of yet the signs however are worrisome.

Within the last 16 trading days price has gone up from Rs 3445 to Rs 4488. Such a rise without any significant boost within the company becomes demotivating for investors at times. However it may not yet be time to worry about such things as market is faring quite well specially for the insurance sector till date nevertheless with market being isotopic nothing can be ensured.

| “000” |

2072/73 Q3 |

2070/71 |

2069/70 |

2068/69 |

2067/68 |

2066/67 |

| Paid Up Capital |

1,734,000.00 |

1083750 |

637500 |

375000 |

375000 |

375000 |

| Reserve & Surplus |

728,757.56 |

688989.678 |

689364.061 |

359740.609 |

36854.186 |

34827.639 |

| Life Insurance Fund/Insurance Fund |

28,836,393.74 |

17050813.69 |

12579474 |

9782510.185 |

7653368.402 |

5525319.707 |

| Long Term Investments |

22,098,368.24 |

8811337.013 |

8530378.39 |

7869906.526 |

6175400.386 |

2029430.87 |

As per the third quarter report of 2072/73, paid up capital of the company is 1.73 arba and reserves & surplus currently is at 72.87 crore. As per the reports published by the company the net profit of company till third quarter currently is at 23.8 crore. Point to be noted here is that the real profit of insurance companies comes only after actuary. Besides, net worth per share of NLIC is Rs 149 and earning per share currently is Rs 18.30. The rising capital structure of the company may be viewed as detriment by many of the investors; however, we also must see the institution as a strong and capable institution which can deal effectively during difficult times if any.

| "000" |

2072/73 Q3 |

2070/71 |

2069/70 |

2068/69 |

2067/68 |

2066/67 |

| Total Income |

330,472.34 |

751849.365 |

883381.894 |

729813.531 |

56814.231 |

15749.214 |

| Total Expenses |

92,438.88 |

137737.48 |

108774.846 |

104107.614 |

123190.011 |

9409.234 |

| Net Profit/(Loss) |

238,033.46 |

614,111.89 |

774607.048 |

625705.917 |

-66375.78 |

6339.98 |

Continuing the FPO trend, NLIC though wished to issue its shares at premium price was stopped by the Securities Board last Friday which has received almost unanimous response from the public. Whether or not it is correct to issue at a higher price is subject to detailed investigation, though investors are finding it almost irrational. It’s not that investors aren’t interested in the issue nonetheless concern that the issue might be a bit expensive seems to be realistic. Just by selling slightly above 30 lakhs units of shares the company would be generating more than 8 arba reserves only summing up the premium.

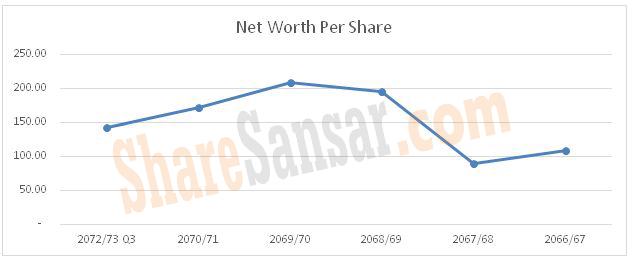

| Ratio |

2072/73 Q3 |

2070/71 |

2069/70 |

2068/69 |

2067/68 |

2066/67 |

| Net worth Per Share(Rs.) |

142.03 |

171.10 |

208.14 |

195.93 |

89.44 |

108.51 |

| Earning per share (Rs.) |

18.30 |

56.74 |

121.51 |

166.85 |

(17.70) |

1.69 |

The fact that market value individually cannot be relied upon as a benchmark for determining premium is actually a sensible point to consider. As prices in secondary market are prone to manipulation we certainly can sense some irrationality in the FPO price, however, it crucial to note that NLIC is an ideal company when it comes to life insurance companies in Nepal and the premium will obviously be higher compared to what we have seen as of yet.

Dinesh Singh Mahat

ShareSansar