Fear, Greed, and the Psychology of the Investor

Mon, Jul 6, 2026 12:39 PM on Economy, Stock Market, Recommended, Exclusive,

Markets are not a game of numbers; they are a game of the mind.

“Investing isn’t about beating others at their game. It’s about controlling yourself at your own game.” — Jason Zweig

When we talk about financial markets, we usually discuss price, charts, indicators, volume, news, interest rates, corporate earnings, bonus and rights shares, policy decisions, and economic data. All of these matter. Yet the true depth of the market does not end there. A market is not merely a game of numbers; it is also a game of the human mind. Here it is not only price that moves: hope moves, fear moves, greed moves, regret moves, confidence moves, the pull of the crowd moves, and at times, silently, so does human ego.

Behind every buy order lies an expectation. Behind every sell order lies a reason. One investor sells to lock in profit; another sells out of fear; another sells simply because he sees others selling. One buys because he sees opportunity; another buys out of greed; another buys for fear of missing out. The price movements we see on the screen are, in truth, the combined result of the psychological reactions of thousands of investors and traders.

When a person enters the market, he does not enter with money alone. He brings his dreams, his fears, his experience, his ego, his hopes, his family’s expectations, his past mistakes, his ambitions for the future and, at times, his impatience. To understand investing as a purely mathematical decision is therefore to understand it only in part. Investing is also a test of emotional discipline.

The Market’s Outer Voice and Inner Voice

When the market is rising, the outer voice is intensely seductive. Social media brims with excitement; from tea stalls to online groups, stories of profit are everywhere. “This share will go higher still,” says one. “The bull run has begun,” says another. Someone points to an old all-time high. To the new investor it seems that if he does not enter now, he will miss the opportunity of a lifetime.

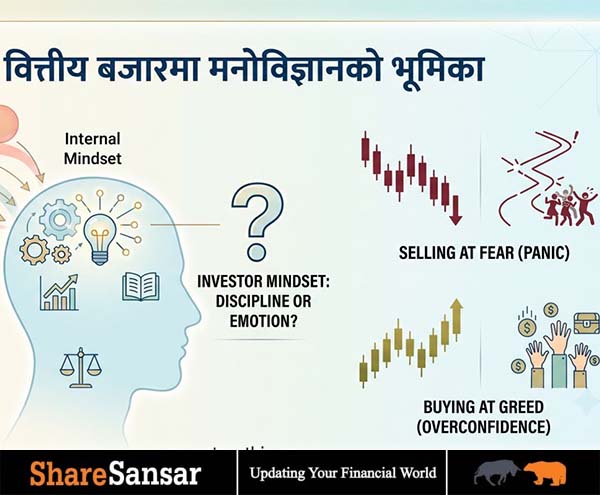

But at that very moment, the inner voice the mind must ask: “Am I buying on the basis of analysis, or merely out of greed because I have watched others profit?” Few pause to ask this question. In the market, heavy losses are often caused not only by choosing the wrong company but also by making decisions driven by emotion.

In the same way, when the market falls, the outer voice fills with fear. The news turns negative. Despair spreads across social media. Those who spoke of “long-term investment” yesterday begin to say “the market is finished” today. At such times, fear enters the investor’s mind: “What if it falls further? What if all my capital is wiped out? Am I too late?” It is this fear that drives many to sell at the weakest moment.

Yet even then the inner voice must ask again: “Am I managing risk, or am I simply running away in panic?” The journey of the successful investor is precisely this struggle between the outer voice and the inner voice.

Fear: A Force That Protects Capital, or a Weakness That Corrupts Judgment?

Fear, in itself, is not a bad emotion. Fear makes a person cautious. An investor with no fear at all may take reckless risks. To protect capital in the market, some measure of fear is necessary. But when fear grows larger than reason, the trouble begins.

In a falling market, fear leads a person to imagine catastrophe rather than to see reality. The price falls by a few percent, yet the loss feels far greater in the mind. Looking at a portfolio drenched in red, the chest grows heavy. The investor opens his phone again and again to check the price. He looks not at the chart but at his loss; not at the structure of the market but at his own pain. It is in this state that judgment fails.

Fear sometimes forces even a good investment to be sold at the wrong time. A company’s long-term fundamentals may be sound and the market’s correction may be ordinary, yet the investor, unable to bear the short-term decline, walks away. Some time later the same price climbs back up, and regret sets in. That regret returns, in the next decision, in the form of greed. In this way, fear and greed give birth to one another endlessly.

Disciplined fear, however, is useful. If an investor has already set his risk limits, placed his stop-loss, sized his position sensibly, and decides according to plan, then that is not fear; it is risk management. Herein lies the difference: emotional fear corrupts judgment, while disciplined caution protects capital.

Greed: A Drive to Seek Opportunity, or an Intoxication That Blinds Us to Risk?

Greed, too, is not wholly bad. A person with no desire to earn a profit never enters the market at all. The wish for financial progress, for building wealth, and for securing the future is natural. But when the desire for profit grows larger than reason, greed becomes an intoxication.

In a rising market, greed swells gradually. At first the investor buys cautiously. As the price rises, confidence grows. When it rises again, he begins to think himself a superb analyst. When it climbs still further, risk seems small and profit seems certain. This is precisely the dangerous state.

Greed makes the investor forget three things: valuation, risk, and plan. He does not consider what the risk–reward ratio is at this price. He does not consider where he will exit if the market turns. He does not consider how much of his capital he is committing to a single stock. He sees only the possibility of profit; the possibility of loss is invisible to him.

Many new investors enter in the market’s final stage, for that is when the story is most attractive. When the price has already climbed very high, the news is at its most positive. When risk has already grown large, confidence is at its peak. This is the irony of the market: when things are cheap, people are afraid; when things are expensive, people are greedy.

Conclusion

The financial market is not merely a game of price, charts, and data; it is also a game of human psychology. Behind every transaction hide emotions such as hope, fear, greed, regret, and the influence of the crowd. The price movements we observe are, in reality, the combined result of the emotional reactions of thousands of investors. When the market rises, the outer voice fills with greed; when it falls, with fear. But the successful investor must be able to ask his inner judgment, amid these outer voices: “Am I deciding on the basis of analysis, or have I been swept away by emotion?”

Neither fear nor greed is wholly bad. Held within discipline, these emotions can be useful; but when they grow larger than reason, they become the cause of corrupted judgment. This, indeed, is the irony of the market: investors are fearful when things are cheap, and greedy when they are dear.

Article By: Ashok Kumar Shah; Author of Master the Technical Analysis (forthcoming)