Company Analysis: Sahayogi Vikas Bank Ltd.

Wed, Nov 4, 2015 4:00 PM on Latest, Exclusive, Featured, Company Analysis,

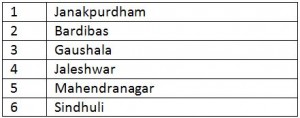

Sahayogi Vikas Bank Limited (SBBLJ) is the 10th Development Bank of Nepal with its Head Office at Vidhyapati Chowk -4, Janakpurdham, Dhanusha. It began commercial operations from 23rd October 2003. The bank has been authorized to conduct operations in 3 districts: Dhanusha, Mahottari and Sindhuli. As of FY 2070/71, the bank had a total of 6 branches.

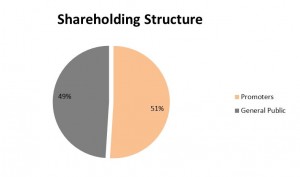

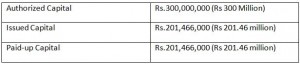

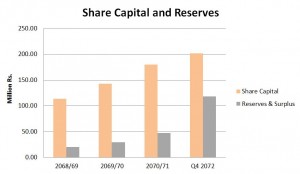

The bank has an authorized capital of Rs.300 Million and issued and paid-up capital of Rs.201.46 million. 51% of the company’s shares are held by its 21 promoters and 49% by the general public.

The company’s reserves have grown to a healthy level of Rs.118.67 million which is more than double the average reserve amount in the 1-3 district development bank category. The company has managed to increase its reserves by 149.06% compared to last year.The company’s total asset size stands at Rs.2.46 billion.

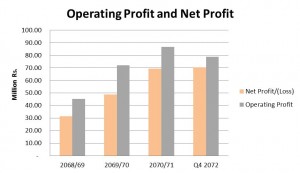

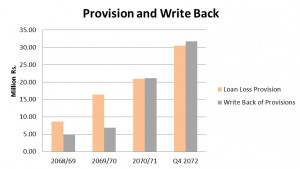

The company earned operating profits of Rs.78.98 million which is 8.79% less than what it earned in the previous fiscal year. The company has had to make large provisions which is the major cause for the decrease in its operating profit. However, the company has managed to write back all of its provisions.

The company’s reserves have grown to a healthy level of Rs.118.67 million which is more than double the average reserve amount in the 1-3 district development bank category. The company has managed to increase its reserves by 149.06% compared to last year.The company’s total asset size stands at Rs.2.46 billion.

The company earned operating profits of Rs.78.98 million which is 8.79% less than what it earned in the previous fiscal year. The company has had to make large provisions which is the major cause for the decrease in its operating profit. However, the company has managed to write back all of its provisions.

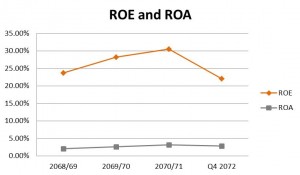

Compared to the previous FY, the company’s net profit only increased marginally by 1.46% from Rs.69.43 million to Rs.70.45 million. The company had managed to grow its net profits by 54.29% in FY 2069/70 and by 42.59% in FY 2070/71. This reduction in profit growth is a cause for concern and is a recurring pattern in other indicators of the company.

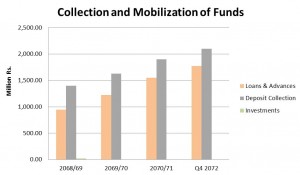

The company’s deposit collection stands at Rs.2.10 billion. This is a growth of 10.35% compared to the previous fiscal year.However, this rate of growth was 16.52% in FY 2069/70 and 16.88% in 2070/71.

Compared to the previous FY, the company’s net profit only increased marginally by 1.46% from Rs.69.43 million to Rs.70.45 million. The company had managed to grow its net profits by 54.29% in FY 2069/70 and by 42.59% in FY 2070/71. This reduction in profit growth is a cause for concern and is a recurring pattern in other indicators of the company.

The company’s deposit collection stands at Rs.2.10 billion. This is a growth of 10.35% compared to the previous fiscal year.However, this rate of growth was 16.52% in FY 2069/70 and 16.88% in 2070/71.

The company’s loan mobilization has also increased by 14.67% from previous year and stands at Rs.1.77 Billion. Here too, the rate of growth has slowed from 26.27% in FY 2070/71 and 30.06% in FY 2069/70.

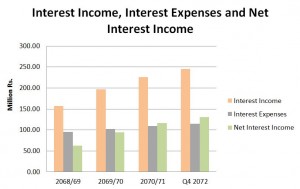

The company’s net interest income grew by 12.54% compared to previous year and stands at Rs.130.973 million. The rate of growth has slowed from previous FY’s 23.52%. This year, the company’s interest income grew by 8.64% while the interest expenses grew by a mere 4.50%.

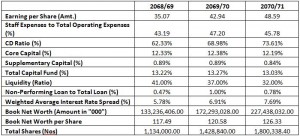

The company’s EPS stands at Rs.34.97. This is a decrease of 28.03% from last year’s Rs.48.59. The EPS decreased due to the increase in the company’s paid up capital through bonus shares and right issue of 26% and 15% respectively. The decrease in EPS is a challenge faced by all BFI’s after the NRB’s decision to raise their paid up capital.

The company’s loan mobilization has also increased by 14.67% from previous year and stands at Rs.1.77 Billion. Here too, the rate of growth has slowed from 26.27% in FY 2070/71 and 30.06% in FY 2069/70.

The company’s net interest income grew by 12.54% compared to previous year and stands at Rs.130.973 million. The rate of growth has slowed from previous FY’s 23.52%. This year, the company’s interest income grew by 8.64% while the interest expenses grew by a mere 4.50%.

The company’s EPS stands at Rs.34.97. This is a decrease of 28.03% from last year’s Rs.48.59. The EPS decreased due to the increase in the company’s paid up capital through bonus shares and right issue of 26% and 15% respectively. The decrease in EPS is a challenge faced by all BFI’s after the NRB’s decision to raise their paid up capital.

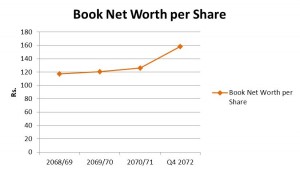

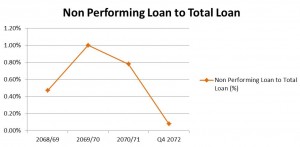

The company’s net worth per share increased by 25.55% this year and stands at a healthy Rs.158.60. Despite high loan loss provisions the bank’s non-performing loan to total loan stands at 0.08% which dropped from an already remarkable 0.78% last year. This shows that the company has done well in managing its risky investments.

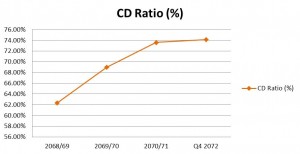

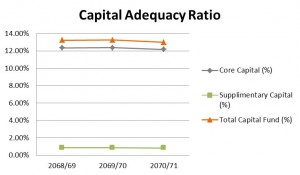

Its Total Capital Fund to RWA stands at 15.07% which is comfortably above the NRB stipulated minimum of 11%, Credit to Deposit ratio is also comfortably within the NRB stipulated maximum of 80%. These indicators show that the bank has plenty of room to extend more credit.

The company’s net worth per share increased by 25.55% this year and stands at a healthy Rs.158.60. Despite high loan loss provisions the bank’s non-performing loan to total loan stands at 0.08% which dropped from an already remarkable 0.78% last year. This shows that the company has done well in managing its risky investments.

Its Total Capital Fund to RWA stands at 15.07% which is comfortably above the NRB stipulated minimum of 11%, Credit to Deposit ratio is also comfortably within the NRB stipulated maximum of 80%. These indicators show that the bank has plenty of room to extend more credit.

Income Statement

Income Statement

Key Ratios

Key Ratios

Capital and Shareholding Structure

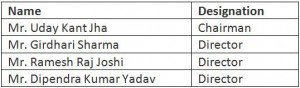

Board of Directors

The current members of the board of directors include:

Branches

Analysis

Overall performance of the bank is above average when compared to other 1-3 district level development banks but its growth has slowed which is a cause for alarm. The company’s paid up capital stands at Rs.201.47 million. This is after a 26% bonus share distribution and 15% rights call.This will further increase to Rs.257.88 million after capitalization of 28% bonus shares declared this year. The size of its paid up capital is markedly higher than the average in its category.

The company’s reserves have grown to a healthy level of Rs.118.67 million which is more than double the average reserve amount in the 1-3 district development bank category. The company has managed to increase its reserves by 149.06% compared to last year.The company’s total asset size stands at Rs.2.46 billion.

The company earned operating profits of Rs.78.98 million which is 8.79% less than what it earned in the previous fiscal year. The company has had to make large provisions which is the major cause for the decrease in its operating profit. However, the company has managed to write back all of its provisions.

Compared to the previous FY, the company’s net profit only increased marginally by 1.46% from Rs.69.43 million to Rs.70.45 million. The company had managed to grow its net profits by 54.29% in FY 2069/70 and by 42.59% in FY 2070/71. This reduction in profit growth is a cause for concern and is a recurring pattern in other indicators of the company.

The company’s deposit collection stands at Rs.2.10 billion. This is a growth of 10.35% compared to the previous fiscal year.However, this rate of growth was 16.52% in FY 2069/70 and 16.88% in 2070/71.

The company’s loan mobilization has also increased by 14.67% from previous year and stands at Rs.1.77 Billion. Here too, the rate of growth has slowed from 26.27% in FY 2070/71 and 30.06% in FY 2069/70.

The company’s net interest income grew by 12.54% compared to previous year and stands at Rs.130.973 million. The rate of growth has slowed from previous FY’s 23.52%. This year, the company’s interest income grew by 8.64% while the interest expenses grew by a mere 4.50%.

The company’s EPS stands at Rs.34.97. This is a decrease of 28.03% from last year’s Rs.48.59. The EPS decreased due to the increase in the company’s paid up capital through bonus shares and right issue of 26% and 15% respectively. The decrease in EPS is a challenge faced by all BFI’s after the NRB’s decision to raise their paid up capital.

The company’s net worth per share increased by 25.55% this year and stands at a healthy Rs.158.60. Despite high loan loss provisions the bank’s non-performing loan to total loan stands at 0.08% which dropped from an already remarkable 0.78% last year. This shows that the company has done well in managing its risky investments.

Its Total Capital Fund to RWA stands at 15.07% which is comfortably above the NRB stipulated minimum of 11%, Credit to Deposit ratio is also comfortably within the NRB stipulated maximum of 80%. These indicators show that the bank has plenty of room to extend more credit.

Capital Plan

According to the capital plan published by the company, the bank plans to issue 28% bonus shares from the earnings of FY 2071/72, 25% from the earnings of FY 2072/73 and 13% from the earnings of FY 2073/74. The bank also plans to merge with Janaki Finance Company Ltd. in FY 2073/74 which will increase the paid up capital of the company to Rs.768.7 million. This will set the bank well above the new paid up capital requirement set by the NRB of Rs.500 million for 1-3 district level development bank.Merger/ Acquisition Prospects

The company plans to merge with Janaki Finance Company Ltd. in FY 2073/74. Although negotiations are in place no formal agreement has been signed. Janaki finance is a 1-3 district level finance company with a current paid up capital of Rs.310.78 million (includes 25% bonus shares announced this year) . It has its headquarters in Janakpurdham, Dhanusha and operates in Dhanusha, Mahottari and Siraha districts. After the company’s merger with Janaki Finance, the bank will have operations in Dhanusha, Mahottari, Siraha and Sindhuli districts. According to the company’s secretary, the bank plans to stay a 1-3 district level development bank. The bank is negotiating with NRB to operating in 4 districts even though it is licensed to operate in only 3.For investors

The company’s earnings have grown consistently in the past but there are signs that this growth will not be as impressive in the future. Having said that, in absolute measure, the bank’s figures are still well above average when compared to other 1-3 district level development banks. The bank distributed dividends of 26% bonus shares and 8.5% cash in FY 2069/70, 26% bonus shares and 10% cash in FY 2070/71 and plans to distribute 28% bonus shares from the earnings of FY 2071/72. It also plans to distribute 25% bonus shares from the earnings of FY 2072/73 and 13% bonus shares from the earnings of FY 2073/74. The bank’s last traded price (as of November 2nd, 2015) was Rs.425. This indicates a PE ratio of 12.15 times and PB ratio of 2.68 times. These show that the company’s stock is moderately valued. Dhanusha and Mahottari, two districts in which the bank operates have been heavily affected by the ongoing Terai unrest. Continuous bandhs, closures and agitations coupled with fuel shortages and boarder closures have severely disrupted all economic activity in the region. The company’s performance is sure to be hampered and investors will need to be patient with the company’s 1st quarter reports of the current fiscal year.Financial Highlights

Balance Sheet

Income Statement

Key Ratios