Company Analysis: ILFCO, Is ILFCO Really Worth Buying?

Fri, Oct 9, 2015 5:16 PM on Latest, Exclusive, Featured, Company Analysis, Stock Market,

International Leasing and Finance Company Ltd. (ILFCO) was established as a joint venture finance company with the Korean Industrial Leasing Co., Ltd. (KILC) which later became Korea Development Bank Ltd. KDB Capital Corporation is the largest leasing company in the Republic of Korea and one among the top three largest leasing companies within the Asian Continent. It has been participating in the management of ILFCO through the provision of technical know-how as a foreign partner since the very inception of the company.

ILFCO states its prime objective as “providing the people of the nation with creative financing alternatives of international standards”. It has been continuously rendering a variety of financial services according to the needs of the Nepalese people since its establishment.

The company was established on December 11, 1994 and began operations as a C class financial institution from October 31, 1995. The company’s head office is located in New Baneshwor, Kathmandu.

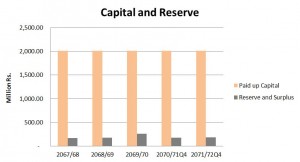

The company has a paid-up capital of Rs.2.008 Billion and has a total of 9 branches.

The company had an operating profit of Rs.241.96 million in FY 2068/69 and it increased to Rs.266.27 million in FY 2069/70. However, the company had an operating loss of Rs.82.65 million in FY 2070/71 because the company’s loan loss provisions increased astronomically by 31358.88% from Rs.0.81 million in FY 2070/71 to Rs.255.75 million in FY 2071/72. The company managed to make an operating profit of Rs.152.98 million in FY 2071/72.

The company’s net profits have been decreasing throughout our review period. It decreased from Rs.150.63 million in FY 2067/68 to Rs.102.7 million in FY 2071/72. The company suffered a loss of Rs.83.27 million in FY 2070/71.

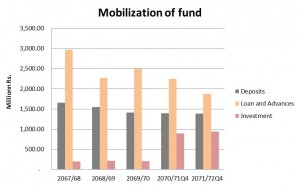

The company’s deposit collection has also decreased throughout our review period from Rs.1.7 billion in FY 2067/68 to less than Rs.1.4 billion in FY 2071/72. The company’s loan mobilization has also decreased from almost Rs.3 billion in FY 2067/68 to Rs.1.38 billion in FY 2071/72. The loan mobilization of the company decreased by 16.58% in FY 2071/72 compared to the previous fiscal year.

However, the company has managed to increase its investments of Rs.209 million in FY 2069/70 to Rs.895 million in FY 2070/71. This is an increase of 326.52%. As of FY 2071/72, the company’s total investments stand at Rs.895.22 million.

The company had an operating profit of Rs.241.96 million in FY 2068/69 and it increased to Rs.266.27 million in FY 2069/70. However, the company had an operating loss of Rs.82.65 million in FY 2070/71 because the company’s loan loss provisions increased astronomically by 31358.88% from Rs.0.81 million in FY 2070/71 to Rs.255.75 million in FY 2071/72. The company managed to make an operating profit of Rs.152.98 million in FY 2071/72.

The company’s net profits have been decreasing throughout our review period. It decreased from Rs.150.63 million in FY 2067/68 to Rs.102.7 million in FY 2071/72. The company suffered a loss of Rs.83.27 million in FY 2070/71.

The company’s deposit collection has also decreased throughout our review period from Rs.1.7 billion in FY 2067/68 to less than Rs.1.4 billion in FY 2071/72. The company’s loan mobilization has also decreased from almost Rs.3 billion in FY 2067/68 to Rs.1.38 billion in FY 2071/72. The loan mobilization of the company decreased by 16.58% in FY 2071/72 compared to the previous fiscal year.

However, the company has managed to increase its investments of Rs.209 million in FY 2069/70 to Rs.895 million in FY 2070/71. This is an increase of 326.52%. As of FY 2071/72, the company’s total investments stand at Rs.895.22 million.

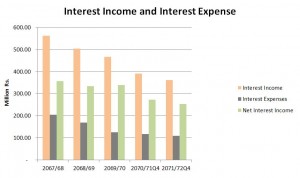

The company’s net interest income has also been in a decreasing trend throughout our review period. It decreased from Rs.356.42 million in FY 2067/68 to Rs.253.05 million in FY 2071/72. This is a decrease of almost Rs.100 million in the company’s primary earnings in just 5 years.

The company’s net interest income has also been in a decreasing trend throughout our review period. It decreased from Rs.356.42 million in FY 2067/68 to Rs.253.05 million in FY 2071/72. This is a decrease of almost Rs.100 million in the company’s primary earnings in just 5 years.

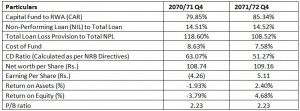

The company’s net worth per share has been hovering between Rs.113 and Rs.108 throughout our review period and stands at Rs.109.16 as of Q4 2072. The company’s non-performing loan to total loan stands at 14.52% which is well beyond the NRB stipulated limit of 5% .Its RWA is at an astounding 85.34% which indicates that a large majority of the company’s loans are risky and could default. Additionally, the high riskiness of the company’s investments also means that it has to allocate a large amount for provisions which can further lower the company’s profitability.

The company’s net worth per share has been hovering between Rs.113 and Rs.108 throughout our review period and stands at Rs.109.16 as of Q4 2072. The company’s non-performing loan to total loan stands at 14.52% which is well beyond the NRB stipulated limit of 5% .Its RWA is at an astounding 85.34% which indicates that a large majority of the company’s loans are risky and could default. Additionally, the high riskiness of the company’s investments also means that it has to allocate a large amount for provisions which can further lower the company’s profitability.

The company has a total of just 9 branches which is considerably low considering the nature of the business and the high capital it has. Additionally 5 of the branches are inside Kathmandu valley and only 4 are outside Kathmandu.

The bank has not been able to hold its AGM for the last 2 years. This shows a lack of corporate discipline in the organization.

The company has a total of just 9 branches which is considerably low considering the nature of the business and the high capital it has. Additionally 5 of the branches are inside Kathmandu valley and only 4 are outside Kathmandu.

The bank has not been able to hold its AGM for the last 2 years. This shows a lack of corporate discipline in the organization.

Profit and Loss

Profit and Loss

Key Ratios

Key Ratios

*All data of FY 2070/71 and FY 2071/72 have been taken from the company’s 4th quarter reports of the respective fiscal years as the annual report for those two years have not been published.

*All data of FY 2070/71 and FY 2071/72 have been taken from the company’s 4th quarter reports of the respective fiscal years as the annual report for those two years have not been published.

Capital Structure and Shareholding Structure

Board of Directors

The current members of the board of directors are:

Analysis

An analysis into the company’s fundamentals shows that the company is in a dire state. The company’s reserves and surplus is dangerously low and stands at Rs.183.92 million as of Q4 2072. The company’s earning per share has stayed below Rs.10 throughout our review period and stands at Rs.5.11 now. This is well below the industry average.

The company had an operating profit of Rs.241.96 million in FY 2068/69 and it increased to Rs.266.27 million in FY 2069/70. However, the company had an operating loss of Rs.82.65 million in FY 2070/71 because the company’s loan loss provisions increased astronomically by 31358.88% from Rs.0.81 million in FY 2070/71 to Rs.255.75 million in FY 2071/72. The company managed to make an operating profit of Rs.152.98 million in FY 2071/72.

The company’s net profits have been decreasing throughout our review period. It decreased from Rs.150.63 million in FY 2067/68 to Rs.102.7 million in FY 2071/72. The company suffered a loss of Rs.83.27 million in FY 2070/71.

The company’s deposit collection has also decreased throughout our review period from Rs.1.7 billion in FY 2067/68 to less than Rs.1.4 billion in FY 2071/72. The company’s loan mobilization has also decreased from almost Rs.3 billion in FY 2067/68 to Rs.1.38 billion in FY 2071/72. The loan mobilization of the company decreased by 16.58% in FY 2071/72 compared to the previous fiscal year.

However, the company has managed to increase its investments of Rs.209 million in FY 2069/70 to Rs.895 million in FY 2070/71. This is an increase of 326.52%. As of FY 2071/72, the company’s total investments stand at Rs.895.22 million.

The company’s net interest income has also been in a decreasing trend throughout our review period. It decreased from Rs.356.42 million in FY 2067/68 to Rs.253.05 million in FY 2071/72. This is a decrease of almost Rs.100 million in the company’s primary earnings in just 5 years.

The company’s net worth per share has been hovering between Rs.113 and Rs.108 throughout our review period and stands at Rs.109.16 as of Q4 2072. The company’s non-performing loan to total loan stands at 14.52% which is well beyond the NRB stipulated limit of 5% .Its RWA is at an astounding 85.34% which indicates that a large majority of the company’s loans are risky and could default. Additionally, the high riskiness of the company’s investments also means that it has to allocate a large amount for provisions which can further lower the company’s profitability.

The company has a total of just 9 branches which is considerably low considering the nature of the business and the high capital it has. Additionally 5 of the branches are inside Kathmandu valley and only 4 are outside Kathmandu.

The bank has not been able to hold its AGM for the last 2 years. This shows a lack of corporate discipline in the organization.

Merger/ Acquisition Prospects

ILFCO is not a very attractive company in terms of its fundamentals. Having said that, the paid up capital of Rs.2 billion, ILFCO has is a very attractive prospect for other larger banks to merge with or acquire this company. Banks with strong fundamentals and proven management abilities can merge with or acquire ILFCO at a relatively cheap price and increase their paid up capital by Rs.2 billion.Company's Fundamentals

Balance Sheet

Profit and Loss

Key Ratios

*All data of FY 2070/71 and FY 2071/72 have been taken from the company’s 4th quarter reports of the respective fiscal years as the annual report for those two years have not been published.