While NESDO Sambridha Laghubitta is Preparing to Issue Its IPO, This is How the Rating Agency ICRA Nepal Evaluates It

Mon, Jun 7, 2021 4:44 PM on Latest, IPO/FPO News,

ICRA Nepal has assigned the issuer rating of [ICRANP-IR] BB+ (pronounced ICRA NP Issuer Rating Double B plus) to NESDO Sambridha Laghubitta Bittiya Sanstha Limited (NSLBSL). Issuers with this rating are considered to have a moderate risk of default regarding timely servicing of financial obligations.

About the Company

Incorporated in April 2018 (in CRO), NESDO Sambridha Laghubitta Bittiya Sanstha Limited (NSLBSL), started operations from March 2019, as a licensed national level class-D MFI. After its licensing, NSLBSL took over the microfinance business being conducted by National Education and Social Development Organization, NESDO Nepal (NESDO), an NGO established in June 1995 and operating as a financial intermediary since November 2000.

NESDO Sambridha Laghubitta Bittiya Sanstha Limited has appointed Global IME Capital as issue manager to float its 8.28 lakh ordinary shares to the general public, its employees, and different mutual funds.

The agreement was signed between the Executive chair of the microfinance Mr. Biswo Prakash Prasai and the CEO of the capital Mr. Paras Mani Dhakal.

Shareholding Structure

The shareholding structure of NSLBSL consists of NESDO Nepal, NGO as a promoter (~70%) along with Prabhu Bank Limited (~7%), and the rest being held by 81 individuals as of mid-January 2021. The registered and corporate office of NSLBSL is located at Kushma-6, New Road, Parbat.

Company Strengths

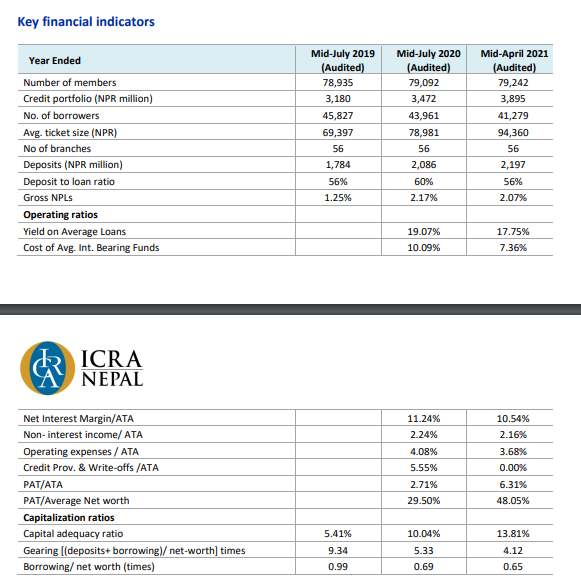

The assigned rating factors in the long track record of NSLBSL in the microfinance institution (MFI) sector (between 2000 and 2019 under the aegis of the promoter, National Education & Social Development Organization (NESDO), and since 2019 as NRB licensed class-D MFI) and its adequate branch network (56 branches in 17 districts as of mid-April 2021). The rating also takes comfort from the company’s strong capitalization profile (~13.8% as of mid-April 2021 against the regulatory minimum requirement of 8%), which is expected to improve further after the proposed initial public offering (IPO).

Furthermore, healthy profitability with return on net worth (RoNW) of ~29.5% and return on assets (RoA) of 2.71% in FY2020 supported by healthy net interest margins (NIMs) remains a positive from the standpoint of the company’s ability to generate internal capital. The rating also derives comfort from the healthy share of deposit in the funding mix (~84% as of mid-April 2021), which renders stability to the funding profile and cost of the fund. Further, a large below-poverty-line population in Nepal, the target group for MFIs, and the experienced management team of the company remain rating positives.

Key credit strengths

1) Adequate track record of operations and experienced management team

2) Strong capitalization profile and low gearing ratio

3) Decent portion of external funding from member deposits

4) Healthy profitability profile supported by strong NIMs, lower credit cost and scale economies

Company Challenges

Nonetheless, the rating is constrained by the incremental concerns about the company’s asset quality with the impact of Covid-19 on the marginalized borrowers. Amid the ongoing pandemic, the company’s NPLs have increased to 2.17% as of mid-July 2020 and 2.07% as of mid-April 2021 from 1.25% as of mid-July 2019. NSLBSL also has a limited track record as a regulated class-D MFI (despite a long track record as a financial NGO or FINGO) and its ability to maintain its performance and asset quality under the regulated framework remains to be seen.

Rating concerns also arise from the company’s geographical concentration risk with ~42% of the credit portfolio concentrated to the top three districts as of mid-April 2021. ICRA Nepal also notes the regulatory changes capping the MFI’s lending rate at 15% and fees at 1.5% for FY2021. This could impair the company’s profitability profile in the event of increased borrowing cost, which currently remains low because of comfortable liquidity in the banking sector. The recent regulatory restriction in collecting recurring pension deposits could mute the future deposit growth and deteriorate the deposit-to-loan ratio and increase the MFI’s reliance on external borrowings, which also remains a rating concern.

Key Credit Challenges

1) Moderate asset quality

2) Geographical concentration risk

3) Low penetration of credit bureau in Nepalese MFI sector; risk of overleveraged borrowers remains high

4) Regulatory risk

Company's financial performance

NSLBSL reported a net profit of ~NPR 98 million in FY2020 on an asset base of ~NPR 3,836 million as of mid-July 2020 against a net profit of ~NPR 78 million over an asset base of ~NPR 3,379 million as of mid-July 2019. Further, it reported a profit after tax of ~NPR 195 million in Q3 FY2021 over an asset base of ~NPR 4,672 million as of mid-April 2021.

NSLBSL’s gross NPLs stood at 2.07% and CRAR at 13.81% as of mid-April 2021 (2.17% and 10.04%, respectively as of mid-July 2020). On the technology front, NBLBSL uses Uranus, a web-based online software, which is centralized across all its branches.

Wrapping Up

Going forward, NSLBSL’s ability to reduce the geographical concentration of its portfolio, maintain its asset quality as well as increase its scale of operations and develop a commensurate control mechanism will have a bearing on its profitability and overall financial profile. The company’s ability to build an adequate capital cushion to withstand probable credit shocks will also remain a key rating sensitivity.