What is the biggest hurdle for NEPSE? Know the factors that will change NEPSE's direction

Thu, May 31, 2018 6:03 AM on Financial Analysis, Stock Market, Economy, Exclusive, Latest,

-Krishna Khatiwada

Three years back when our economy was hit at the core by earthquake and border blockade, NEPSE was booming. When it hit an all-time high of 1888 points on 27th July 2016, the turnover stood at Rs 2.1 arba whereas turnover on 30th May 2018 is only Rs 43.90 crores, with NEPSE index hovering at 1,322 and these figures are very disappointing.

Why are investors demoralized to invest in Nepal's stock market although stock market is one of the best wealth creating instruments in developing countries?

In Nepal, there are three major investment sectors viz. real estate, fixed deposit and securities market (stock, bond, mutual funds etc.). Capital flows majorly in these three sectors and when one instrument performs better than the remaining two, people will flock to that sector. Currently in Nepal, finance sectors are not balanced. The high level of competition and low liquidity in this sector has led the interest rates to rise rapidly.

Fixed deposits are considered safe (though there is some risk) than stock market. So it’s obvious that the one who is taking extra risk by investing in the stock market will seek for extra reward. But the situation here is different—investors are not getting returns even equivalent to the fixed deposit by taking extra risk in stock market. Average yield of commercial banks in Q3 of 2074/2075 is around 5% in stock market which is very less than the returns that commercial banks pay for keeping the money safely in fixed deposits. Many investors who are involved in market with the loans have gone bankrupt and the one who have survived are definitely not looking to stay longer as interest rates on loans are soaring and the market return is very low. Thus, these factors are building negative sentiment in people towards stock market.

How does interest rate affect NEPSE?

The interest rates and NEPSE index is inversely related, i.e. when interest rate paid by banks increases, NEPSE index turns downward.

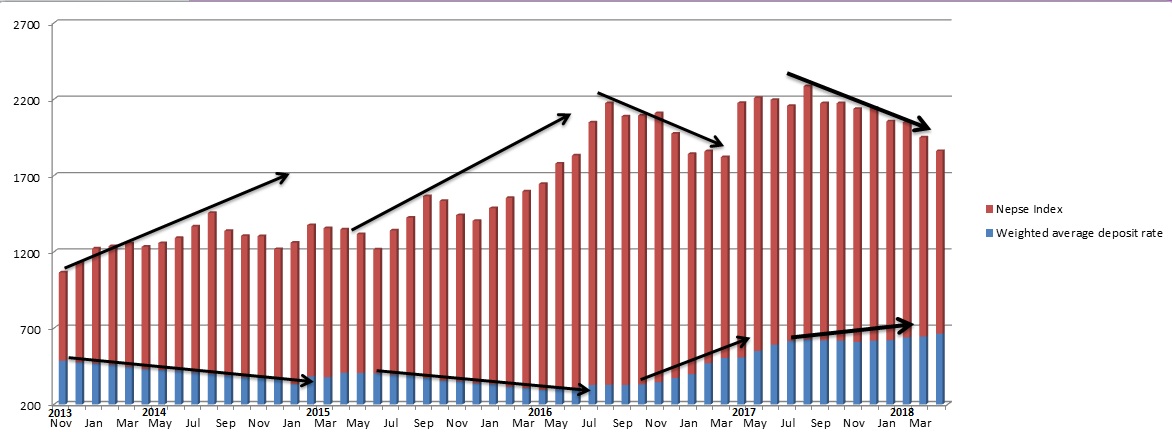

Graph below shows the relationship between average weighted deposit rate and NEPSE Index. The average weighted deposit rate is multiplied by 100 for effective comparision.

Average weighted deposit rates are the average interest paid by banks on fixed deposits and savings. As you can see in the graph, in the last 4 years whenever AWDR (blue) moves downward, NEPSE (Red) starts uptrend and when it increases, NEPSE starts downtrend.

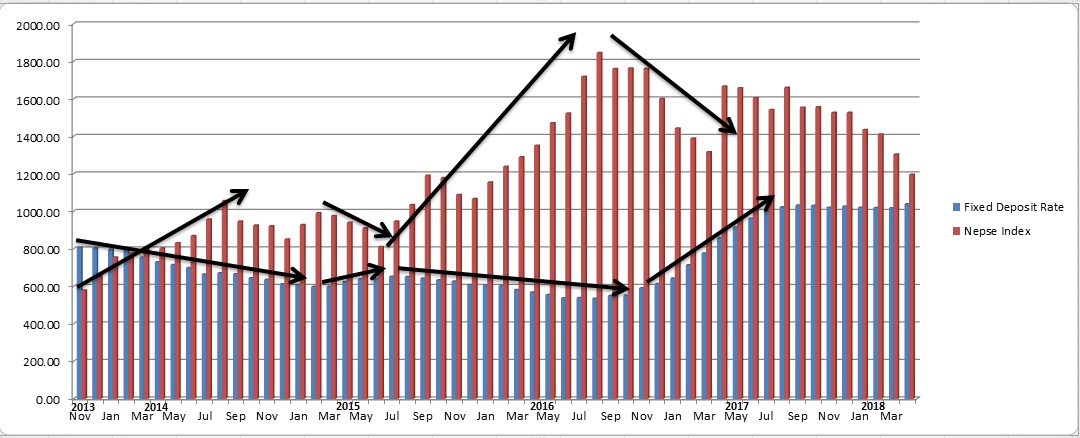

Here is another graph which shows relation between fixed deposit rates (blue) which is multiplied by 100 and NEPSE (red).

As you can see above, fixed deposit rates and NEPSE index are related inversely, so when one decreases other increases and vice versa. We often look at other indicators but ignore these important macro indicators of the market.

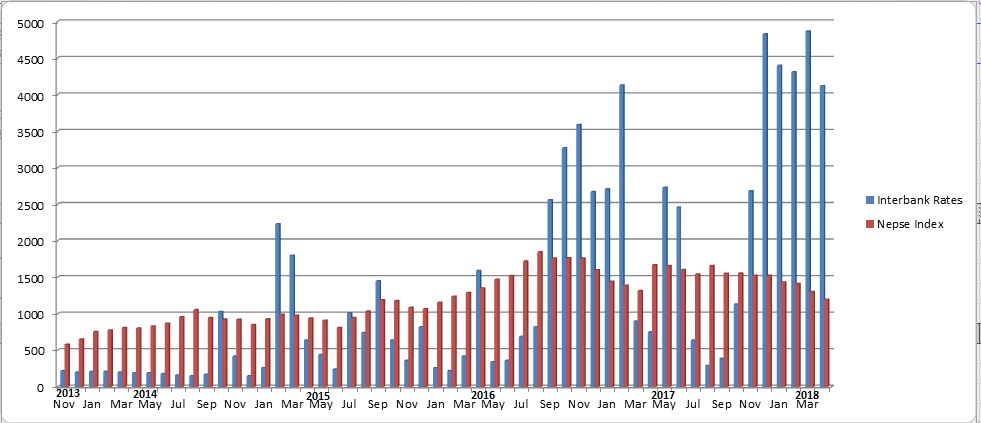

The most interesting relation is between the interbank interest rates (blue) which is multiplied by 1000 and NEPSE index (red). Graph below shows the same.

Inter-banking rate is important indicator to understand liquidity in the banking sector and interbank loans are usually given for very short period of time. High interbank lending rate indicates that there is more demand for liquid capital, which means most of the banks are in the need of cash. High interbank rates are a sign of low liquidity in the market.

With low liquidity, capital flow in the market decreases which eventually leads to a downward movement of the market. Interbank rates are revised every single month. From the graph above, we can observe that whenever interbank rate was above 0.50%, NEPSE index has turned downward and in the last five months, interbank rate was above 4%.

In 2018, Romania’s and Turkey’s interbank rate has increased rapidly which resulted in downward market movement of these countries. So, interbank rate is one of the major indicators for predicting overall market trend. We often look at the micro-economical factor and ignore banking rates' impacts on stock market.

What happens to institutional investors in stock market when bank's interest rates increase?

Retail investors brings small amount of money in stock market, which has little impact on market. When institutional players like insurance companies, mutual funds, banks, EPF, CIT and others equity funds get involved in market, it creates larger impact because the capital they bring in market will be in billions. Mutual funds can invest majority of their fund in capital market whereas other institutional investors are allowed to invest some percentage of their total fund. If we add all institutional investors, the total capital they could bring to the Nepal stock market exceeds few kharba but the tragedy is that the average daily turnover in NEPSE in last one year has ranged between Rs 30 to 60 crores only. This means that institutional investors are not interested in the stock market. Institutional investors operate on public capital and they have to pay customers their principal amount with returns.

At current situation, if they invest their capital in stock, it means that they are taking more risk for low returns whereas they could easily get predefined returns of 11% with larger margin of safety in banks. As a result of high interest rates, most of the mutual funds in Nepal are keeping more than 50% of their capital in banks, which is not their core work. With this argument, we can say institutional investors are less likely to get involved in market as long as the banking interest rates are high.

Whenever interbank and fixed deposit rates have increased, NEPSE has turned negative. So, for the growth of Nepse, interest rates must decrease.

We have discovered few factors that can increase liquidity in domestic market which can reduce overall banking interest rates.

- Growth in Per-capita income: Nepal’s per-capita income is now around Rs 1,09,296 which had grown by 15.39% (increased by around Rs 14,000) this year. Currently, Nepal’s population stands at 2.95 crores, which means National income has increased hugely by Rs 4.13 arba. High per-capita income increases consumer spending power and that can increase the liquidity in the market.

- Political Stability: Nepal has gone through many years of political uncertainty, and changing government’s policies has discouraged many domestic and foreign investors in Nepal. Now the government is looking firm which may result in some degree of political stability in the country. Stable politics and policies attract many investors across the globe which can increase capital flow in the country.

- Periodic capital expenditure by government: With firm government, capital expenditure will be periodical as well as effective. When government was unstable most of the expenditure were done at the 11th hour. Previous data suggests that government of Nepal disbursed around 40% of their capital expenditure in first ten months and remaining 60% in last two months of the year. Periodic expenditure creates stable cash flow in the market.

- Growing banking sectors: NRB had urged banking & finance sectors to open new branches in rural areas. As a result, the number of branches for all BFIs has increased to 5,848 in Chaitra 2074 from 4,272 in Chaitra last year. Commercial banks have added a total of 715 new branches in the period of last one year. This initiative of NRB gave an easy accessibility of banking system to rural people which can bring savings from their home to the bank as keeping money in a bank is safer and generates interest on money. This can help in increasing liquidity in the market.

- Foreign Direct Investments: Government of Nepal is taking necessary steps for encouraging FDI, some of the policies have been revived and many sectors are opened for foreign investors where they can invest 100% or can start a joint venture with domestic company. Banks in Nepal are now connecting with international banks as NRB has approved borrowing from foreign banks. All these measures are encouraging foreign investors in the country which ultimately increases liquidity in the market.

When banks change interest rates on deposit, they also change loan rates keeping their net interest spread almost unaltered, so banks get least affected by changing interest rates. When interest rates changes, it’s the common people who get affected.

If interest rate goes below the average annual return of NEPSE then there will be greater flow of capital in the stock market, which will change NEPSE’s downward track to uptrend.