Union Life Insurance Given "BBB" Rating by ICRA Nepal; This is What it Means

Fri, May 21, 2021 2:32 PM on Stock Market, Latest,

ICRA Nepal has assigned the issuer rating of [ICRANP-IR] BBB (pronounced ICRA NP Issuer Rating triple B) to Union Life Insurance Company Limited (ULICL). Issuers with this rating are considered to have a moderate degree of safety regarding timely servicing of financial obligations.

Company Profile

Union Life Insurance Company Limited (ULICL) is a public limited life insurance company (LIC), operating since July 2017. Its head office is in New Baneswor, Kathmandu. The company has an equity investment of multiple business houses in Nepal such as Jagadamba group, Golchha Organization, Gadiya group, Neupane group, Rajesh Hardware group & Tibrewala Group.

Company Ownership

As of mid-July 2020, the major shareholders of ULICL include, Mr. Shekhar Golcha (~19.9%), Mr. Sahil Agrawal (~19.9%) Mr. Sulav Agrawal (~18%), Mr. Sandip Kumar Agrawal (~6.6%), Mr. Rahul Kumar Agrawal (~6.6%), and Mr. Sharad Kumar Tibrewala (~6.6%) among others.

The authorized capital of the company is NRs. 215 crore. The promoters have contributed 70% of this, amounting to NRs. 150.50 Crore whereas Nepalese citizens can contribute NRs. 64.50 Crore to the remaining 30% of this capital via the IPO.

Company Performance

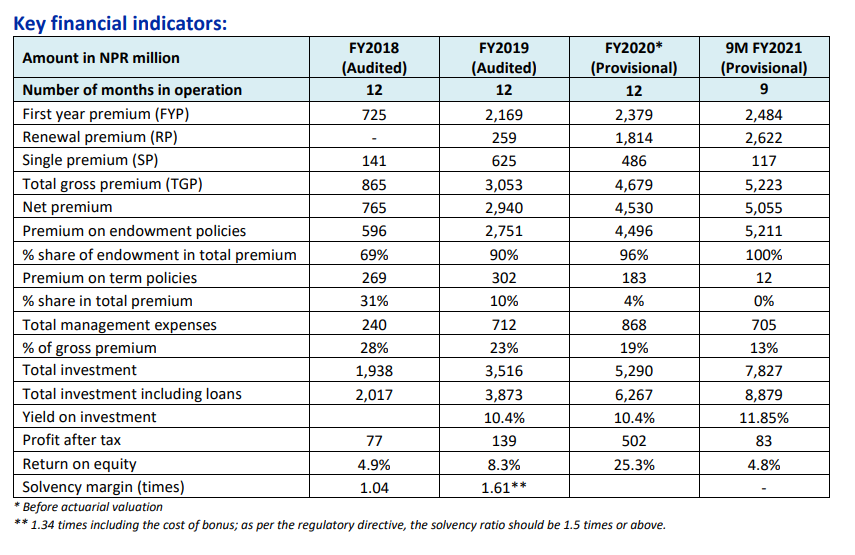

The company reported a profit after tax of ~NPR 83 million during 9M FY2021 on a total asset base of NPR 10,141 million as of mid-April 2021.

The assigned rating factors in ULICL’s strong franchise network (202 branches across the country as of mid-April 2021) and robust agency channel developed over a short time span which has helped the company scale up its operation vis-a-vis other new age players. This coupled with endowment dominated business with a good persistency ratio, strong promoter group support and an experienced senior management team augur well for future business growth. Low penetration of the insurance sector in Nepal also offers growth potential to new players like ULICL. The rating also takes into consideration adequate quality of investment portfolio with decent returns, and the company’s adequate reinsurance arrangements, including catastrophic provisions, which provide comfort to its claims-paying ability and its ability to maintain solvency in the event of catastrophic events.

Company Strength

These are the key rating strengths of the company according to ICRA Nepal:

1) Adequate branch and agency network, experienced management and ownership

2) Product mix dominated by endowment products; good policy continuation rate

3) Adequate reinsurance arrangement

4) Progressive profitability supported by investment earnings

Company Challenges

In contrast, these are the key rating challenges of the life insurance company:

1) Limited track record and therefore untested underwriting controls

2) Suboptimal solvency profile

3) Impact of ongoing Covid-19 pandemic in the Life insurance industry

The rating agency has stated that the rating remains constrained by ULICL’s limited track record of underwriting performance. Likewise, the management’s ability to achieve sustainable growth amid intense competition remains to be seen. The rating also remains constrained by the fragmented nature of the industry and increasing competition (19 LICs in Nepal). Business disruptions caused by the Covid-19 triggered lockdown and its expected impact on the earnings and claims of the insurance industry could also exacerbate the solvency concerns, which remains a key rating challenge. A probable increase in claims amid the outbreak of the second wave of the covid-19 pandemic would also remain key monitorable.