The Engine of the Economy: Unleashing the Potential of SMEs in Nepal

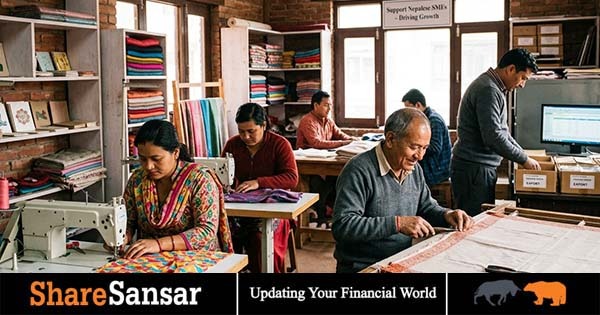

For a developing economy like Nepal, Small and Medium Enterprises (SMEs) are not just a peripheral sector; they are the very backbone of the nation’s economic stability and growth. From local handicraft workshops in the Kathmandu Valley to modern agro-processing units in the Terai, SMEs are the primary drivers of job creation, poverty alleviation, and export potential.

However, despite their immense promise, the tale of the Nepalese SME is often one of struggle. To truly understand the landscape, we must look at the data driving this sector, uncover the root causes behind their high mortality rate, and explore actionable measures to protect and propel them forward.

The Critical Role of SMEs in Nepal: By the Numbers

SMEs are vital to establishing an inclusive, resilient economy in Nepal. The data highlights exactly how heavily the nation relies on these businesses:

- Gross Domestic Product (GDP) Contribution: According to studies by the United Nations Economic and Social Commission for Asia and the Pacific (UN ESCAP), SMEs contribute approximately 22% to Nepal’s GDP.

- Employment Generation: The SME sector is the largest employer in the country outside of traditional agriculture. It generates an estimated 1.75 to 1.8 million jobs. Furthermore, cottage and small industries account for over 80% of total industrial employment, making them invaluable for empowering marginalized groups and women.

- Export Dominance: SMEs account for a massive share of Nepal's export manufacturing potential. Sectors like carpets, pashmina, tea, handicrafts, and aromatic plants are almost entirely driven by small and medium operators.

Why Do SMEs in Nepal Fail? (The Barriers to Success)

Despite their economic importance, many Nepalese SMEs operate in a survival state rather than a growth state. Several critical bottlenecks explain why these businesses often fail to scale or ultimately collapse:

- The "Missing Middle" in Financing

The International Finance Corporation (IFC) estimates Nepal's SME finance gap to be around US $3.6 billion, with 44% of SMEs reporting access to finance as a major constraint. Banks rely heavily on fixed real estate collateral, which many small business owners do not have. Even when loans are secured, high interest rates can quickly cripple a business's cash flow.

- Poor Cash Flow and Financial Mismanagement

Many SMEs operate as inherited family businesses with traditional management practices. A lack of financial literacy leads to poor cash flow management. Delayed payments from buyers, combined with a lack of cash reserves, mean that even profitable businesses can run out of money to cover day-to-day operations.

- The Brain Drain and Skill Shortages

With hundreds of thousands of young Nepalese migrating abroad for employment, domestic market demand has shrunk, and SMEs face a severe shortage of skilled labor. Businesses struggle to find trained personnel in technology, manufacturing, and modern marketing.

- Bureaucratic Red Tape and Regulatory Hurdles

SMEs often find themselves bogged down by complex licensing requirements, unclear regulations, and burdensome tax compliance. Policy instability—where incentives granted by one piece of legislation are repealed by another—creates an uncertain environment that discourages long-term investment.

- Isolation and Market Access Constraints

Without proper integration into Global Value Chains (GVCs), Nepalese SMEs struggle to reach international markets. Domestically, they face fierce price competition from cheaper, mass-produced imported goods. Logistical barriers, such as poor rural-to-urban transport networks, further increase their operational costs.

Controlling Measures: A Blueprint for SME Success

To transform the SME sector from a vulnerable demographic into a robust engine of national prosperity, targeted interventions are required from both the government and the private sector.

- Shift to Cash-Flow and Project-Based Financing:

The financial sector, guided by the Nepal Rastra Bank (NRB), must transition from collateral-centric lending to cash-flow and project-based financing. Expanding alternative credit scoring models and properly funding concessional export credit schemes will directly address the $3.6 billion finance gap.

- Simplify Compliance and Bureaucracy:

The government should implement a true "single-window" system for business registration, licensing, and tax filing. Simplifying tax structures specifically for micro and small enterprises will encourage informal businesses to enter the formal economy without the fear of overwhelming administrative burdens.

- Invest in Capacity Building and Technology:

Public-Private Partnerships (PPPs) should be leveraged to provide SMEs with training in digital literacy, modern accounting, and quality control. Helping SMEs adopt basic accounting software and e-commerce platforms can drastically improve their cash flow management and market reach.

- Develop Targeted Export Subsidies:

To help Nepalese SMEs compete globally, the government must provide streamlined, easily accessible cash export subsidies. Assisting SMEs in acquiring international quality certifications will also allow them to export high-value goods like pashmina, herbs, and handicrafts to premium markets like the European Union.

- Strengthen Infrastructure and Logistics:

Investing in reliable electricity, better road networks, and efficient customs clearance processes will drastically reduce the overhead costs for SMEs, allowing them to price their goods more competitively against foreign imports.

Conclusion

Small and Medium Enterprises are the true engines of innovation and common prosperity in Nepal. While the challenges of financing, talent retention, and bureaucratic red tape are significant, they are not insurmountable. By recognizing their value and implementing targeted, supportive policies, Nepal can safeguard its SMEs, ensuring they not only survive but thrive to drive the nation's economic future.

Article By:

Anuj Shrestha

MBA Student, Pokhara University