Snow River IPO Opens Today; Should You Invest in This Hydro? Take a Closer Look

Tue, May 12, 2026 8:21 AM on Company Analysis, Financial Analysis, National, Latest,

Snow Rivers Limited is a power producing company that operates the Super Kabeli Khola, A Hydropower Project. Located in the Taplejung District of eastern Nepal, the project uses the natural flow of the Kabeli and Amji rivers to generate electricity.

Unlike many companies that ask for investment while still building, this project is already finished and fully functional. It began officially selling electricity to the national power grid on Poush 05, 2081.

The facility has a total capacity of 13.5 Megawatts. The Super Kabeli Khola A Hydropower Project (SKKAHPP) is a Run-of-River (RoR) type hydropower project located in Sirijangha Rural Municipality, Wards No. 7 and 8 (formerly Yamphudin and Kheban VDCs), Taplejung District, Mechi Zone, Koshi Province, Nepal. The project site lies approximately 253 km northeast (aerial distance) of Kathmandu. Kabeli Khola, on which the project is developed, is a major tributary of the Tamor River.

Board of Directors:

|

S.N. |

Name of Directors |

Designation |

Appointment Date (B.S.) |

|

1 |

Mr. Mohan Bikram Karki |

Chairman |

2082/01/26 |

|

2 |

Mr. Uttam Paudel |

Director |

2082/09/07 |

|

5 |

Mr. Santosh Bhattarai |

Independent Director |

2079/08/22 |

|

6 |

Ms. Dipa Rana Magar |

Female Director |

2080/05/27 |

|

7 |

Mr. Prakash Shrestha |

Independent Director |

2081/07/29 |

About the Issue and Rating:

Snow Rivers Limited has received an upgraded credit rating of [ICRANP-IR] BB+ from ICRA Nepal, moving up from its previous "BB-" status. This rating indicates that the company has a "moderate risk" regarding its ability to pay back its financial debts on time. The upgrade is a positive signal for investors, reflecting the company’s transition from a construction phase project to an active, electricity generating business since late 2024.

|

Particulars |

Details |

|

|

Total Units for General Public |

7,78,125 Units |

|

|

Price per Share |

Rs. 100 (Face Value) |

|

|

Opening Date |

Baisakh 29, 2083 (May 12, 2026) |

|

|

Early Closing Date |

Jestha 01, 2083 (May 15, 2026) |

|

|

Late Closing Date |

Jestha 12, 2083 |

|

|

Issue Manager |

Sanima Capital Limited |

|

|

Credit Rating |

[ICRANP-IR] BB+ (Moderate Risk) |

|

|

Project-Affected Locals |

9,37,500 Units |

Already Allotted |

|

Foreign Employed Nepalis |

93,750 Units |

Already Allotted |

|

Mutual Funds |

46,875 Units |

Reserved |

|

Company Employees |

18,750 Units |

Reserved |

|

General Public |

7,78,125 Units |

Opening Baisakh 29 |

Financial Ratio

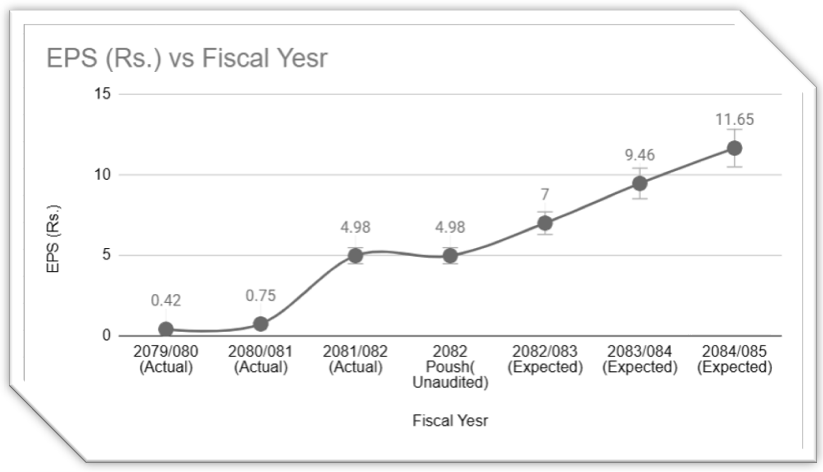

Earning Per Share:

The company’s Expected Earning Per Share is too much high then it’s actual Earning Per Share. It’s actual EPS till Poush end was Rs. 4.98 and it’s expected EPS is RS. 11.65 in next two year. Company’s EPS was 0.42 in the F.Y. 2079/80 and it gains only around Rs. 4 in 2 years. If everything is favourable for the company then it can achieve it’s expected EPS else it’s growth compare to the market average will be low or moderate.

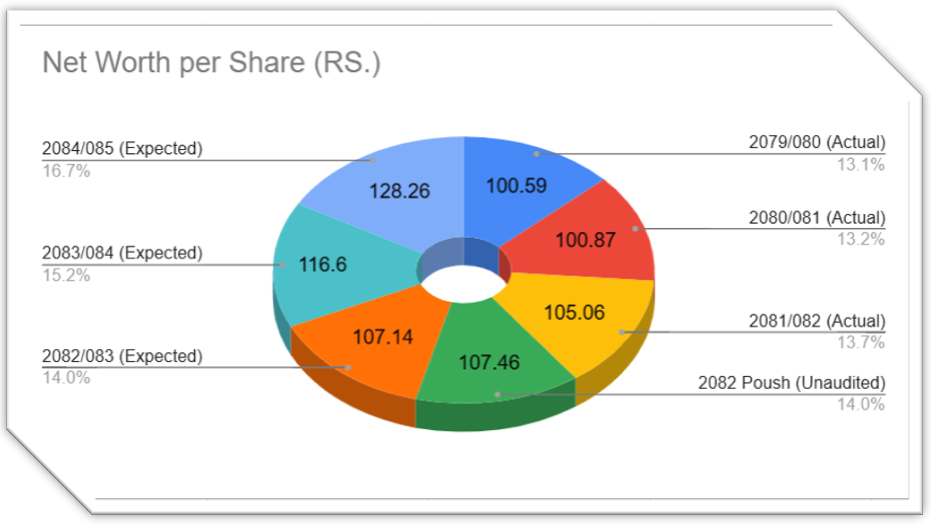

Net Worth Per share:

Snow Rivers Net Worth Per Share for the F.Y. 2079/80 was Rs. 100.59 and it’s current net worth per share till Poush end was 107.46. The company’s IPO is issued at par value this shows company is giving it’s Initial Offering in discount price of RS. 7. It’s expected net worth per share is achievable because Snow River already started it’s production and running smoothly, Most of the Hydro companies raise money for the construction of the project but this one already started making money for the investor. The company expects it’s NWPS to be Rs. 128.26 at the end of F.Y. 2084/85, which seams achievable for the company.

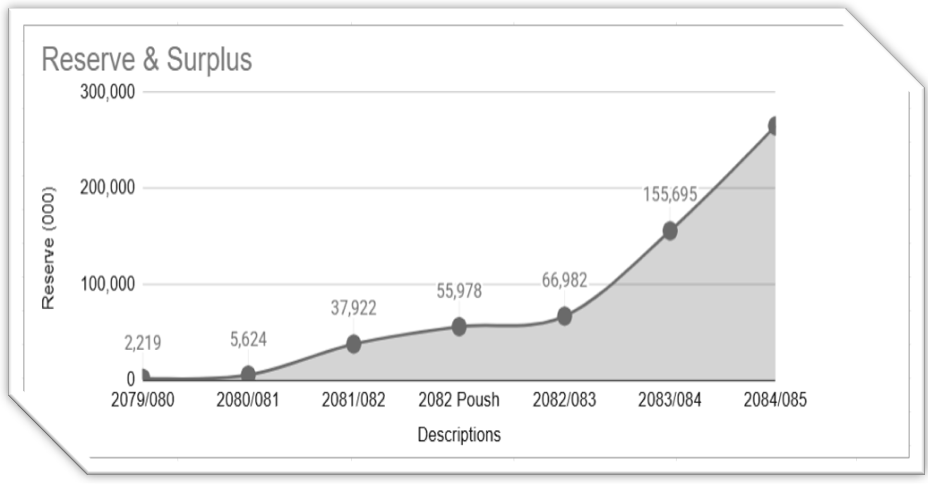

Reserve and Surplus:

It’s been more than around 1 Years since the company completed it’s construction and started selling electricity to the national power grid. The company’s account shows that it reserves around Rs. 37,922,000 (3.79 Crore) in the previous F.Y. 81/82. The company expected it’s Reserve and Surplus to grow from 3.97 Crore to more than 20 crore in next two years. It’s not high expectation for the Hydro companies because Government is also prioritizing the Hydro sector for the economy boost that helps to reach $100 Billion economy in next 5 years.

Financial Highlight:

| Actual | Expected | ||||||

| Particulars | 2079/080 | 2080/081 | 2081/082 | 2082 Poush (Unaudited) | 2082/083 | 2083/084 | 2084/085 |

| Total Non-Current Assets (Rs. '000) | 915,871 | 2,278,215 | 2,586,348 | 2,543,605 | 2,608,596 | 2,520,251 | 2,432,102 |

| Total Current Assests (Rs '000) | 225,657 | 210,828 | 214,418 | 215,871 | 199,499 | 279,147 | 295,176 |

| Total Assets (Rs. '000) | 1,141,529 | 2,489,043 | 2,801,166 | 2,759,476 | 2,808,095 | 2,799,398 | 2,727,278 |

| Total Equity (Rs. '000) | 379,477 | 650,000 | 750,000 | 750,000 | 937,500 | 937,500 | 937,500 |

| Total Non-Current Liability (Rs.'000) | 550,707 | 1,613,642 | 1,921,576 | 1,869,692 | 1,719,830 | 1,622,455 | 1,515,553 |

| Total Current Liability (Rs. '000) | 212,125 | 219,776 | 91,668 | 83,806 | 83,783 | 83,783 | 9,330 |

| Total Liability & Equity (Rs. '000) | 1,141,529 | 2,489,043 | 2,801,166 | 2,759,476 | 2,808,095 | 2,799,398 | 2,727,278 |

| Paid-up Capital (Rs. '000) Before IPO | 376,477 | 650,000 | 750,000 | 750,000 | - | - | - |

| Paid-up Capital (Rs. '000) After IPO | - | - | - | - | 937,500 | 937,500 | 937,500 |

| Reserves & Funds (Rs. '000) | 2,219 | 5,624 | 37,922 | 55,978 | 66,982 | 155,695 | 264,895 |

| Total Net Worth (RS.'000') | 378,696 | 655,624 | 787,922 | 805,978 | 1,004,482 | 1,093,159 | 1,202,395 |

| No. of Shares ('000) | 3,765 | 6,500 | 7,500 | 7,500 | 9,375 | 9,375 | 9,375 |

| Net Profit / (Loss) (Rs. '000) | 1,588 | 3,405 | 33,074 | 49,635 | 65,639 | 88,678 | 109,236 |

| Return on Net Worth (%) | 0.42% | 0.52% | 4.20% | 6.16% | 6.53% | 8.11% | 9.08% |

| Paid-up Capital Per Share (Rs.) | 100 | 100 | 100 | 100 | 100 | 100 | 100 |

The Health Check:

The health of Snow Rivers Limited is currently in a "sweet spot" because it has already crossed the most dangerous hurdle in the hydropower business: the construction phase. Most companies ask for money while they are still digging tunnels and fighting river floods; this company is already finished and has been selling electricity for over a year. This means the risk of project delays or unexpected building costs, the two biggest killers of hydropower value is effectively zero. The fact that the water they use is immediately recycled by another power plant downstream shows a high level of technical planning and cooperation, which stabilizes their operational footprint.

What stands out most is the recent upgrade in their credit rating. Moving from a "BB-" to a "BB+" is a professional signal that the company’s internal health is improving as it shifts from a "borrower" to a "money maker." Their management team has remained consistent through the difficult building years, which suggests a steady hand at the wheel. While the project was slightly expensive to build, the fact that they have a 30-year-plus license means they have a long, clear runway to pay off their bank loans and transition into a "cash cow" that can eventually provide steady rewards to its shareholders. In short, it is a mature, functioning asset rather than a speculative gamble.