Paradox of Growth: Expanding Cooperatives Await Effective Government Intervention

As we saw victims of failed cooperatives protesting at Maitighar Mandala. Many cooperatives have been operating inefficiently, with instances of mismanagement and non-compliance with regulatory guidelines. In some cases, misconduct committed by cooperative operators has severely affected members. As a result, depositors and members are demanding the return of their hard earned savings.

At first glance, one might assume that such incidents would discourage people from joining cooperatives or depositing their money in them. It would seem logical to predict a declining trend in the cooperative sector. However, the reality presents a striking contradiction.

While all classes of financial institutions licensed by Nepal Rastra Bank (NRB), despite having abundant resources, are struggling to expand their businesses, community-based cooperatives - with limited resources and increasing scrutiny from policymakers and expert committees - have continued to achieve remarkable growth. Interestingly, cooperatives are not losing business; instead, they are either maintaining stability or expanding further.

Below is a five year overview (B.S. 2078 to 2082) of the cooperative sector:

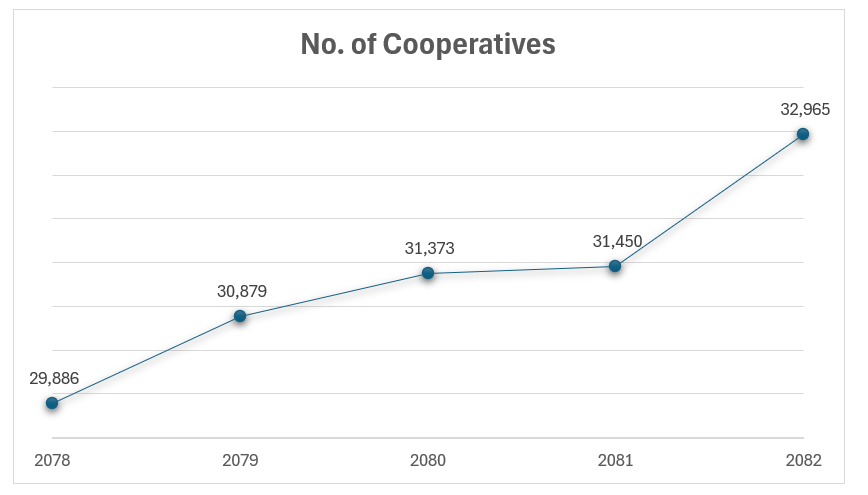

1. Number of Cooperatives

The number of cooperatives has been steadily increasing. Despite widespread negative sentiment and rumors in the market, the overall number of cooperative institutions has not declined. In 2082 alone, 1,515 new cooperatives were established, reflecting an average annual growth rate of 2.50% over the review period.

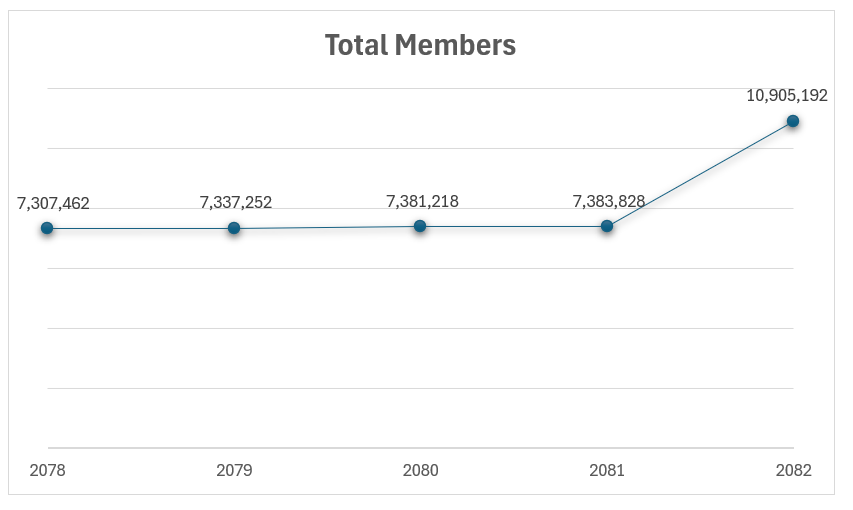

2. Total Members

Cooperatives are not losing their customer base. Even as victims protest to recover their savings, membership continues to grow. On average, cooperatives have recorded an annual membership growth rate of 12.18%.

In 2082, cooperatives added 3,521,364 new members nationwide, marking a significant 47.69% increase in member enrollment.

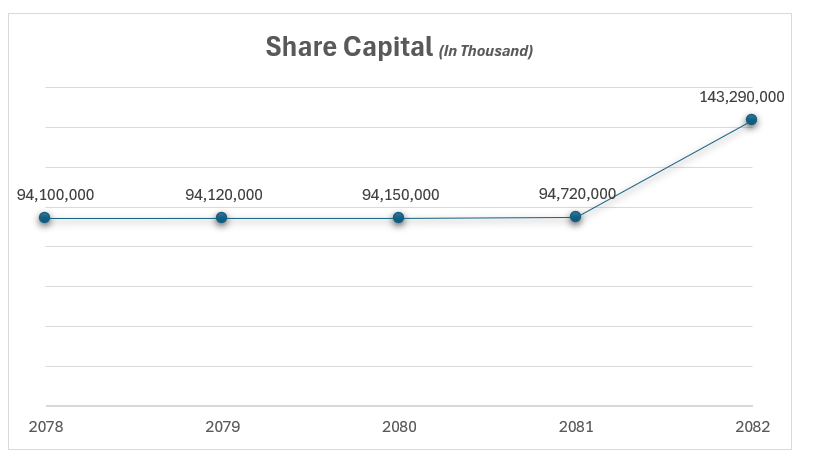

3. Share Capital

As of 2082, a total of 32,965 cooperatives hold a combined share capital of Rs. 143.29 billion. The average share capital per cooperative stands at Rs. 4,346,731. On a per-member basis, the average shareholding amounts to Rs. 13,140.

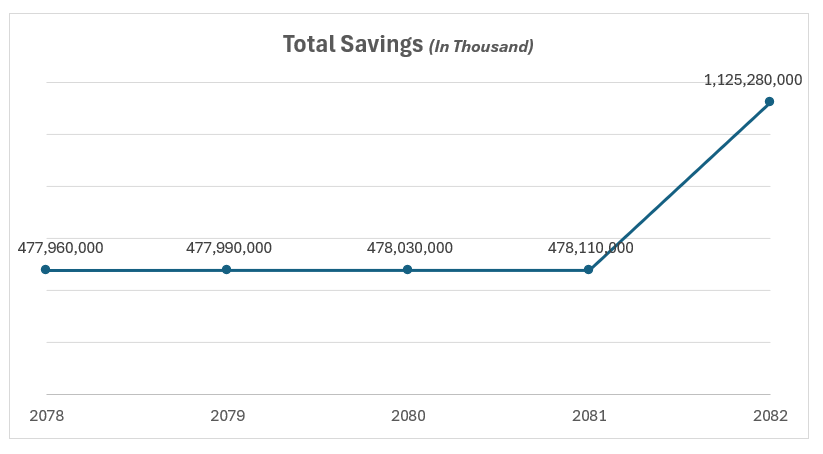

4. Total Savings

Although the sector experienced fluctuations in savings during the review period, 2082 saw a dramatic surge. Total savings grew by 135.36%, increasing from Rs. 478.11 billion in 2081 to Rs. 1,125.28 billion in 2082. On average, each member holds savings of Rs. 103,187 within cooperatives.

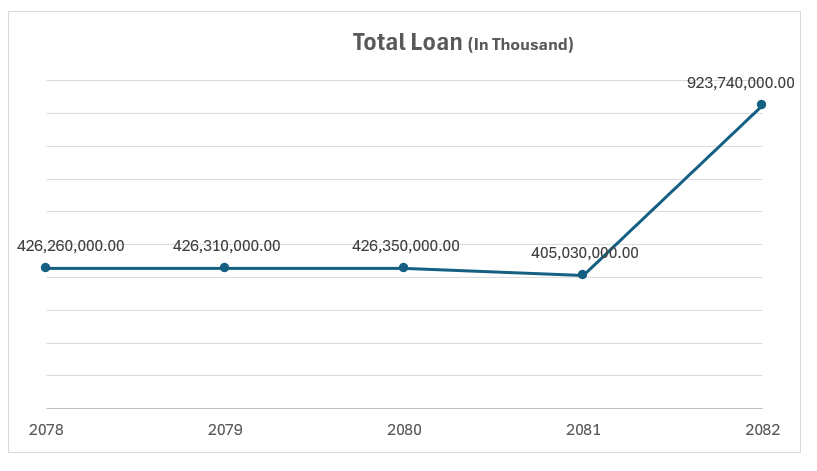

5. Total Loans

In line with the growth in savings, lending also expanded significantly. Total loans increased by 128.07%, rising from Rs. 403 billion to Rs. 923.74 billion.

As of 2082, the credit-to-deposit ratio of cooperatives stands at 82.09%, indicating active financial intermediation.

Key Analytical Insights

- Despite external shocks and governance concerns, the cooperative sector remains strong and continues to grow steadily.

- In 2082 alone, 1,515 new cooperatives were established, and 3,521,364 new members were added. This figure is comparable to the 3,660,438 deposit accounts opened by all NRB-licensed banks and financial institutions (BFIs) during the same period. This raises an important question: why are people still choosing community-based cooperatives over well-regulated and resource-rich BFIs?

- New cooperatives and old cooperatives have increased of Rs. 48.57 billion in share capital within a single year.

- On average, each member holds Rs. 13,140 in shares and Rs. 103,187 in savings within the cooperative sector.

- During the review period, the cooperative sector generated substantial new business, including 3,521,364 new members, Rs. 647.17 billion in additional savings, and Rs. 518.71 billion in new lending.

Conclusion

The cooperative sector in Nepal presents a paradox. On one hand, victims continue to protest against mismanagement and fraud. On the other, the sector continues to expand at an impressive pace, attracting millions of new members and mobilizing vast financial resources.

This contradiction highlights a deeper structural and behavioral question: whether the growth reflects genuine trust in community-based finance - or a gap in financial awareness and regulatory enforcement.