Nepal Bank FPO at 280 can be the best opportunity for value investors to add some share in their portfolio (Exclusive company analysis)

Fri, Jun 29, 2018 12:39 AM on Exclusive, IPO/FPO News, Stock Market, Company Analysis, Latest,

- Puskar Shrestha

After much wait, Nepal Bank Limited (NBL) is issuing its Further Public Offering to the general public. The bank is issuing a total of 1,76,84,858 unit shares as FPO at a price of Rs 280 per share. The bank created many controversies when it had announced to issue FPO as the bank was unable to comply with the guidelines of Securities Registration and Issue Regulation, 2073. People were unsure whether the bank would be able to issue FPO or not. However, the commercial bank will be issuing FPO after gaining approval from all the regulatory bodies.

Synopsis of the issue

Name of the organization: Nepal Bank Limited

No of Share issued: 1,76,84,858 unit

Amount to be collected: Rs 4,95,17,60,240

Issue manager: Siddhartha Capital Limited

The interested applicants can place their applications through any of the financial institutions providing C-ASBA facility. The minimum applications can be placed for 50 units while the maximum applications can be placed for all 1,76,84,858 units.

After the new decision being made by the Securities Board of Nepal (SEBON), the institutional applicants can apply for the share from the first day as well. The issue will open from Ashadh 15, 2075 which will last till Ashadh 19, 2075.

Introduction of the company:

Nepal Bank Limited is the first commercial bank of Nepal which was established in Kartik 30, 1994 B.S. It was formed under the principle of joint venture between Government and the general public.

The authorized capital of the bank is Rs 10 arba. The bank has current paid-up capital of Rs 8.04 arba which will increase by Rs 1.76 arba and its reserve will increase by Rs 3.18 arba after FPO issue.

Composition of Board of Directors

The board of directors is composed of 7 members who are nominated from the following;

|

Person nominated by Nepal Government |

4 |

|

Person nominated from among ordinary shareholders |

2 |

|

Person expert in the field nominated by Nepal Rastra Bank |

1 |

Basic Overview and Competitiveness with the Industry:

Commercial Banks are the largest sectors providing financial services to all the sectors. The investment made in the commercial banks are considered to be a safe investment due to strong fundamentals, stringent regulatory norms as well as due to progressive performance shown by the banks in the recent years. Moreover, 28 commercial banks hold a large portion in the stock market as well.

Being the first commercial bank of the country, Nepal Bank Limited has maintained its long list of customers. Nevertheless, the partial ownership of the Government has also played an important role in the performance of the bank. In terms of accessibility, the bank currently provides banking services through 126 branches.

However, if we consider comparing the performance of Nepal Bank with the industry average, the average growth in the net profit of the industry as per the third quarter report was 18.55% while the profit of Nepal Bank increased by 2.06%. However, Nepal bank was 3rd in terms of net profit as per the third quarter report of the current fiscal year. It had earned Rs 2.56 arba as net profit in the third quarter.

People still have trust on Nepal Bank due to ownership of government and protection of the government.

Strength- Weakness- Opportunities- Threat (SWOT) analysis

Strengths:

- The bank has a long track record being the oldest commercial bank which is further enhanced by the ownership by Nepal Government and an experienced management team.

- The bank already has adequate capitalization which would be further strengthened after the proposed FPO.

- Consistent growth in loans and advances and considerable growth in the total income and net profit.

- Strong current and savings account ratio and comfortable liquidity profile.

- The bank has strong operational profit and growth is outstanding during last few years.

- Improved staff efficiency leads to low expenses compared to its income.

- Nepal Bank has huge land and buildings and investment on different listed companies’ shares.

Weakness:

- The bank has always showcased moderate Assets quality and high non-performing loan ratio.

- Decreasing investment portfolio with less diversification.

- Exposure to regulatory risk related to industry.

Opportunities:

- Nepal Bank always has the opportunity to reach its services to greater number of customers through a wide number of 126 branches.

- Being backed up by the Government provides greater edge over the competitors as there might be increased chances for extending its services and also they have huge amount of lower cost funds of government institutions.

Threats:

- Tough competition from private commercial banks, which in recent times are aggressively increasing branches and customers.

- Lethargic approach of the management has caused the bank to underperform in comparison to its capacity.

Capital Plan of the bank

After the adjustment of the FPO issue, the promoter shareholders (government) will be holding 51% of the total holdings while the general shareholders will be holding 49% of the total shares of the bank. The promoters share would be of Rs 5 arba and the ordinary shareholders would be holding shares worth Rs 4.80 arba in total.

The capital plan of the company can be seen as below:

The current issue is supposed to be the ultimate issue for the bank unless any kind of new capital increment requirement is not presented by the Rastra Bank. The bank’s capital will remain the same and the reserve of the bank is supposed to rise along with the passage of time.

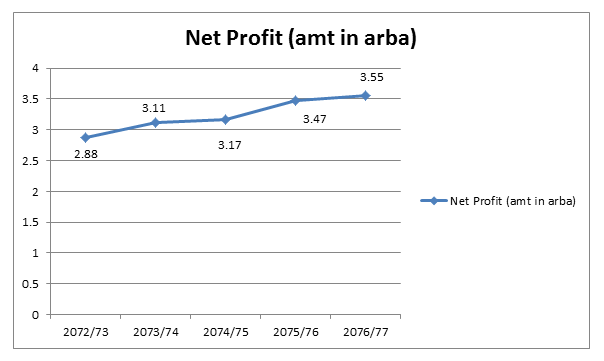

Net Profit:

The bank has published its estimated net profit for the upcoming 3 fiscal years. When we compare the net profit figures as presented by the bank, we can observe the following:

The bank has reported impressive profit in the previous fiscal years and has also projected to continue the rise in the profit following the same trend.

Deposits and Lending

Deposits and lending have simultaneous effect with each other for a banking institution. The creation of one leads to the formation of another. Hence, they are the most integral part of any banking institutions. Due to its long period of service in the banking sector, Nepal Bank Limited stands among one of the top banks with one of the highest amounts of deposit and lending bases.

The bank has projected that its deposit will increase by around 30% at the end of 2076/77 whereas its lending will increase by 71.78% when compared with the actual figures of fiscal year 2072/73.

Underwriters Detail:

|

S.No. |

Name of Underwriter |

Underwritten number of shares |

Underwritten amount (Rs in crore) |

|---|---|---|---|

|

Global IME Capital Limited |

40,50,277 |

113.40 |

|

|

NIBL Ace Capital Limited |

32,13,220 |

89.97 |

|

|

Civil Capital Market Limited |

16,07,252 |

45.00 |

|

|

CBIL Capital Limited |

41,20,932 |

115.38 |

|

|

Sunrise Capital Limited |

12,85,802 |

36.00 |

|

|

Laxmi Capital Market Limited |

16,07,252 |

45.00 |

|

|

Sanima Capital Limited |

9,64,351 |

27.00 |

|

|

Nepal SBI Merchant Banking Limited |

8,35,772 |

23.40 |

|

|

Total |

1,76,84,858 |

494.17 |

Compound Annual Growth Rate (CAGR)

Compound Annual Growth Rate (CAGR) is the mean annual growth rate of an investment over a specified period of time longer than one year.

|

Particulars (Rs in '000) |

FY 2071/72 |

FY 2076/77 |

CAGR (%) |

|---|---|---|---|

|

Size of Balance Sheet (Assets) |

88,211,086.00 |

153,656,808.00 |

11.74% |

|

Deposits |

77,998,776.00 |

116,213,454.00 |

8.30% |

|

Loans and Advances |

50,970,858.00 |

105,226,996.00 |

15.60% |

|

Net Interest Income |

3,311,020.00 |

8,398,593.00 |

20.46% |

|

Net Profit |

483,848.00 |

3,553,440.00 |

49.00% |

|

Average CAGR |

21.02% |

||

CAGR is not a true return rate but it is just a representational figure. CAGR describes the rate at which an investment would have grown at a steady rate.

Price/Earnings to Growth Ratio (PEG Ratio)

The price/earnings to growth ratio (PEG ratio) is a stock’s price-to-earnings (P/E) ratio divided by the growth rate of its earnings for a specified time period. It is used to determine a stock’s value while taking the company’s earnings growth into account, and is considered to provide a more complete picture than the P/E ratio.

PEG Ratio=PE Ratio/ Growth rate

PE Ratio is 6.57 times.

PEG Ratio = 6.57/21.02=0.31

For the calculation of PE ratio the market price of the share has been taken as the issue price of FPO i.e. Rs 280.

The stocks with PEG ratios lower than 1 are considered to be underpriced.

If we compare the PE of Nepal Bank with other commercial banks (Industry Average at 16 times) then its relatively low indicating the price of Nepal Bank is relatively low and also the PEG ratio is far below 1 indicating the FPO price is undervalued.

Graham’s Number

The product of price to earnings ratio and price to book value ratio is called Graham’s number which is named after the “father of value investing”, Benjamin Graham. According to him, if the product of two is below 22.5, the stock is said to be undervalued. Benjamin Graham was the mentor of Warren Buffet, who doesn’t need any introduction. Many successful investors use Graham’s number for the selecting a Stock.

Nepal Bank’s PE is 6.57 and PB is 1.4 at FPO Price.

Graham’s Number of Nepal Bank at FPO Price is PE*PB=6.57*1.4= 9.19 which below 22.5. This also suggests that the price of NBL is undervalued.

In a nutshell:

The FPO issue of Nepal Bank Limited has been a much discussed issue in the stock market. The price at which the FPO is being issued has been termed by many investors to be high compared to its market price. The bank is issuing huge number of shares as well. If the present scenarios are considered, it is most likely that the FPO of Nepal Bank Limited will be undersubscribed. Recently issued FPO of NMB Bank is also facing problems to subscribe the shares even though institutional investors have already been invited to apply for the shares.

Though the bank carries a great legacy behind it and showcases a strong fundamental, the FPO issue of Nepal Bank Limited is not likely to gather attention from the individual investors since its market price is around the FPO price at NEPSE. And probably the FPO issue will be subscribed through the underwriters.

Regarding the number of units to be applied, it can be assumed that the investors will get hold of all the shares that the apply for. So, they investors can place applications for the unit of shares that they wish to hold.

So, considering the market price investors might not be interested to apply but if you are a value investor then FPO of Nepal Bank at Rs 280 can be the best price to hold some shares for long term considering its strong fundamentals.