How did the regional development banks perform this quarter?

Fri, Nov 23, 2018 1:28 PM on Stock Market, Exclusive,

The development banking industry is often found to be changing in today’s scenario. The influence of raised paid up capital requirement is still visible in this sector as the number of listed companies keeps on changing. The merger and acquisition process in still on the runway in this sector. Business students and investors are often confused in understanding the categorization of this industry. Here, is the overall status of companies operating as of today:

Please note that three development banks are going into merger and acquisition namely Sahara Bikas Bank Limited (SHBL), Western Development Bank Limited (WDBL), Hamro Bikas Bank Limited (HAMRO). Sahara Bikas Bank (SHBL) is in acquisition process by Deva Bikas Bank Limited (DBBL), Western Development Bank Limited (WDBL) is in the process of acquisition by Deva Bikas Bank Limited (DBBL) and Hamro Bikas Bank Limited is in the process of acquisition by Jyoti Bikas Bank Limited (JBBL). Post-merger, there will be 16 development banks. The analysis excludes banks which are yet to float IPO, problem ridden banks and Sahara Bikas Bank Limited (SHBL). Hence, the comparative analysis highlights the situation of 18 development banks operating in 1 to 3 districts only.

The further analysis is focused on the 18 development banks operating in 1 to 3 districts and discards all the remaining banks.

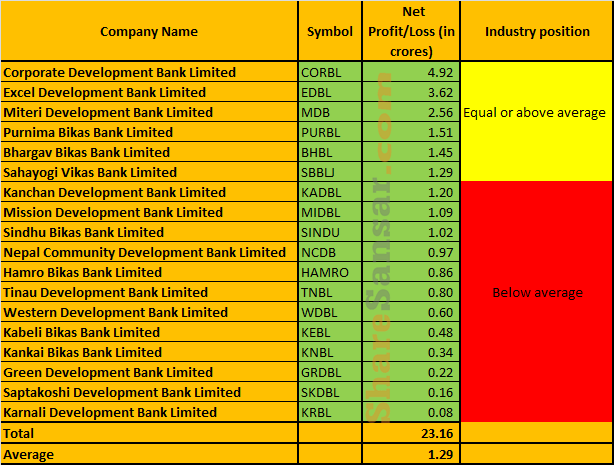

Net profit:

As per the net profit of first quarter of 2075/76, Corporate Development Bank Limited (CORBL) is in the lead with a profit of Rs 4.92 crore. CORBL has a negative reserve and was in loss until 4th quarter of FY 2074/75. Similarly, Excel Development Bank (EDBL) has the second highest net profit of Rs 3.62 crore in the same quarter. The bank with the least net profit is Karnali Development Bank (KRBL) whose net profit amounts to Rs 8 lakhs.

(Please download and study the image in case of difficulty upon studying).

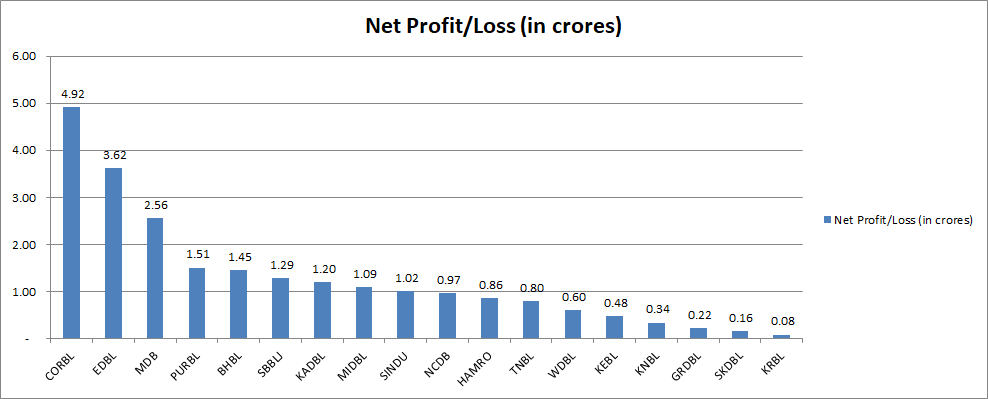

Paid up capital:

The central bank of the country has directed these development “B” categorized banks to meet the paid up capital requirement. NRB has directed development banks of national level to meet the paid up capital of at least 2.50 arba, development banks operating in 4 to 10 districts to meet the paid up capital of at least 1.2 arba and development banks operating in 1 to 3 districts a paid up capital of 50 crores. Only three banks operating in 1 to 3 districts are yet to meet the paid up capital. Excel Development Bank Limited (EDBL) has the highest paid up capital of Rs 69.27 crores followed by Nepal Community Development Bank (NCDB) with Rs 52.64 crores.

(Please download and study the image in case of difficulty upon studying).

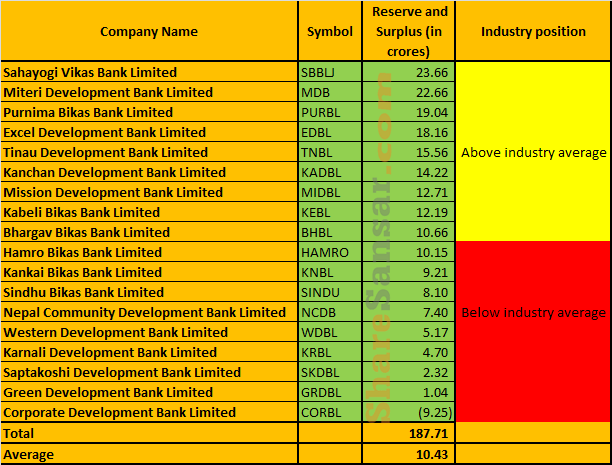

Reserve and surplus:

With the changes in paid up capital, the reserves and surplus of the banks are likely to be affected. In terms of reserves and surplus, Sahayogi Vikas Bank Limited (SBBLJ) has maintained its lead even in reserve and surplus of Rs 23.66 crore. Miteri Deverlopment Bank Limited (MDB) has maintained second position with Rs 22.66 crore reserve and surplus fund. Investors are requested to note down the bank with negative reserve and surplus is Corporate Development Bank Limited (CORBL) having a negative reserve of Rs 9.25 crores.

(Please download and study the image in case of difficulty upon studying).

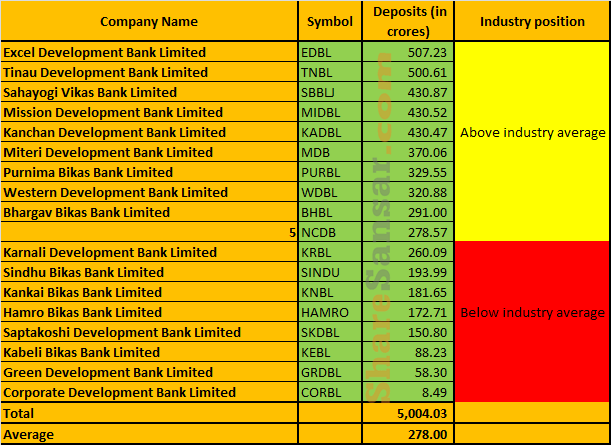

Deposit collection:

The development banks are going through an intense competition with each other. The banks have been trying their best to attract the deposit clients. As of the first quarter of FY 2075/76, Excel Development Bank (EDBL) has established itself in the top list in deposit collection as well. It has a deposit worth Rs 5.07 arba. Similarly, the bank is followed by Tinau Bikas Bank Limited (TNBL) and Sahayogi Vikas Bank Limited (SBBLJ) with the collected deposit of Rs 5.00 arba and Rs 4.30 arba respectively. CORBL has the lowest deposit collection of Rs. 8.49 crore only. The banks operating in 1 to 3 districts collected total deposit worth Rs 50.04 arba.

(Please download and study the image in case of difficulty upon studying).

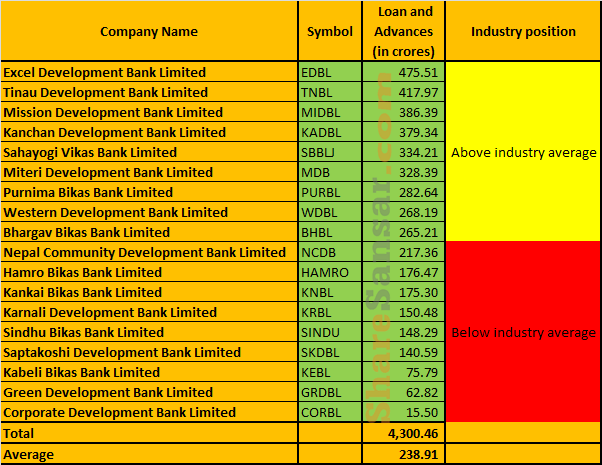

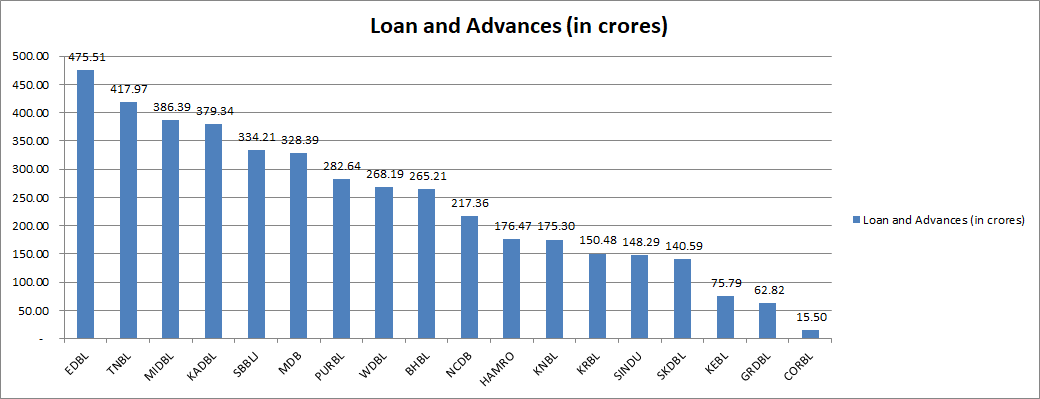

Loans and advances:

As shown by the figures, the positions in loans and advances are almost similar to deposit. The top three positions are occupied by Excel Development bank (EDBL), Tinau Development Bank (TNBL) and Miteri Development Bank Limited (MIDBL) with credit disbursement worth Rs 4.75 arba, 4.17 arba and 3.86 arba.

(Please download and study the image in case of difficulty upon studying).

Major indicators:

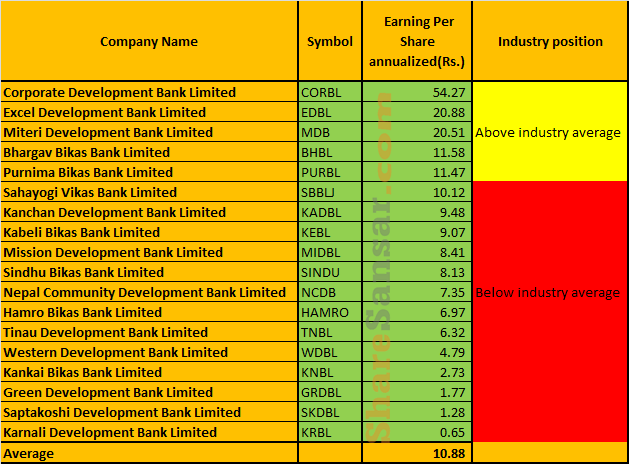

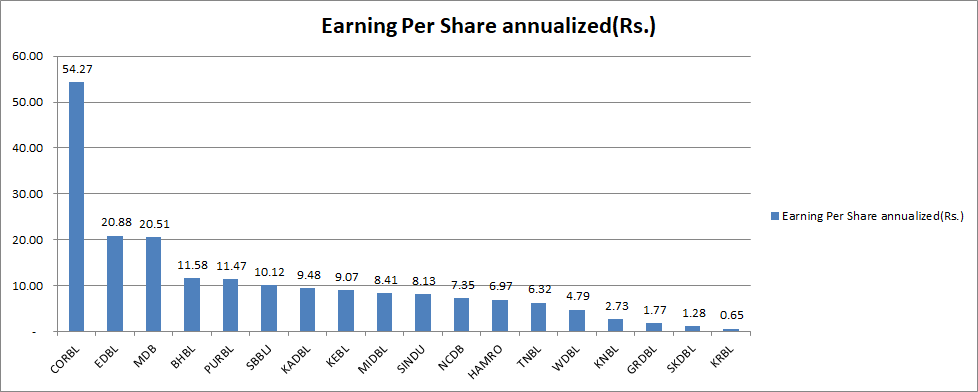

Earnings per share (Annualized):

With the increment in the paid-up capital requirement, the EPS were expected to fall. However, some banks have managed to maintain their EPS better than others. The top position is occupied by Corporate Development Bank Limited (CORBL) with EPS of Rs 54.27. Excel Development Bank (EDBL) is in the second position with an annualized EPS of Rs 20.88 per share. Miteri Development Bank (MDB) has an EPS of Rs 20.51 per share. Note that CORBL reserve is negative and NPL is highest in the industry.

(Please download and study the image in case of difficulty upon studying).

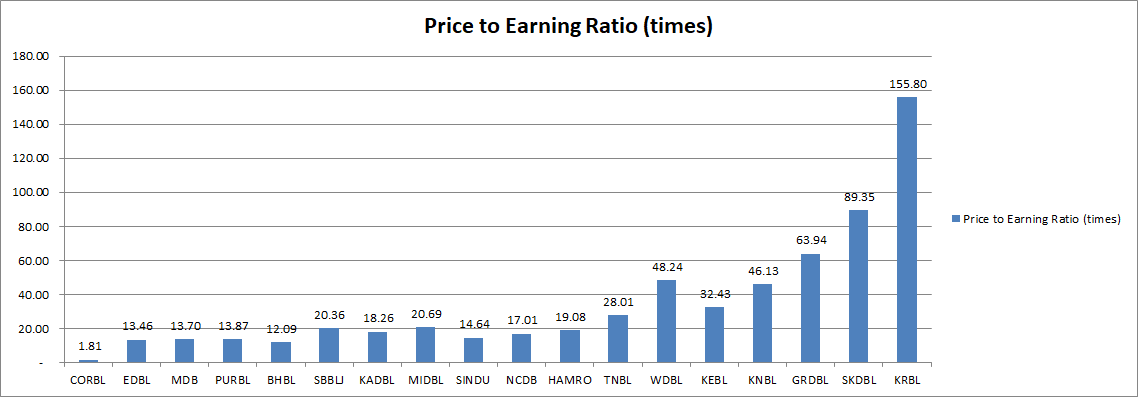

P/E Ratio:

The development bank (operating in 1 to 3 districts) with the lowest P/E ratio as of 21st November, 2018 is Corporate Development Bank Limited (CORBL) i.e. 1.81 times followed by Excel Development Bank Limited (EDBL) with P/E ratio of 13.46 times.

(Please download and study the image in case of difficulty upon studying).

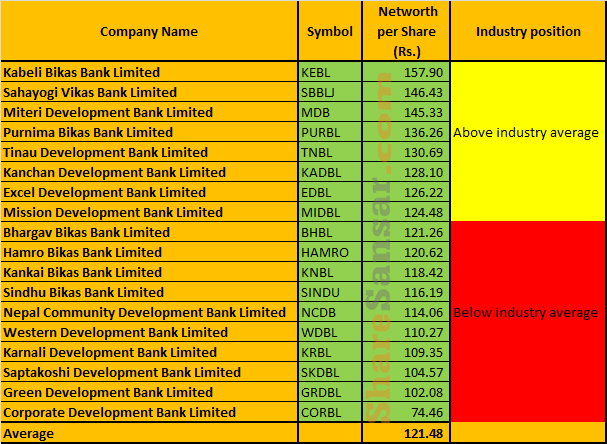

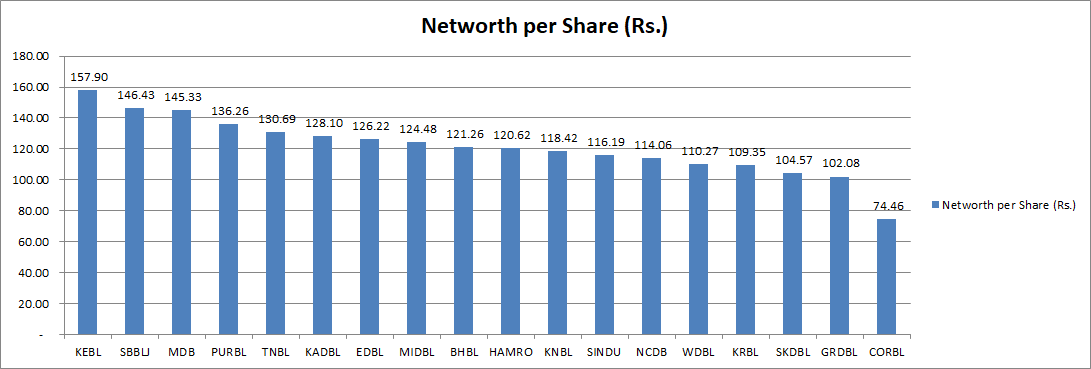

Net worth per share:

The highest net worth per share among these development banks is Rs 157.90 of Kabeli Bikas Bank Limited (KEBL). Sahayogi Bikas Bank Limited (SBBLJ) has the second highest net worth per share as of Q1 of FY 2075/76 i.e. Rs 146.43.

(Please download and study the image in case of difficulty upon studying).

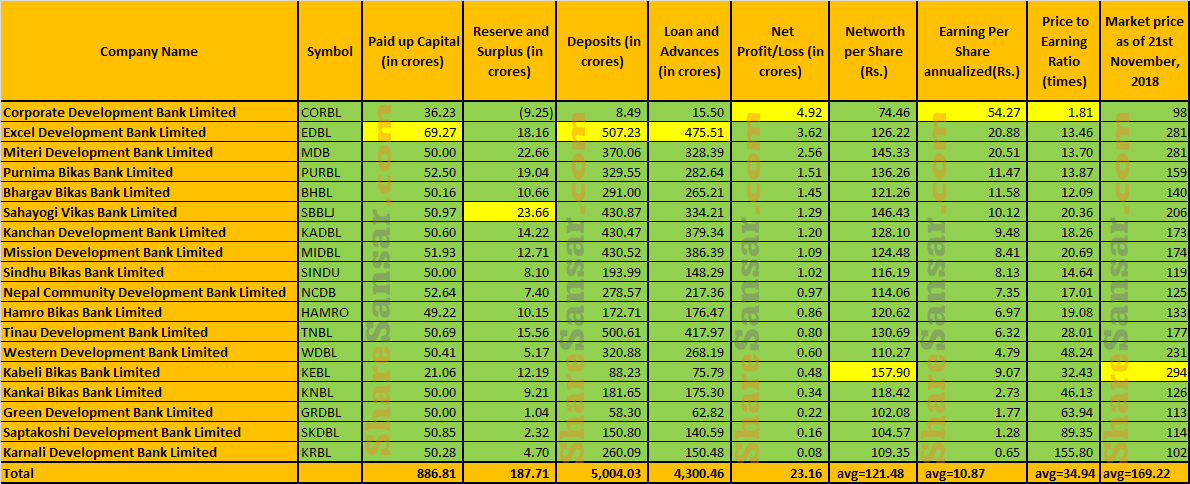

A full picture:

Finally the table below provides a full picture with major indicators of the development banks as of the first quarter of FY 2075/76:

(Please download and study the image in case of difficulty upon studying).

Please feel free to drop a comment if you have any say on the operation of these development banks.