Despite of huge business growth; most of the commercial banks succeed to maintain low Non-performing loan

Mon, Aug 28, 2017 6:50 AM on Latest, Exclusive, Featured, Stock Market,

Non-performing loans (NPL), simply known as bad loans represents the portion of loans whose timely principal or interest are not received by the banks. Moreover, it is the fundamental ratio which shows percentage of loans which are default on scheduled payment of principal or interest.

NPL above 5% is considered to be riskier. So, investors must be cautious with the bank having high NPL before investing. Thus, more the NPL, more will the risk for banks and vice versa. Risk in the sense that higher NPL restricts the banks from providing dividends to its shareholders from the profit it earned and also it increases its risk weighted assets for which bank needs to maintain extra capital. This case may be the vital factor for diminishing the goodwill of the bank as well. Following are the main conditions on which loans loss provisions are made, incase;

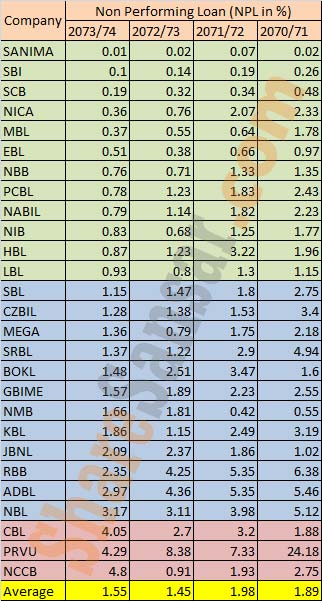

Below table shows the NPL of last 4 fiscal year (FY):

Below table shows the NPL of last 4 fiscal year (FY):

(Note: while calculating average NPL, NPL above 5% is not included as NPL of some banks above 5% may affect the average NPL.)

From the above data in the FY 2073/74, Sanima Bank Limited (SANIMA) stood at the top of table with NPL of 0.01% only, followed by Nepal SBI Bank Limited (SBI) and Standard Chartered Bank Nepal Limited (SCB) with NPL of 0.1% and 0.19% respectively. Civil Bank Limited (CBL), Prabhu Bank Limited (PRVU) and Nepal Credit and Commerce Bank Limited (NCCB) has highest NPL among the commercial bank above 4%. Average NPL stands at 1.55%.

(Note: while calculating average NPL, NPL above 5% is not included as NPL of some banks above 5% may affect the average NPL.)

From the above data in the FY 2073/74, Sanima Bank Limited (SANIMA) stood at the top of table with NPL of 0.01% only, followed by Nepal SBI Bank Limited (SBI) and Standard Chartered Bank Nepal Limited (SCB) with NPL of 0.1% and 0.19% respectively. Civil Bank Limited (CBL), Prabhu Bank Limited (PRVU) and Nepal Credit and Commerce Bank Limited (NCCB) has highest NPL among the commercial bank above 4%. Average NPL stands at 1.55%.

- If lender becomes bankrupt

- It lender disappears or becomes out of contact

- If loans are misused

- If lenders are blacklisted by Credit Information Bureau (CIB)

- If lenders make delayed in payment of principal and interest as per scheduled set by NRB.

Below table shows the NPL of last 4 fiscal year (FY):

(Note: while calculating average NPL, NPL above 5% is not included as NPL of some banks above 5% may affect the average NPL.)

From the above data in the FY 2073/74, Sanima Bank Limited (SANIMA) stood at the top of table with NPL of 0.01% only, followed by Nepal SBI Bank Limited (SBI) and Standard Chartered Bank Nepal Limited (SCB) with NPL of 0.1% and 0.19% respectively. Civil Bank Limited (CBL), Prabhu Bank Limited (PRVU) and Nepal Credit and Commerce Bank Limited (NCCB) has highest NPL among the commercial bank above 4%. Average NPL stands at 1.55%.

- Sijan Bajracharya