Shikhar Power Development Limited Issues IPO for General Public From Today: In Depth Analysis of Company Performance

Sun, Mar 1, 2026 12:13 PM on Company Analysis, IPO/FPO News, Latest,

Company Profile:

Shikhar Power Development Limited is a Nepalese hydropower company established in Bhadra 2071 B.S. (2015 A.D.), focused on developing and operating run‑of‑river hydropower projects. The company aims to contribute to Nepal’s energy sector by generating clean and reliable electricity for the national grid, leveraging the country’s abundant water resources.

Its flagship project, the Bhim Khola Small Hydropower Project (4.96 MW), is already operational, while the Lower Bhim Khola Cascade Project (6.05 MW) is under construction, expected to further increase the company’s capacity and revenue. Before its IPO, the company was fully promoter owned, and it has now opened up 32.65 % of its shares to the public, retaining 67.35 % with the original promoters.

Board of Directors:

|

Name |

Position |

|---|---|

|

Mr. Narayan Prasad Upadhyay |

Chairman |

|

Mr. Hemraj Acharya |

Managing Director |

|

Mr. Saroj Prasad Dahal |

Director |

|

Mr. Namrata K.C |

Director |

|

Mr. Abhaya Singh Panday |

Director (Expert) |

About the Issue & Rating:

|

Aspect |

Details |

|---|---|

|

Total IPO Shares Issued |

3,200,000 ordinary shares |

|

Face Value per Share |

Rs 100 |

|

Portion of Shares Offered to Public |

32.65 % of total issued capital |

|

Portion Retained by Promoters |

67.35 % of total share capital |

|

Issue Manager |

Global IME Capital Limited |

|

Rating Agency |

ICRA Nepal Limited |

|

Issuer Credit Rating Assigned |

[ICRANP‑IR] BB |

|

Rating Interpretation |

Moderate credit risk: indicates moderate ability to timely meet financial obligations |

The company’s issued capital is Rs 98 crore, of which 32.65% (3,200,000 shares) will be offered to the public at Rs 100 per share. 10% (980,000 shares) is reserved for locals affected by the project and its transmission line in Baglung District. The remaining 22.65% (2,220,000 shares) is for the general public, of which 10% (222,000) is for Nepalis working abroad, 2% (44,400) for company employees, and 5% (111,000) for mutual funds. The general public can apply for 1,842,600 shares, opening on 17th Falgun.

Financial Performance:

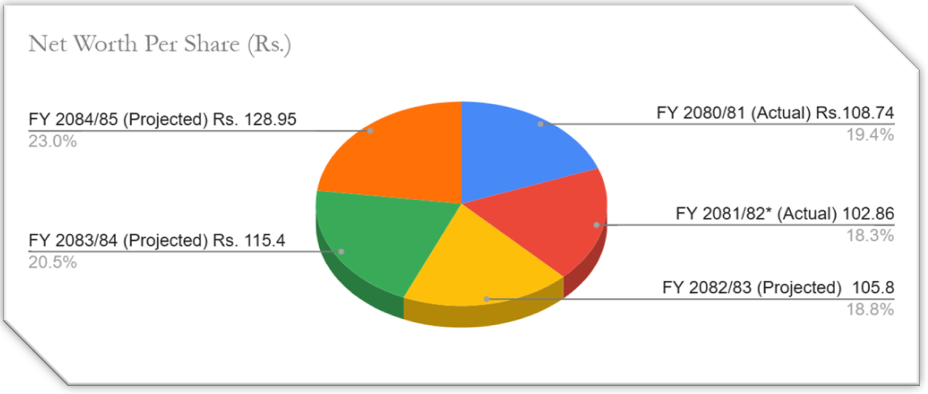

- Net Worth Per Share:

The charts and table show that each share currently has a real world value of Rs. 102.86, which is slightly above the price you would pay to buy it. While there was a minor dip in value recently as the company spent money to complete its first power plant, the outlook is very positive. As the company begins selling electricity consistently, its value is projected to grow by roughly 25% over the next three years, reaching Rs. 128.95 per share by 2085.

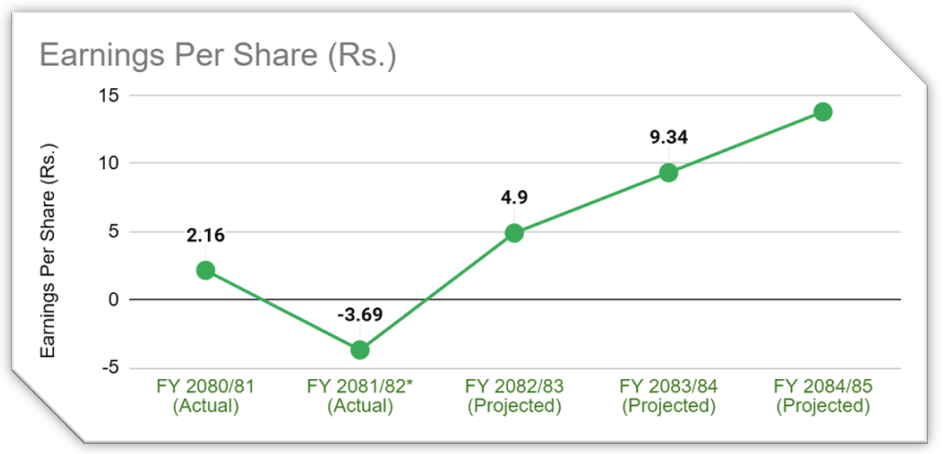

2. Earning Per Share:

The Earnings Per Share (EPS) chart shows that the company is currently moving through a typical "startup" phase for a hydropower project. While they recorded a loss of Rs. 3.69 per share in this F.Y 2081/82, However, the outlook is positive as the company projects a quick recovery, expecting to earn Rs. 4.90 per share next year. As their power plants reach full operation, these earnings are predicted to climb steadily to Rs. 9.34 and Rs. 13.81 by FY 2083/84 and 2084/85 respectively, showing that the company expects its profit making ability to nearly triple in the coming years.

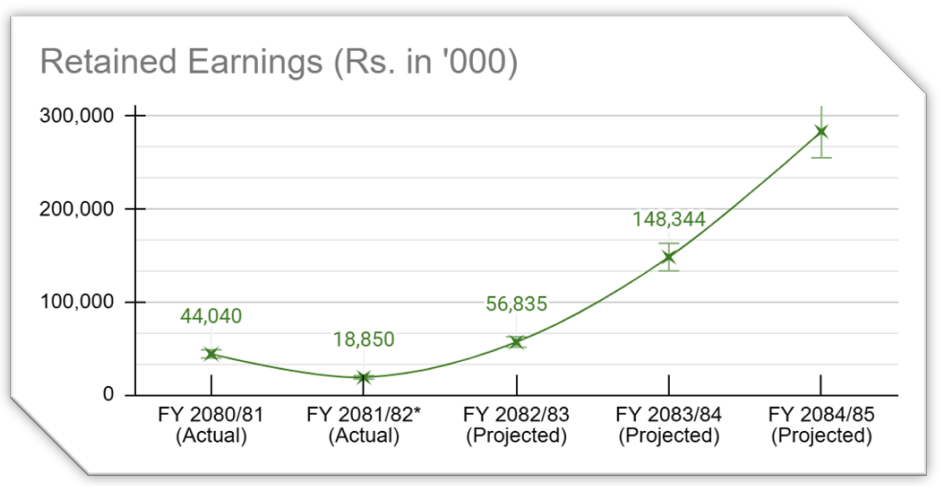

3. Reserve & Surplus:

The company's Retained Earnings which are the accumulated profits kept for future growth rather than paid out show a temporary dip to Rs. 1.88 Crores in the most recent actual year (FY 2081/82). However, the outlook is very strong, with the company projecting a massive recovery as its power plants become fully productive. These savings are expected to grow nearly 15 times higher, reaching over Rs. 28.36 Crores by FY 2084/85 and 14.83 Crores by FY 2083/84, which suggests the company is building a significant financial cushion to pay off its debts and eventually reward its shareholders.

4. Financial Highlight:

|

Particulars |

Actual |

Estimated |

|||

|---|---|---|---|---|---|

|

2080/81 |

2081/82 |

2082/83 |

2083/84 |

2084/2085 |

|

|

Total Non-Current Assets |

12,43,192 |

1,371,817 |

18,24,882 |

24,39,349 |

2,355,713 |

|

Total Current Assets |

59,284 |

68,486 |

253,847 |

174,620 |

264,665 |

|

Total Assets |

13,02,476 |

1,440,303 |

2,078,729 |

2,613,969 |

2,620,378 |

|

Shae Capital ('000) |

50,40,00 |

66,00,00 |

9,80,000 |

9,80,000 |

9,80,000 |

|

Reserve & Surplus ('000) |

44,040 |

18,850 |

56,835 |

148,344 |

283,675 |

|

Total Current Liabilities |

80,301 |

84,515 |

2,492 |

49,093 |

3,062 |

|

Total Equity & Liabilities |

13,02,476 |

1,440,303 |

2,078,729 |

2,613,969 |

2,620,378 |

|

Net Profit ('000) |

10,879.00 |

-24,328.00 |

47,985.00 |

91,509.00 |

135,331.00 |

|

Earnings Per Share (Rs.) |

2.16 |

-3.69 |

4.9 |

9.34 |

13.81 |

|

Net Worth Per Share (Rs.) |

108.74 |

102.86 |

105.8 |

115.4 |

128.95 |

|

Return on Equity (%) |

1.99 |

-3.59 |

4.63 |

8.09 |

10.71 |

Risk Vs Return:

Analysing the risk versus return for Shikhar Power Development Limited reveals a company in a significant transition phase, moving from heavy investment into a period of expected high production. The primary risk lies in the short term financial stability, as seen in the recent actual loss of Rs. 3.69 per share for FY 2081/82 and a sharp drop in cash reserves from Rs. 4.4 Crore to Rs. 1.8 Crore. This "startup" phase is typical for hydropower, where high interest on loans and construction costs temporarily outweigh income. However, the potential return is high; the company projects a rapid recovery with net profits reaching Rs. 13.53 Crore and an Earnings Per Share (EPS) of Rs. 13.81 by FY 2084/85. Furthermore, the efficiency of the company is expected to improve greatly, with the Return on Equity (ROE) projected to climb from a low of 1.99% to a robust 10.71%. Overall, while there is immediate risk due to low cash cushions and current losses, the long term prospect offers a strong growth opportunity if the company meets its electricity production targets over the next three years.