NEPSE Valuations Surge: P/E and P/B Ratios Near Record Highs as Banking Sector Remains Undervalued

Sun, Nov 2, 2025 4:45 PM on Stock Market, Exclusive,

The Nepal Stock Exchange (NEPSE) was established on January 13, 1994, marking the beginning of a formal and regulated secondary securities market in Nepal. Trading on the NEPSE floor began the same day with 62 listed companies, primarily comprising commercial banks, development banks, insurance firms, and a few manufacturing and hotel companies. Today, NEPSE has grown to 251 listed companies across 12 sectors -Commercial Banks, Development Banks, Finance, Microfinance, Life Insurance, Non-Life Insurance, Hydropower, Manufacturing & Processing, Hotels & Tourism, Investment, Trading, and Others. With new listings each year, these sectors continue to expand, reflecting the gradual deepening of Nepal’s capital market.

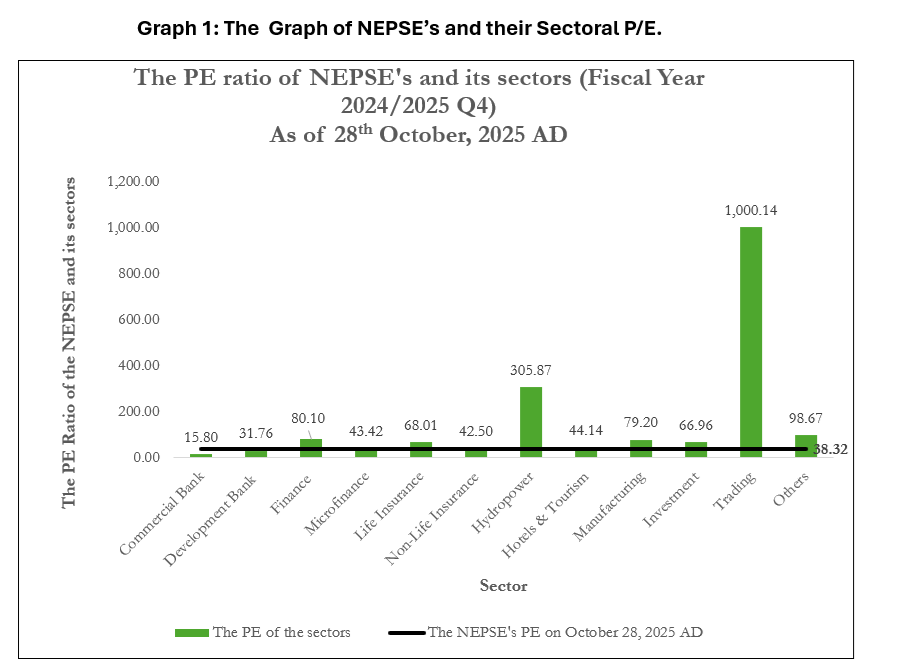

The Price-to-Earnings (P/E) and Price-to-Book (P/B) ratios are key indicators used to assess whether stocks are undervalued or overvalued. The P/E ratio reflects how much investors are willing to pay for each rupee of a company’s earnings, while the P/B ratio measures how much they are willing to pay relative to the company’s net worth. Based on financial statements for Q4 of FY 2024/25, the latest P/E and P/B ratios as of 28th October 2025 reveal the valuation levels of NEPSE and its various sectors:

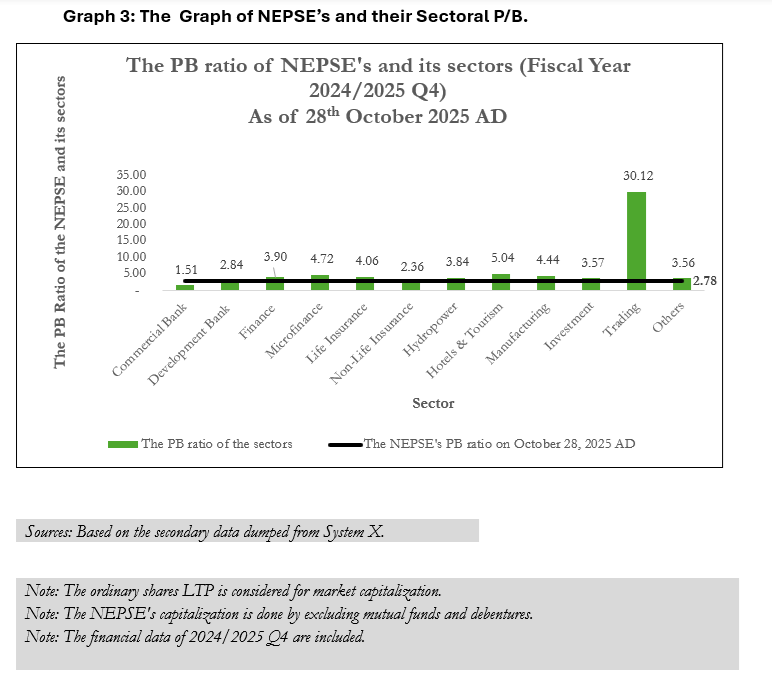

Sources: Based on the secondary data dumped from System X.

Note: The ordinary shares LTP is considered for market capitalization.

Note: The NEPSE's capitalization is done by excluding mutual funds and debentures.

Note: The financial data for 2024/2025 Q4 are included.

Sources: Based on the secondary data dumped from System X.

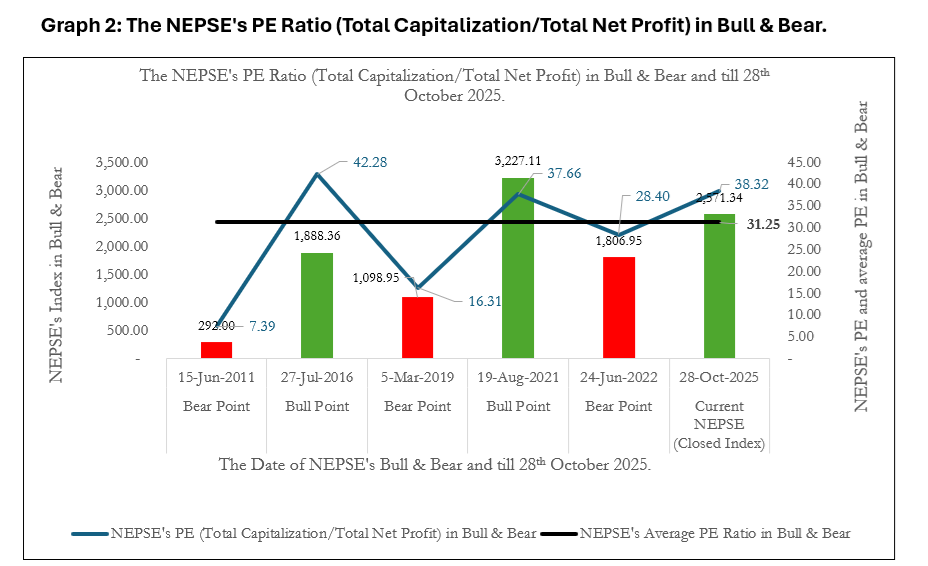

Higher P/E and P/B ratios indicate that investors are paying more for earnings and book value, respectively. According to legendary investor Benjamin Graham, a P/E ratio below 15 provides a “margin of safety” for long-term value investors. Similarly, the CFA Institute notes that P/E ratios below the market average-typically 10-15 are considered attractive when earnings quality is strong. Globally, a sustainable P/E range for long-term investment is 15-20, while ratios above 25 are generally seen as overvalued unless supported by robust earnings growth. As of October 28, 2025, NEPSE’s overall P/E ratio stands at 38.32, significantly higher than the global health range and above its historical average of 31.25, nearing the past peak of 42.28. Among all sectors, commercial banks have the lowest P/E of 15.80, followed by development banks, while all other sectors trade well above NEPSE’s average. Although the P/E ratio alone cannot determine valuation, it should be analyzed alongside factors such as earnings growth, return on equity, cost of capital, inflation and interest rates, earnings retention, and industry comparisons. In Nepal’s current economic and political climate, most of these factors remain unfavorable, with only interest rates and inflation showing mild improvement. Therefore, NEPSE’s high sectoral P/E ratios appear unjustified, leaving commercial banking as the only sector that still looks undervalued.

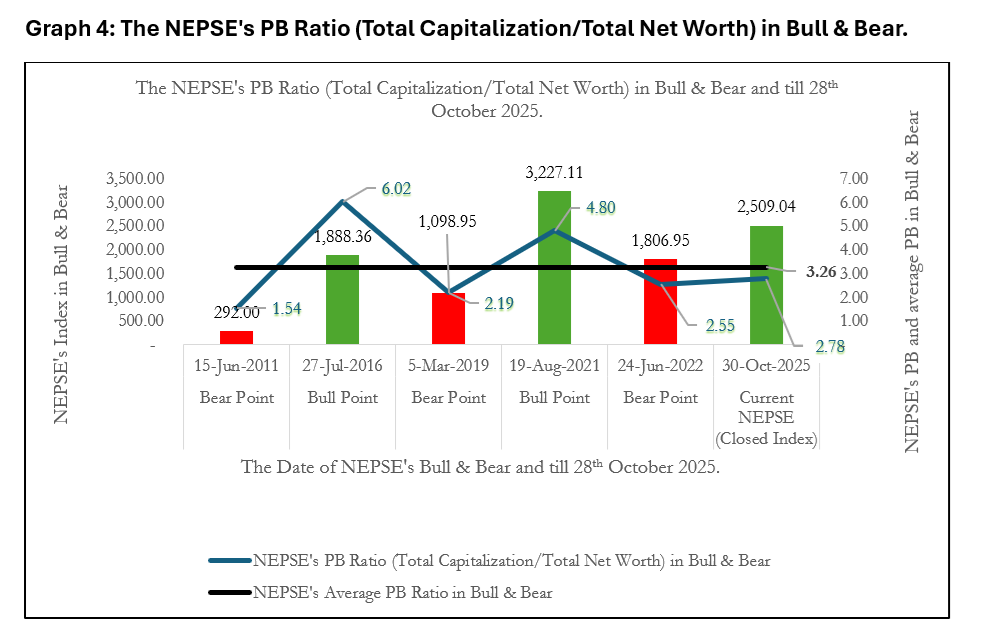

The Price-to-Book (P/B) ratio remains one of the most established valuation metrics, widely used by both value and institutional investors to gauge long-term investment appeal. It reflects how much investors are willing to pay for each unit of a company’s net book value - calculated as Assets minus Liabilities. A P/B ratio of 1 means a stock is trading exactly at its book value; above 1 indicates overvaluation, and below 1 suggests undervaluation. Globally, an optimal long-term P/B range lies between 1.5 and 2.5, though it varies by sector and profitability. High-growth sectors like technology or consumer goods can justify higher ratios of 3-5 if their return on equity (ROE) consistently exceeds the cost of capital. As of October 28, 2025, NEPSE’s overall P/B ratio stands at 2.78, exceeding the healthy global range. Only the commercial banking sector appears reasonably valued with a P/B of 1.51, while most other sectors trade above NEPSE’s average. Although the overall P/B level is close to its historical average, the valuation is not supported by improved fundamentals. The P/B ratio, like the P/E ratio, should be interpreted in context with ROE, cost of equity, and sustainable growth rate. In Nepal’s current political and economic environment, most of these factors remain unfavorable. While lower interest rates have slightly reduced the cost of equity, they alone do not justify the high valuations across sectors. Historically, NEPSE’s growth has not been backed by corresponding earnings or economic expansion. After reaching its all-time high of 3,227.11 on August 19, 2021, driven by pandemic-era liquidity and online trading, the index fell sharply to 1,806.95 by mid-2022. A partial recovery followed, reaching 3,048.15 in August 2024, aided by policy easing and reduced interest rates. However, since then, NEPSE has mostly moved sideways between approximately 2,440 and 3,000, with persistent political instability weighing on sentiment.

Without strong earnings growth or economic improvement, the index is unlikely to surpass its 2021 peak. Many mid- and low-cap stocks are already inflated beyond their fundamentals, creating a potential bubble risk. For long-term value investors, the commercial banking sector and a few stocks of other sectors remain the most viable opportunities, given their moderate valuations and relatively stable fundamentals. To achieve sustainable returns, investors should focus on fundamentally strong, dividend-paying companies with reasonable P/E and P/B ratios, supported by solid business growth and long-term value creation.

Article By: Dipendra Pandey

(Finance Enthusiast, Former Merchant Banker, Manager at Prince Cargo Pvt. Ltd., and Proprietor of Barahi Farmhouse)

References:

1. Narayan Prasad Paudel, INVESTING IN SHARES OF COMMERCIAL BANKS IN NEPAL: AN ASSESSMENT OF RETURN AND RISK ELEMENTS.

2. Stock Market, NEPSE: Past, Present and Future, Sharesansar.

https://www.sharesansar.com/newsdetail/stock-market-nepse-past-present-and-future

3. JOHN SCHELLHASE, STACI WARDEN, MILKEN Institute, Framing the Issues: Modernizing the Public Equity Market in Nepal.

4.Securities Board of Nepal (SEBON) – “English Section” document.

5.Nepal Rastra Bank (NRB) – Occasional Paper “The Development of Securities Market in Nepal”.

https://www.nrb.org.np/contents/uploads/2022/07/vol13_art1.pdf?utm_source=chatgpt.com

6.Dhan R Chalise (2020), Secondary Capital Market of Nepal: Assessing the Relationship Between Share Transaction and NEPSE Index, Management Dynamics, 2020 , Volume 23, No. 2: 53-62, 2020.