Unveiling Q1 FY 2082/83: A Comprehensive Analysis of Leading Commercial Banks and Key Financial Insights

Fri, Nov 14, 2025 1:30 PM on Financial Analysis, Company Analysis, Corporate, Exclusive,

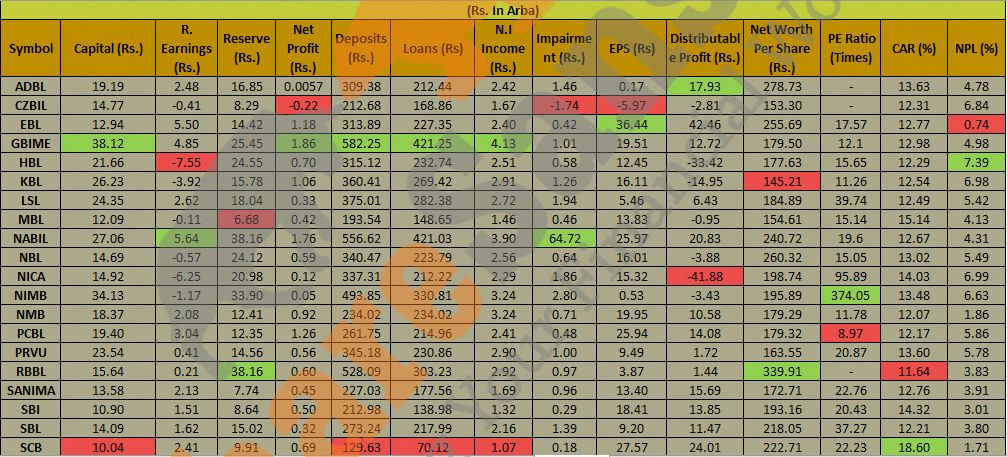

All 20 commercial banks have unveiled their financial reports for the first quarter of FY 2082/83, offering a fresh look into their performance during the third-month period. The disclosures present a deeper understanding of their profitability, capital strength, and overall business growth. This summary captures the major highlights and evolving trends in net earnings, capital adequacy ratios, and other essential financial indicators.

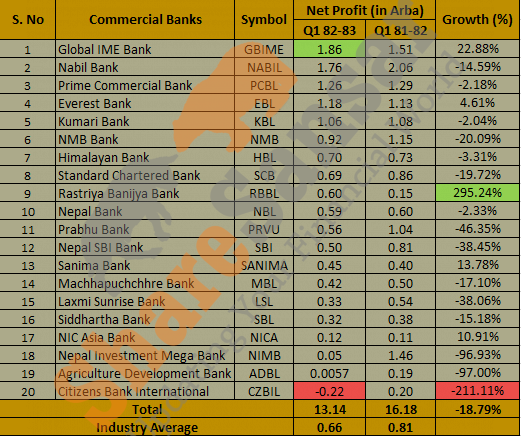

Net Profit:

In Q1 FY 2082/83, Global IME Bank Limited (GBIME) led with a net profit of Rs. 1.86 Arba, marking a 22.88% increase over the same period last year. Nepal Investment Mega Bank (NIMB) followed with a net profit of Rs. 1.76 Arba, though this represents a 14.59 % decrease from the previous year. Prime Commercial Bank Limited (GBIME) took third with Rs. 1.26 Arba.

Ratriya Banjiya Bank Limited (RBL) recorded the highest growth, a staggering 295.24% rise, while Citizens Bank International Limited (CZBIL) saw the largest decline at 211.11%.

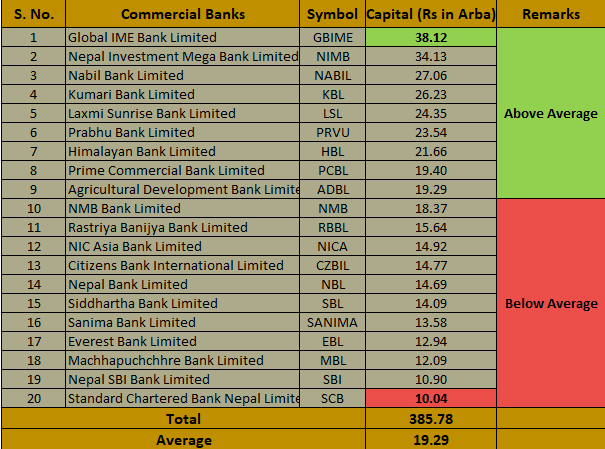

Paid-Up Capital:

Global IME Bank Limited (GBIME) holds the highest paid-up capital at Rs. 38.12 Arba, followed by Nepal Investment Mega Bank Limited (NIMB) at Rs. 34.13 Arba, and Nabil Bank Limited (NABIL) with Rs. 27.06 Arba. Standard Chartered Bank Nepal Limited (SCB) has the lowest paid-up capital at Rs. 10.04 Arba.

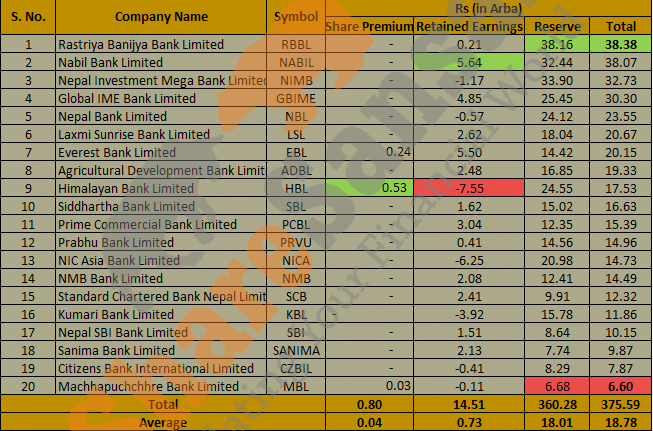

Reserve and Surplus:

The combined reserve and surplus of all commercial banks totaled Rs. 3.75 Kharba, with the industry average standing at Rs. 18.78 Arba. Rastriya Banijya Bank Limited (RBBL) led with Rs. 38.38 Arba, followed by Nabil Bank Limited (NABIL) at Rs. 38.07 Arba and Nepal Investment Mega Bank Limited (NIMB) with Rs. 32.73 Arba.

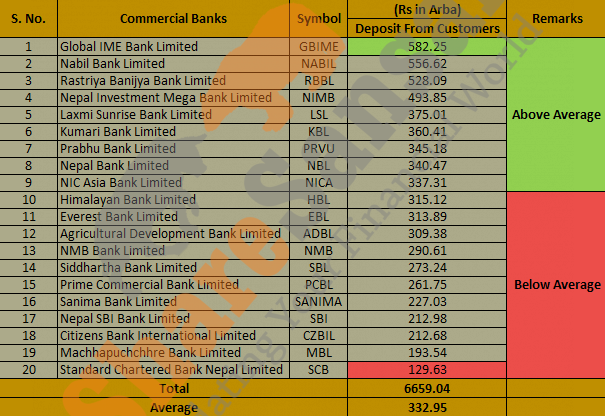

Deposits From Customers:

Collectively, commercial banks gathered Rs. 66.02 Kharba in customer deposits, with nine banks surpassing this average. Global IME Bank Limited (GBIME) led at Rs. 5.82 Kharba, followed by Nabil Bank Limited (NABIL) at Rs. 5.56 Kharba and Rastriya Banijya Bank (RBBL) at Rs. 5.28 Kharba. Standard Chartered Bank Nepal Limited (SCB) recorded the lowest deposit collection at Rs. 1.29 Kharba.

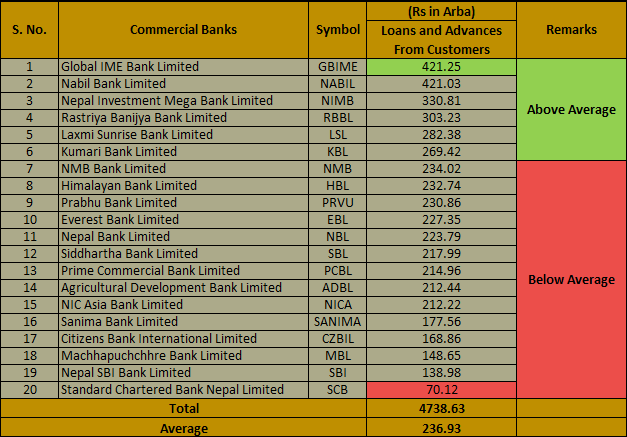

Loans and Advances to Customers:

Global IME Bank Limited (GBIME) topped the list in loans and advances with Rs. 4.21 Kharba, followed by Nabil Bank Limited (NABIL) also with Rs. 4.21 Kharba.

Standard Chartered Bank Nepal Limited (SCB) had the smallest portfolio at Rs. 70.12 Arba. The industry average loan disbursement was Rs. 7.01 Kharba, with six banks exceeding this average.

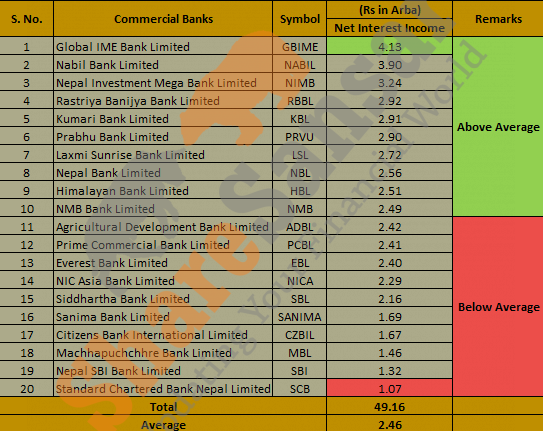

Net Interest Income:

Net interest income, reflecting core banking earnings, saw Global IME Bank Limited (GBIME) leading at Rs. 4.13 Arba, closely followed by Nabil Bank Limited (NABIL) at Rs. 3.90 Arba.

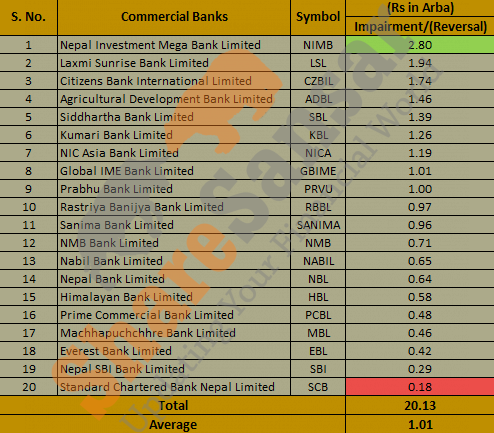

Provisions (Impairment/Reversal):

Banks allocated Rs. 20.13 Arba for loan loss provisions and delayed loan repayments. Global IME Bank Limited (GBIME) recorded the highest impairment charge at Rs. 2.80 Arba, with Citizens Bank International Limited (CZBIL) next at lowest Rs. 0.18 Arba.

Major Indicators:

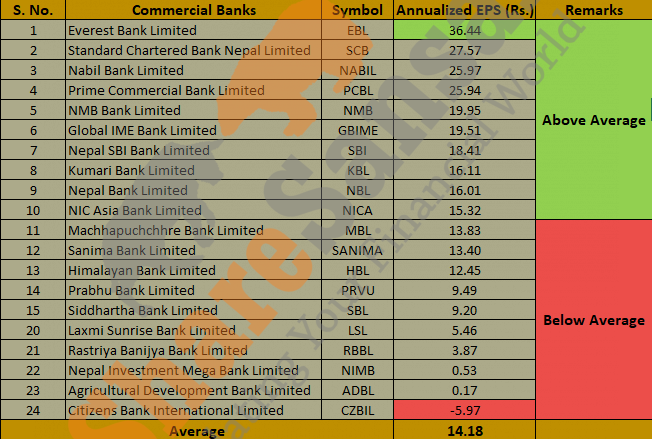

Annualized Earnings Per Share (EPS):

Everest Bank Limited (EBL) posted the highest annualized EPS at Rs. 36.44, followed by Standard Chartered Bank Nepal Limited (SCB) at Rs. 27.57 and Prime Commercial Bank Limited (PCBL) at Rs.26.53. The industry average EPS was Rs.13.80, with ten banks above this benchmark. Citizens Bank International Limited (CZBIL) had the lowest EPS at Rs. 5.97.

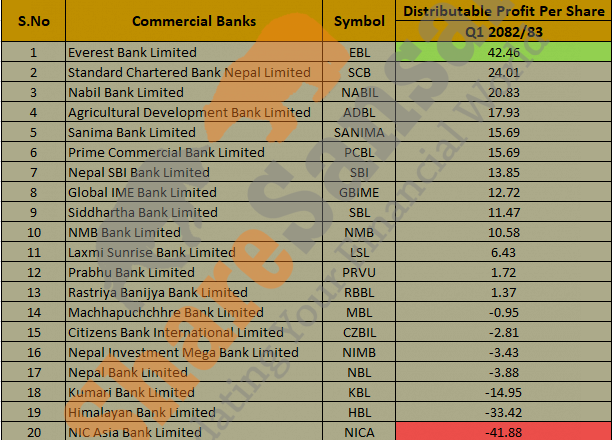

Distributable Profit Per Share:

Everest Bank Limited (EBL) reported a distributable profit exceeding Rs. 42.46 per share, followed by Standard Chartered Bank Nepal Limited (SCB) at Rs. 24.01. Seven banks reported negative distributable profit per share for the quarter.

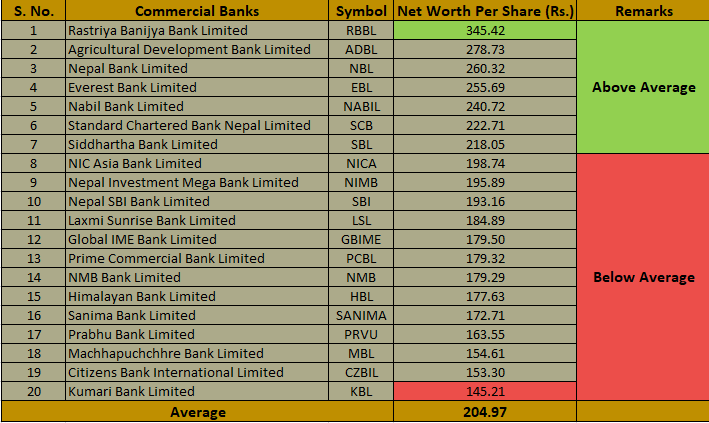

Net Worth Per Share:

Rastriya Banijya Bank Limited (RBBL) reported the highest net worth per share at Rs 339.91, followed by Agriculture Development Bank Limited (ADBL) at Rs 278.73 and Nepal Bank Limited (NBL) at Rs 260.32. Kumari Bank Limited (KBL) recorded the lowest net worth per share at Rs 145.21, while the industry average stood at Rs 203.84.

*Note: Preference Share is excluded while calculating the Net worth of Agriculture Development Bank (ADBL).

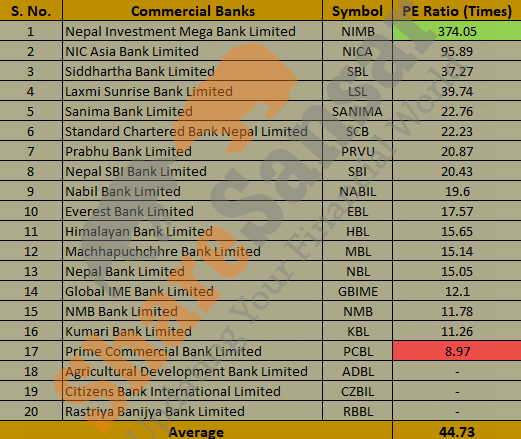

P/E Ratio:

Prime Commercial Limited (PCBL) had the lowest P/E ratio at 8.97 times, followed by Kumari Bank Limited (kBL) at 11.26 times. This reflects quarter-end ratios, and current ratios may vary with recent stock prices.

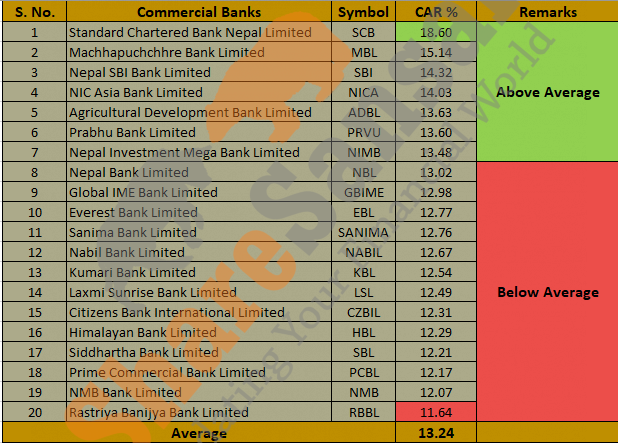

Capital Adequacy Ratio (CAR):

Standard Chartered Bank Nepal Limited (SCB) reported the highest CAR at 18.60%, while NMB Bank Limited (NMB) reported the lowest at 12.07%. This ratio indicates a bank’s capital in relation to its risk-weighted assets.

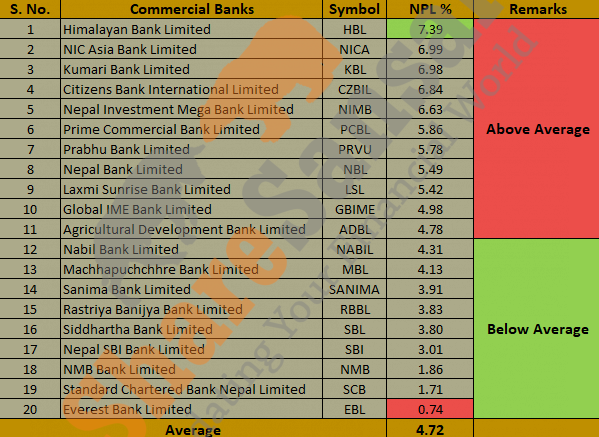

Non-Performing Loan (NPL):

Everest Bank Limited (EBL) had the lowest NPL at 0.74%, while Himalayan Bank Limited (HBL) reported the highest NPL at 7.39%.

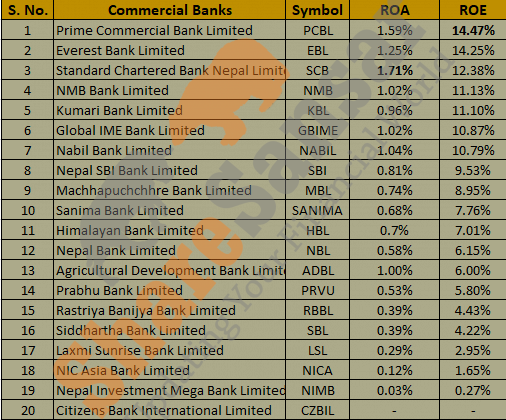

Return on Assets (ROA) & Return on Equity (ROE):

Prime Commercial Bank Limited (PCBL) recorded the highest ROE at 14.47% and Standard Chartered Bank Nepal Limited (SCB) reported the highest ROA at 1.71%.

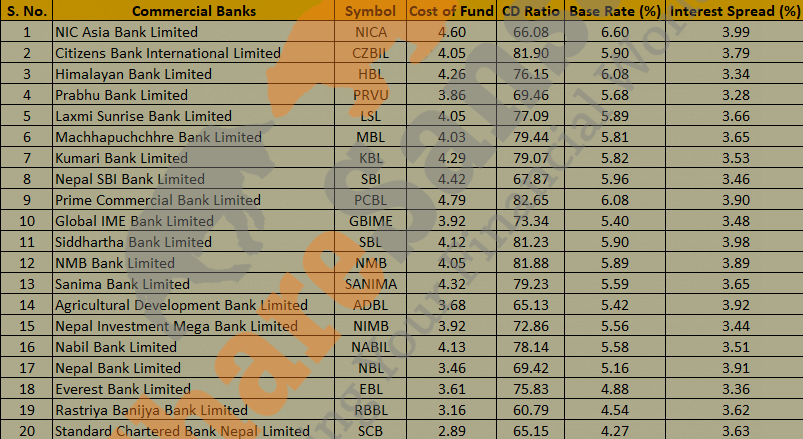

Additional Indicators: Cost of Funds, CD Ratio, Base Rates, and Interest Spread

- Cost of Funds: Prime Commercial Bank Limited (PCBL) reported the highest cost of funds at 6.36%, with Standard Chartered Bank Nepal Limited (SCB) having the lowest at 2.89%.

- CD Ratio: NMB Bank Limited (NMB) had the highest CD ratio at 82.65%, while Rastriya Banijya Bank Limited (RBBL) had the lowest at 62.39%.

- Base Rate: NIC Asia Bank Limited (NICA) had the highest base rate of 6.60%, and Standard Chartered Bank Nepal Limited (SCB) reported the lowest at 4.27%.

- Interest Spread: The average net interest spread across commercial banks was around 3.2% to 3.9%.

The table below provides a detailed overview of these financial indicators across the 20 commercial banks for Q1 FY 2082/83.