Kalinchock Hydropower to Issue IPO from Chaitra 22; In Depth Analysis of Company Performance

Thu, Mar 26, 2026 12:57 PM on IPO/FPO News, Highlight News, Company Analysis, National,

Kalinchock Hydropower Limited (KHL) was incorporated on May 19, 2016 as a private limited company and later converted into a public limited company on June 15, 2022. The company is developing a 5 MW Run-of-River Sangu (Sorun) Khola Hydroelectric Project (SKHP) in Dolakha District, Bagmati Province, Nepal, under the BOOT (Build, Own, Operate, and Transfer) model. The project has a signed Power Purchase Agreement (PPA) with the Nepal Electricity Authority (NEA) and is being financed under a 70:30 debt-to-equity structure, with a total estimated project cost of approximately NPR 1,030 million. The company's current paid-up capital stands at NPR 550 million post-IPO, with RBB Merchant Banking Limited serving as the Issue Manager for the public offering approved by SEBON.

Board of Directors:

|

S.N. |

Name |

Designation |

|

1 |

Indira Panta |

Chairman |

|

2 |

Tanka Lal Shrestha |

Director |

|

3 |

Hari Prasad Tiwari |

Director |

|

4 |

Bhabani Pokharel |

Director |

|

5 |

Ramchandra Upreti |

Director |

About the Issue and Rating:

Kalinchock Hydropower Limited is issuing 13,75,000 ordinary shares at Rs. 100 par value, representing 25% of the total paid-up capital of Rs. 55 Crores. The issue is structured across two phases the first targeting project-affected locals of Dolakha District and Nepalis in foreign employment, and the second for the general public. The company has been assigned a CARE-NP BB issuer rating by CARE Ratings Nepal Limited, indicating a moderate risk of default in meeting financial obligations on time, valid until July 6, 2026.

IPO Issue Details:

|

Particulars |

Details |

|

Total Issued Capital |

Rs. 55 Crores (55,00,000 shares) |

|

Total Public Issue |

Rs. 13.75 Crores 13,75,000 shares (25%) |

|

Par Value per Share |

Rs. 100 |

|

Project-Affected Locals |

5,50,000 shares (10%) |

|

Nepalis in Foreign Employment |

82,500 shares |

|

General Public |

6,84,750 shares |

|

Issue Manager |

RBB Merchant Banking Limited |

|

Issue Date |

22 Chaitra, 2082 |

Financial Performance:

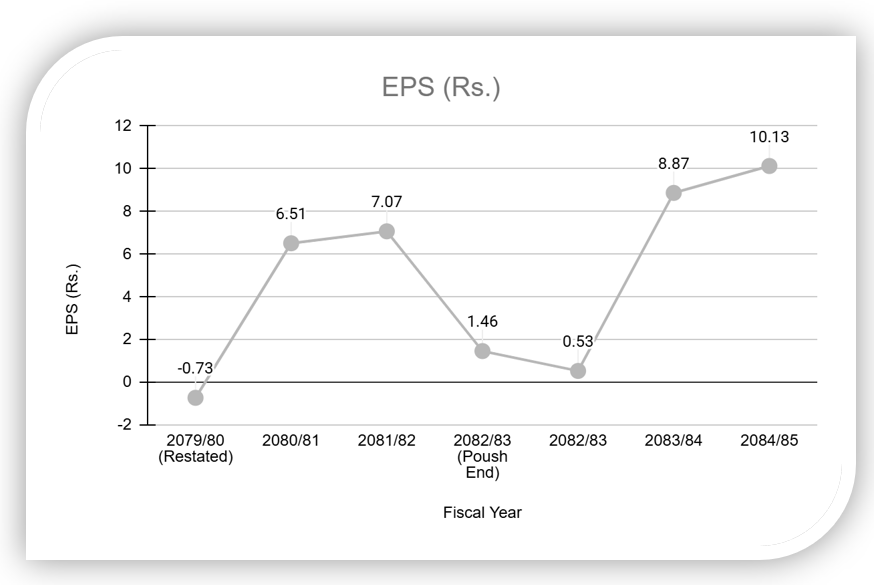

1. Earning Per Share (EPS): FY 2079/80 to Projected 2084/85

The company reported a loss of Rs. 0.73 per share in FY 2079/80, which was the early construction phase. It recovered strongly to Rs. 6.51 in 2080/81 and Rs. 7.07 in 2081/82, reflecting improving pre operational income and reduced losses. The projected EPS dips to Rs. 0.53 in 2082/83 the year of commercial operation commencement primarily due to heavy interest and depreciation charges in the initial production year. However, it is projected to grow significantly to Rs. 8.87 in 2083/84 and Rs. 10.13 in 2084/85 as revenue stabilises and debt servicing normalises, reflecting the long-term earnings potential of the project.

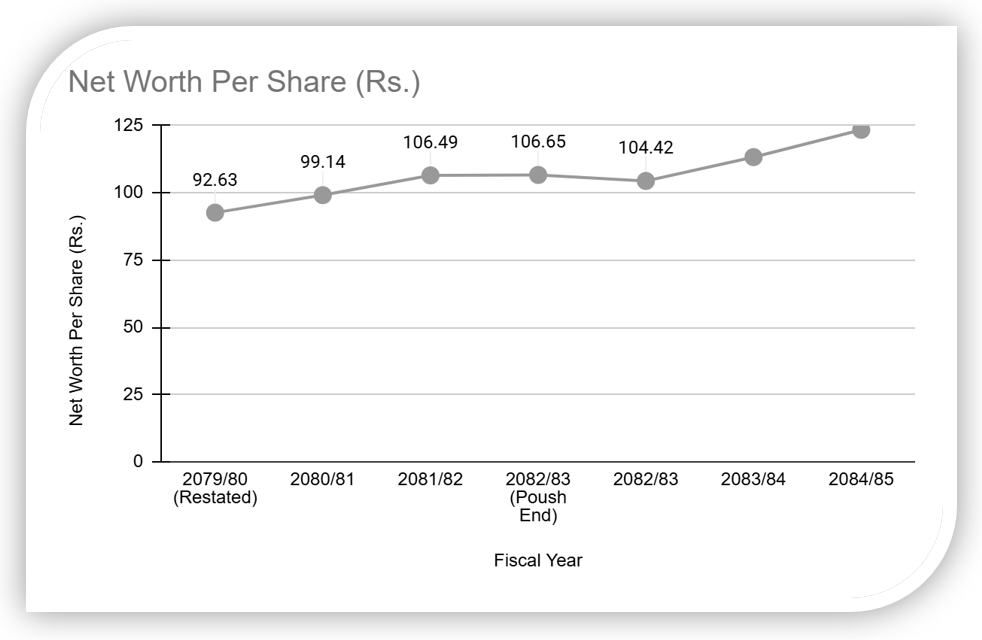

2. Net Worth Per Share: FY 2079/80 to Projected 2084/85

The net worth per share of Kalinchock Hydropower Limited has shown a steady upward trend from Rs. 92.63 in FY 2079/80 to Rs. 106.65 as of Poush end 2082/83, reflecting consistent accumulation of retained earnings during the construction phase. It slightly dips to Rs. 104.42 in the projected full year of 2082/83, which coincides with the commercial operation commencement year and associated initial year financial pressures. Thereafter, it is projected to grow to Rs. 113.29 in 2083/84 and Rs. 123.43 in 2084/85, consistently remaining above the par value of Rs. 100 indicating that the company's book value per share is healthy and investor equity is well protected throughout the projection period.

Financial Highlight:

|

Particulars |

Actual |

Estimated |

|||

|

2080/81 |

2081/82 |

2082/83 |

2083/84 |

2084/2085 |

|

|

Total Non-Current Assets |

364,799,309 |

881,124,638 |

1,260,299,266 |

1,216,840,671 |

1,173,382,075 |

|

Total Current Assets |

108,875,805 |

88,241,883 |

182,193,502 |

230,252,185 |

282,090,472 |

|

Total Assets |

473,675,113 |

969,366,521 |

1,442,492,768 |

1,447,092,856 |

1,455,472,547 |

|

Share Capital |

225,000,000 |

330,000,000.00 |

550,000,000.00 |

550,000,000.00 |

550,000,000.00 |

|

Others Captial |

-1,934,794 |

21,406,683 |

- |

- |

- |

|

Reserve Surplus |

- |

- |

24,323,805 |

73,112,244 |

128,851,454 |

|

Total Current Liabilities |

53,629,346 |

62,183,762 |

82,306,745 |

86,405,744 |

90,701,798 |

|

Total Equity & Liabilities |

473,675,113 |

969,366,521 |

1,442,492,768 |

1,447,092,856 |

1,455,472,547 |

|

Net Profit |

14,651,599 |

23,341,477 |

2,917,122.00 |

48,788,439.00 |

55,739,211.00 |

Note: All the financial data are extracted from the prospectus of the company presented to the SEBON

Risk vs Return:

Kalinchock Hydropower Limited's IPO at Rs. 100 par value presents a classic risk return trade off typical of early stage hydropower investments. On the risk side, the CARE-NP BB rating, high 70:30 debt-to-equity ratio, single asset concentration, and a projected profit collapse to just NPR 29.17 Lakhs in 2082/83 signal that short-term returns will be under pressure, with little to no dividend expected in the first 1/2 operational years. However, these risks are substantially offset by strong return fundamentals, a guaranteed take or pay PPA with NEA, annual tariff escalations of 3% for up to 8 years, EPS recovery to Rs. 10.13 by 2084/85, and Return on Equity climbing to 15.6% over the projection period. The IPO at par price means investors are not overpaying, and the project's near complete construction status (83% done) minimises execution risk. In summary, the short term pain is real but temporary, while the long term return profile is attractive making this IPO a moderate risk, good return proposition for patient, long term investors willing to hold through the initial operational adjustment phase.