Can Nepal’s Banks Afford to Ignore Nature-Related Risks?

The economy and the financial system, through their loan exposures to projects, have a dual relationship with nature. They not only depend on it, but they can also affect it and be affected. This can give rise to nature-related risks, driven by the degradation, encompassing the loss of biodiversity and ecosystem services.

A 2025 international study reported in The Guardian and published in Ambio, Nepal, as the world’s most “nature-connected” nation. It shows that nature is closely connected to the lives of people in Nepal in social, religious, environmental, cultural, and financial ways. From low altitude Terai plains to the high Himalayas, the nature is not only a scenery but the foundation of our lives and livelihoods. Many livelihoods coexist and mutually benefit one another. The example of community-based forest management is the prime example in the world. When societies lose that connection, biodiversity declines and materialism rises.

In Nepal today, the problem is not a lack of love for nature or the connection thereof, but that our financial decisions rarely reflect that love. Nature impacts, dependencies, risks, and opportunities remain invisible in most lending decisions. The time has come for banks and financial institutions (BFIs) to recognize that protecting nature is not merely a matter of Corporate Social Responsibility (CSR) but an economic necessity.

Missing Link Between Nature and Financial Institutions

Nepal’s economy is deeply rooted in its natural capital. According to the World Wide Fund for Nature (WWF), forests cover more than 44% of the country’s total land area, forming the foundation of rural livelihoods and ecological stability.

Nepal Rastra Bank (NRB) mandates that ‘A’ class commercial banks have to allocate 40% of total loans to priority sectors by the end of Asadh 2084. The priority sectors include agriculture and micro cottage small, and medium enterprises. And the energy sector should get at least 10%, and 5% to low-income households. In the case of development banks and finance companies, it is required to allocate a minimum of 20% and 15%, respectively, to agriculture, MSMEs, energy, and tourism, along with 5 percent to low-income households within the same timeframe. These priority sectors are directly or indirectly dependent on Nepal’s natural resources.

The World Bank’s 2025 assessment further highlights that agriculture, forestry, and ecotourism together support the majority of Nepal’s population, with farming alone employing around 61% of the national workforce. Despite this dependence, nature’s value remains largely invisible in financial decision-making.

BFIs continue to fund hydropower projects, farms, and infrastructure without fully considering how damage to the environment could harm those investments. When watersheds are damaged or rainfall patterns shift, hydropower output falters, agricultural yields decline, and loan performance suffers. Insurance claims worth NRs 11.82 billion have been filed to cover damages caused by the monsoon disasters on September 27 and 28. According to the Nepal Insurance Authority, 3,418 claims have been submitted across various sectors, and NRs 610.79 million have been reimbursed to the victims after loss assessments were completed as of mid-November.

These environmental risks of the BFIs have been managed through the ESRM Guidelines & Green Finance Taxonomy published by the NRB. However, the nature-related risks are faintly accommodated in the credit due diligence and mitigation.

Relation between Ecology and Economy:

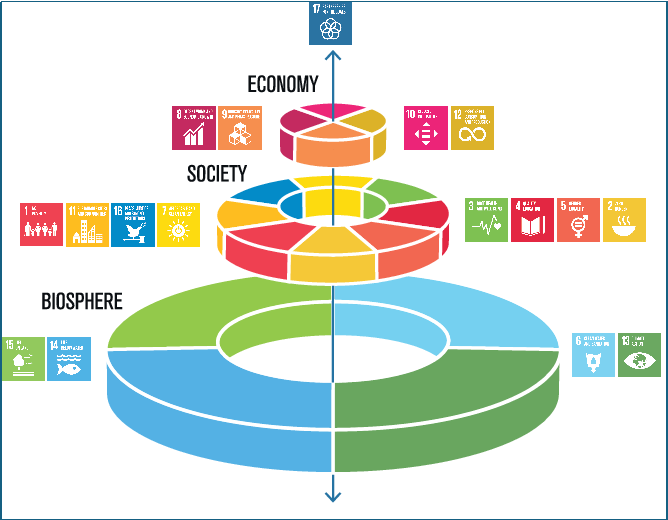

The Sustainable Development ‘Wedding Cake’ model developed by the Stockholm Resilience Centre illustrates that the economy and society are embedded within the biosphere (nature and its resources). This model demonstrates that nature serves as the foundation layer upon which social and economic activities depend.

For BFIs, this model is significant because financial performance is ultimately linked to the health of the natural ecosystem. For a country like Nepal, where mega projects like hydropower, agriculture farming, and tourism rely heavily on the functioning ecosystems and their resources. The process of integrating nature-related risks into credit loan appraisal, portfolio management, and strategic planning is not an ethical add-on but a necessity. Protecting natural capital safeguards asset quality, reduces long-term risk exposure, and supports sustainable economic growth. Consequently, there is no finance without society and no society without nature.

Figure 1: Wedding Cake model of SDG by Stockholm’s Resilience Centre

Understanding Nature-Related Financial Risks

Nature-related financial risks are the degradation of the ecosystem that impacts the financial economy. They are linked to but distinct from climate risk. Many of these risks arise directly from human actions such as deforestation, pollution, and over-extraction of resources. These risks translate into credit, liability, market, financial, and reputational exposure.

The nature-related risks expose BFIs to multiple categories of risk.

Credit risk arises when the repayment capacity of the borrowers is weakened due to nature degradation. For example, in hydropower, deforestation in upstream area alters river hydrology leading to reduced cash flows due to lower generation effecting timely loan repayments.

Market Risk occurs when the devaluation of the assets changes as per the perception of market of demand linked to nature impacts. For example, companies heavily depend on unsustainably sourced timber and woods may see declining valuation as market shift towards certified, organic, and nature-positive products.

Liability Risk arises from the legal claims such as fines or compensation linked with environmental degradation, such as mining company facing lawsuits and remediation costs for effecting water bodies discharging untreated effluents to water bodies.

Reputational risk affects the financial institutions when its relevant stakeholders perceive their financing as harmful to nature. For example, banks financing projects inside protected areas may face public backlash, loss of clients, and reduce confidence of investor

For Nepalese banks and financial institutions, understanding both their dependence on nature and their clients’ impact on it is now fundamental to managing credit risk and safeguarding investments. Understanding and managing the investment made in the business that highly depends on the natural ecosystem is therefore critical to maintain competitiveness, ensure compliance, and secure long-term sustainability of both resources and business.

Nature-based solutions and their management through NGFT and ESRM Guidelines

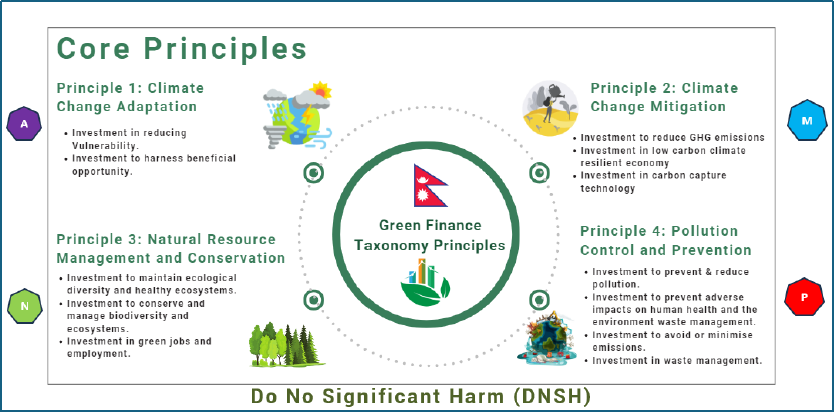

The Nepal Rastra Bank’s Green Finance Taxonomy (NGFT), introduced in 2024, represents a significant milestone in aligning the financial system with nature financing. It is a national classification system that identifies which economic activities can be considered environmentally sustainable and a low-carbon economy. One of the core principles, “Natural Resources Conservation and Management,” urges BFIs to integrate the protection, restoration, and sustainable use of ecosystems and biodiversity into their financing decisions. The classification system classifies the projects and businesses into Green (investment-ready), Amber (investment after suggestion and adoption of remedial measures), and Red (discourage activities while encouraging reshaping of investments) with the same guiding document.

Figure 2: Core Principles of Green Finance Taxonomy

The NRB issued Environmental and Social Risk Management (ESRM) Guidelines in 2018 (later revised in 2022), providing banks and financial institutions with a structured framework to identify, assess, and manage the risks associated with environmental and social aspects in their lending portfolios. This guideline has helped the BFIs to reduce or mitigate these risks, resulting in sustainable business.

NGFT and ESRM, together encourage banks to conduct environmental due diligence, integrate nature-related into credit assessments, and promote responsible investment practices. Nepal’s financial sector can systematically embed nature financing into its operations by linking the ESRM’s risk management approach with the NGFT’s taxonomy of sustainable activities. This ensures that development and conservation progress together rather than at the cost of one another.

A Wake-up Call for Nepalese BFIs

Nepal’s journey in nature financing has only just begun, presenting a unique opportunity for its BFIs to lead with purpose. In order to move from awareness to real impact, BFIs must align with proven national and international frameworks that integrate biodiversity and climate considerations into finance.

There are environmental regulations, such as Nepal Environmental Protection Act/Rules, Hydropower Development Policy, National Climate Change Policy, Forest Act, Water Resources Act, and other international agreements that drive the business with compliance and sustainable resources. However, BFIs barely assess compliance with these rules and regulations, exposing themselves to non-financial risks. To address such risks, the banks must increase their institutional capacity to incorporate these risks into a long-term profitable business.

The BFIs should not only deep dive into ESRM and NGFT but also cater to international best practices as well. Adopting global frameworks such as the Taskforce on Nature-related Financial Disclosures (TNFD) can help financial institutions assess their dependencies and impacts on nature. TNFD provides a framework to understand and report how nature affects their operations and investments. It is built on four key pillars: Governance, Strategy, Risk & Impact Management, and Metrics & Targets. The TNFD also provides additional guidance for identifying and assessing nature-related risks using the LEAP methodology. The LEAP stands for Locate, Evaluate, Assess, and Prepare.

- Locatethe interfaces with nature across geographies, sectors, and value chains;

- Evaluatedependencies and impacts on nature;

- Assessnature-related risks and opportunities to your organization; and

- Prepareto respond to nature-related risks and opportunities, including reporting on material nature-related issues to the primary users of financial reports and other stakeholders, aligned with the TNFD’s recommended disclosures

By adopting these national and international guides, Nepal’s banks can strengthen their portfolios and their role in promoting sustainable, nature-positive finance.

Conclusions

Nepalese BFIs can protect Nepal’s rich natural resources and become true leaders in nature-positive finance by following these global initiatives. This is not only about doing good but about protecting the foundation of our economy. The role of BFIs stands at critical junction to safeguard biodiversity, mitigate nature-related risks to ensure long-term economic resilience of the country by integrating the nature into lending and investment decisions. This not only ensure the green economy but balances the sustainable profit as well as protecting the planet, ensuring the sustainable use of Nepal’s natural resources for future generation. So, the message for Nepal’s financial sector is clear and urgent: The time to act is now.

Ram Parajuli & Prabin Kumar Kafle

Ram Parajuli works in the Environmental and Social Risk Management Unit at Global IME Bank, Nepal, focusing on ESG integration, sustainable finance, and responsible investment practices.

CA Prabin Kumar Kafle is a GARP-certified Sustainability and Climate Risk Professional, law graduate, and climate advocate with over five years of experience in banking, finance, and sustainability.