Baisakh’s rise in NEPSE and outstanding performance of commercial banks! What will be your investment decision after comparing the performance on the basis of Q3 reports of commercial banks?

Tue, May 14, 2019 4:32 PM on Exclusive, Financial Analysis, Stock Market, Latest,

-Dheerusha Tiwari

-Dheerusha TiwariThe third quarter of fiscal year 2075/76 has come to an end. Baisakh month witnessed the rise in NEPSE index from 1180 to around 1320 level. “A” graded 28 commercial banks of the country have published their reports. Experts have anticipated the stock market might have entered the bullish zone. Given the circumstances, let us compare each of these commercial banks on the basis of third quarter reports of FY 2075/76.

The following are the key elements necessary in analyzing the third quarter performance of commercial banks:

- Net profit:

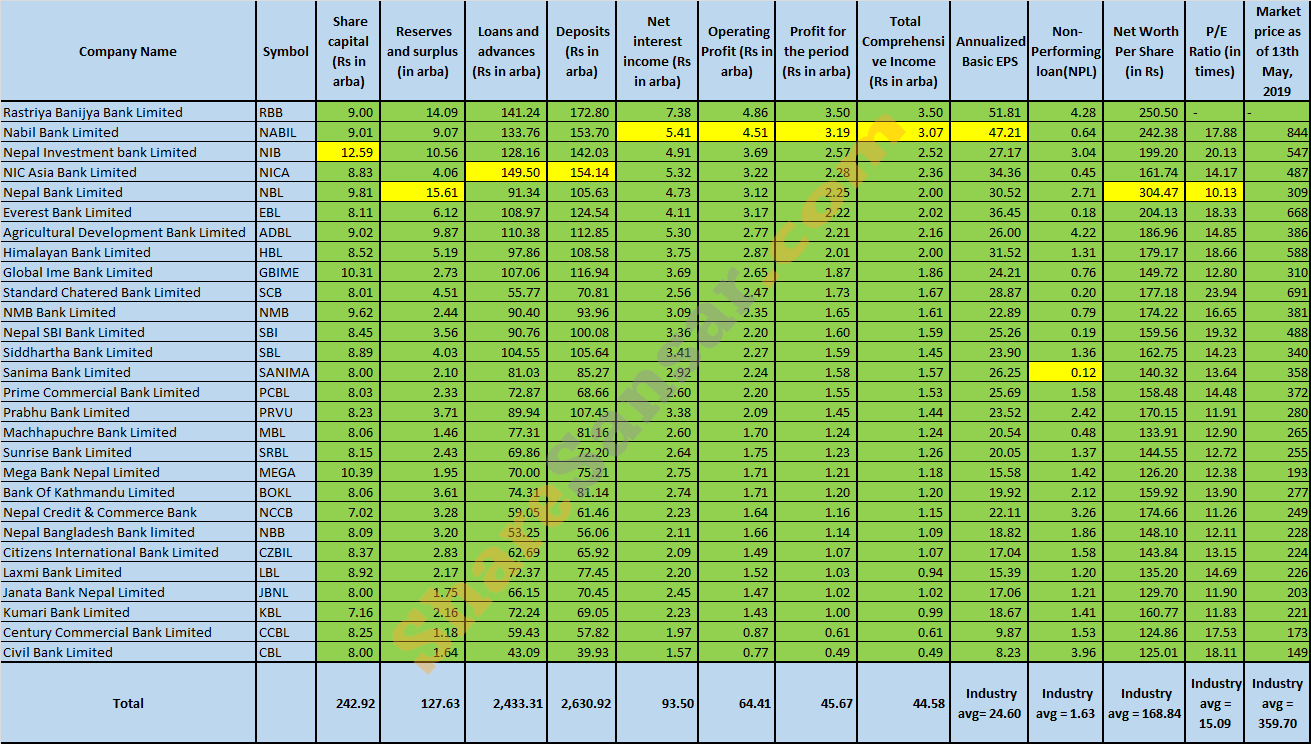

As per the net profit of third quarter of 2075/76, Rastriya Banijya Bank (RBB) is in the lead with a profit of Rs 3.50 arba. Similarly, NABIL Bank Limited (NABIL) has the second highest net profit of Rs 3.19 arba in the same quarter. In the third position, Nepal Investment Bank Limited (NIB) has the net profit of Rs 2.57 arba. The bank with the least net profit is Civil Bank Limited (CBL) whose net profit amounts to Rs 49 crore.

The industry average net profit of the 28 commercial banks is Rs 1.63 arba. 11 commercial banks have net profit above the industry average. Remaining all banks has net profit below the industry average.

Compared to the same quarter of last year, NIC Asia Bank Limited (NICA) has significantly increased its net profit by 144%. Similarly, Mega Bank Limited has increased the profit by 131.33%.

In the Nepal Financial Reporting Standards (NFRS) format of financial statements, investors will find several types of income and profits. For instance, profit for the period, comprehensive income, distributable profit, profit after regulatory adjustments, etc. However, the actual profit can be determined through specimen “profit/loss for the period” of financial statement.

- Paid up capital:

Paid up capital in NFRS refers to the amount of money that commercial banks have received from their shareholders through the exchange of shares in the primary market. The central bank of the country has directed these “A” categorized banks to meet the paid up capital requirement of at least 8 arba. Nepal Credit and Commercial Bank (NCCB) and Kumari Bank Limited (KBL) are still to meet the paid up capital requirement. However, Kumari bank has already endorsed 21.25% bonus for last two FY and yet the bonus amount i.e. Rs 1.52 arba left to be adjusted in paid up capital in the published quarterly result.

The bank with highest paid up capital are Nepal Investment Bank (NIB) with Rs 12.59 arba capital, Mega Bank Limited (MEGA) with Rs 10.39 arba and Global IME Bank Limited (GBIME) with Rs 10.31 arba paid up capital.

- Reserve and surplus:

With an industry average of Rs 4.56 arba, seven banks stand above the average benchmark of Rs 4.56 arba in their reserve fund.

In terms of reserves and surplus, Nepal Bank Limited (NBL) has maintained its lead with a reserve and surplus of Rs 15.61 arba. Rastriya Banijya Bank (RBB) has maintained second position with Rs 14.09 arba reserve and surplus fund. Nepal Investment Bank Limited (NIB) is in the third position with reserve and surplus of Rs 10.56 arba. The bank with least reserve and surplus is Century Commercial Bank Limited (CCBL) with a reserve of Rs 1.18 arba.

- Deposit collection:

In an average, commercial banks have collected Rs 93.96 arba as deposit. Only 13 banks are above the average deposit collection.

In the banking sector, the deposit collection will play a major role in the upcoming days. Lack of liquidity is the major concern among most of the commercial banks. So, those banks which are able to retain deposit or increase deposit collection are likely to perform better in the days to come.

As of the third quarter of FY 2075/76, Rastriya Banijya Bank (RBB) stands on top with total deposits worth Rs 1.72 kharba. NIC Asia Bank Limited (NICA) is aggressively involved in collecting deposits from existing and prospective clients with deposits of Rs 1.54 kharba. Similarly, the bank is followed by NABIL Bank Limited (NABIL) with the collected deposit of Rs 1.53 kharba respectively. Civil Bank Limited (CBL) has the lowest deposit collection of Rs. 39.93 arba only.

The average deposit collected by the industry is Rs 93.96 arba.

- Loans and advances:

In today’s context, the concern of investor simply does not rest upon which bank has more loans. The nature of loan portfolio equally matters. The table below shows the accumulated loans which includes loans to BFIs and loans to customers. As shown in the figure, the top position in loans and advances is occupied by NICA Bank Limited (NICA) with credit disbursement worth Rs 1.49 kharba. Rastriya Banijya Bank (RBB) has a loan and advances portfolio of Rs. 1.41 kharba. Nabil Bank Limited (NABIL) has the loan portfolio of Rs 1.33 kharba. Similarly on the other end of the rope, stands Civil Bank Limited (CBL) with the lowest loan and advances portfolio of Rs. 43.09 arba.

The industry average loan disbursed is Rs 86.90 arba. 13 commercial banks have the loan portfolio above Rs 86.90 arba.

- Net interest income:

Net interest income is the net earnings of commercial banks through their core business of collecting deposits and lending loans. The bank with highest net interest income is Rastriya Banijya Bank (RBB) with income of Rs 7.38 arba followed by Nabil Bank Limited (NABIL) with income of Rs 5.41 arba and NICA Bank Limited (NICA) with income of Rs 5.32 arba.

The industry average net interest income stands at Rs 3.34 arba. 12 out of 28 commercial banks are above the industry average in terms of net interest income.

Nepal Credit and Commerce Bank increased net interest income by the highest percentage of 120.69% as compared to net profit of the same quarter in the previous year. It is further followed by Mega Bank Limited.

- Operating profit:

Rastriya Banijya Bank (RBB) has been able to build the topmost rank in terms of operating profit. The bank attained Rs 4.86 arba solely as profits from operating activities. Nabil Bank Limited (NABIL) secured a profit if Rs 4.51 arba in the third quarter of this fiscal year. Finally, Nepal Investment Bank Limited (NIB) secured an operating profit of Rs 3.69 arba. The industry average is Rs 2.30 arba with 11 banks above the average benchmark.

The change in operating profit compared to the same quarter in the previous year has been provided in the table below:

- Total comprehensive income:

Rastriya Banijya Bank (RBB) has also highest comprehensive income of Rs 3.50 arba. Nabil Bank Limited (NABIL) has the second highest comprehensive income of Rs 3.07 arba. Nepal Investment Bank Limited (NIB) has the third highest comprehensive income of Rs 2.52 arba.

Major indicators:

- Earnings per share (Annualized):

Rastra Banijya Bank (RBB) becomes the bank to serve investors with highest annualized EPS of Rs 51.81 per share. Nabil Bank Limited (NABIL) has the second highest EPS of Rs 47.21 per share. Everest bank limited (EBL) in the third position with annualized EPS of Rs 36.45 per share. Civil Bank Limited (CBL) stays at the bottom with an earning of Rs. 8.23 per share.

The average EPS of 28 commercial banks stands at Rs 24.60. 13 commercial banks still provide EPS higher than that of the industry average.

- Net worth per share:

The highest net worth per share among these commercial banks is Rs 304.47 which belongs to Nepal Bank Limited (NBL). Rastriya Banijya Bank (RBB) is in the second position with Rs 250.50. Nabil Bank Limited (NABIL) has the third highest net worth per share as of Q3 of FY 2075/76 i.e. Rs 242.38. Century Commercial Bank Limited (CCBL) has the least net worth of Rs 124.86 per share.

The industry average net worth stands around Rs 168.84 per share. 11 companies have net worth more than the industry average.

- P/E ratio:

Nepal Bank Limited (NBL) has the least PE ratio of 10.13 times. It is followed by Nepal Credit and Commerce Bank (NCCB) with PE ratio of 11.26 times and finally Kumari Bank Limited (KBL) has third least PE ratio of 11.83 times. Only NCCB is yet to meet the paid up capital requirement.

17 commercial banks have a P/E ratio lower than the industry average of 15.09 times.

- Non-performing loan:

Bad loans cost commercial banks a lot of money. Commercial banks need to be able to minimize their non-performing loan. Sanima Bank Limited (SANIMA) has the least NPL of 0.12. Finally, Everest bank Limited (EBL) has the second least NPL of 0.18. The overall commercial banking industry has average NPL of 1.58.

In a nutshell:

Finally the table below provides a full picture with major indicators of the 28 commercial banks as of the third quarter of FY 2075/76:

Note: Rastriya Banijya Bank Limited has been excluded while labeling yellow color for the best ranking because Rastriya Banijya Bank has not been listed in NEPSE.

Dear investors, please feel free to share your investment decision after the performance evaluation of key indicators of these commercial banks.