Till when commercial bank will be on aggressive mode in expanding loans? Exclusive study based on CAR and CCD ratios

Mon, Feb 25, 2019 1:29 PM on Economy, Exclusive, Stock Market,

Aakriti Thakali

It’s been almost three years of loanable fund shortage in the financial market of Nepal. Surely there were times of ease, but if we see the big picture there always has been a mis-match between the deposits and lending ratio. The most basic principle of economics says that in a free market, the demand and supply of funds always interacts with each other to determine the equilibrium interest rate and the quantity of funds floated in the market. We often hear the expression “It’s Nepali time”, which means the actual thing will happen later than the stated time. We are slow, we admit that but are we really this slow that the deposit and lending balance requires more than 3 years to take form?

However, we also must take other things into consideration. First, there is no FREE MARKET, just the illusion of it. The repetitive gentlemen’s agreement on rate fixation is one evidence. Secondly, the extensive blame shifting game that has created a vicious circle where none has fully accepted that they are at fault.

REGULATORY FRONT

We often hear from regulatory body’s personnel that this shortage is the result of bankers’ carelessness (might as well say over-ambitiousness), as they started lending on the hopes but getting deposits in future. But business isn’t run on hopes, is it?

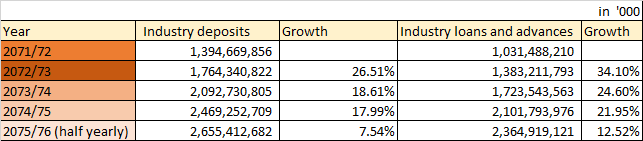

The below table shows the growth of deposits and lending of the commercial banks over the years:

As seen in the table above, we can see that for each consecutive year, the growth in loans and advances is higher than the growth in deposits. That is the first clear sign of disbalance.

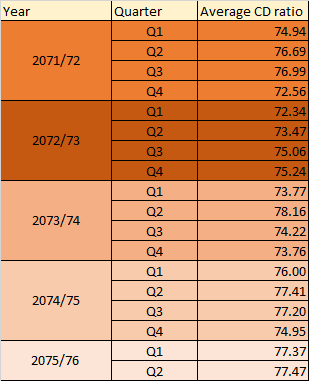

Similarly, the other thing we need to look at is the CD ratio of the commercial banks.

As shown in the table above, the average CD (credit to deposit) ratio of commercial banks had gone down to around 72% from 76% during the earthquake and the embargo period. Then, with minor fluctuation here and there, the ratio has started to rise from FY 2074/75 till now.

According to the directive set by the Nepal Rastra Bank, the commercial banks must maintain a credit to core capital-cum-deposit ratio at 80%. This means that if the bank is already at 80%, then to lend further they will have to raise further deposits. However, the banks’ CD ratio itself has reached 77% by now, which means that the CCD ratio is not very far from the limit. So, the question again is – until when the banks are going to remain aggressive in lending?

2072 Baisakh marks the date of devasting earthquake and that is the year when the entire economy took a hit. The first year after earthquake and the embargo went by to reinvigorate the system. Despite that, the commercial banks reported 26% rise in deposits and 34% rise in lending.

The year after that also showed huge demand for loanable funds as people had now started to stand on their own feet. There was demand in the productive sector, construction sector and surprisingly also from import-based companies as they had started to thrive from the ashes of embargo’s suffering and rapid rise in imports.

Thus to meet this demand, banks started to lend more and in that year the deposits rose by 18% whereas the lending rose by a solid 24%. Then as the year followed, the gap stayed leading to liquidity shortage in the market. Even as per the Q2 data of this year, the growth in lending is higher than the deposits growth.

Then, again on Shrawan 21, 2072 NRB issued the directive whereby the Commercial Banks had to increase their capital by 4 fold to Rs 8 arba along with all other BFIs (development banks, finance companies, microfinance companies, Insurance companies). The main goal, as NRB says, was to consolidate the sector and few banks went for merger too. However, the rest went for either bonus shares, right shares or Further Public Offering (FPO) to increase their paid-up capital.

The catch is, it doesn’t limit to capital increment the bank now also needs to generate enough profit to serve that increased capital and what is the source of their earnings? Loans and advances.

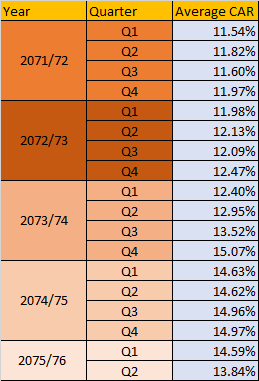

As of CAR (Capital Adequacy Ratio) Framework, 2015, commercial banks are required to maintain CAR of 11%. The CAR ratio is calculating the total capital (tier 1 and tier 2) by the risk weighted assets. The risk weighted assets of banks is represented by the quality of loans or credit they disburse. Higher the risk, higher the weight.

So when the capital went up by four folds, the CAR also increased and that gave commercial banks space to lend more.

We can clearly see from the above table that the average CAR (before NRB directive to increase paid up capital in 2072) is near to 11% which is the minimum requirement set by NRB. We can also see that the CAR has increased maximum at end of FY 2073/74, which marks the deadline by which the banks had to meet the requirement.

So far, despite shortages banks have maintained their operations but for how long can they be aggressive in lending?

BANKERS’ FRONT

That was what the regulatory body had to say in their defense and as we can see there is enough evidence to back it too. However, from the other end of the table, the bankers often lament that if the government did their capital expenditures on time then that would ease the situation. This is also true, according to NRB’s macroeconomic data of 6 months, the capital expenditure done by government is only 20% of the estimated expenditure. So when the funds aren’t being mobilized in the market, then how can we achieve the growth that we have targeted.

Looking from a broader perspective, we keep on blaming government about their inefficiency in timely utilization of capital expenditure. But we need to be aware about the fact that this problem of government has been there since decades while the problem of loanable funds shortage has been here for 3 years now.

We do need to poke government to be more effective and efficient, but in this matter instead of pointing the government only, we can also see the desire of commercial banks to earn more profit by expanding loans in short term causing this problem.

Here we can also see the failure of NRB’s directive to meet its intended purpose of raising paid up capital by 4 fold in such short term. This is the very reason that has given banks the confidence to be extra aggressive. The aggressive growth strategy and the fight between BFI’s to get the limited deposit available in the market has resulted in rising interest rates since last 2 fiscal year.

Similarly, the other argument bankers present is “too much regulation” and not enough room to breathe. The banking industry has a very high systemic risk, so one bank falls the chances that it will pull down other banks with it is also high. Due to this fact, the banking sector today is the most regulated sector. Some of the requirements that commercial banks need to follow are:

- Minimum capital requirement of Rs 8 arba

- Capital adequacy ratio of 11%

- CCD (Credit to core capital cum deposit) ratio of 80%

- Cash reserve ratio (CRR) and Statutory Liquidity Ratio (SLR) of 4% and 10% respectively

- Minimum 25% of total lending in priority sector

Important takeaways

The CAR of banks is still above the mandated 11% due to increased capital cushion. This shows they still have appetite to more risk by expanding their business and lending. The trend shows falling CAR from the start of 2074/75 and the average CAR as of second quarter of 2075/76 stands at 13.84%. So in near future, the banks will have to shift to defensive mode to maintain their CAR at the policy level.

This leads us to infer that, although the banks’ lending has been growing pretty aggressively we can anticipate slow-down next year onwards. However, if there is increased supply of funds in the system or their capital is raised further then the CAR will further add room for more risk.

As long as the Capital stays and the deposits don’t show significant rise, the CAR will surely hit the floor of 11%. Once the CAR comes at the minimum level, the mis-match between deposits and lending portfolio will come into balance and when that balance is attained the interest rates will also stabilize.

It has surely been a long time since the onset of loanable funds shortage, but now, as we can see from the trends, if all the associated parties play by the rules and avoid unhealthy competition, stability can be achieved.

So once again, till when the banks will be aggressively lending? I think we know the answer now.

From next year, we can expect that the growth of loan and advances will align with the growth of deposit in the banking sector. This will also subdue the pressure on interest rates.