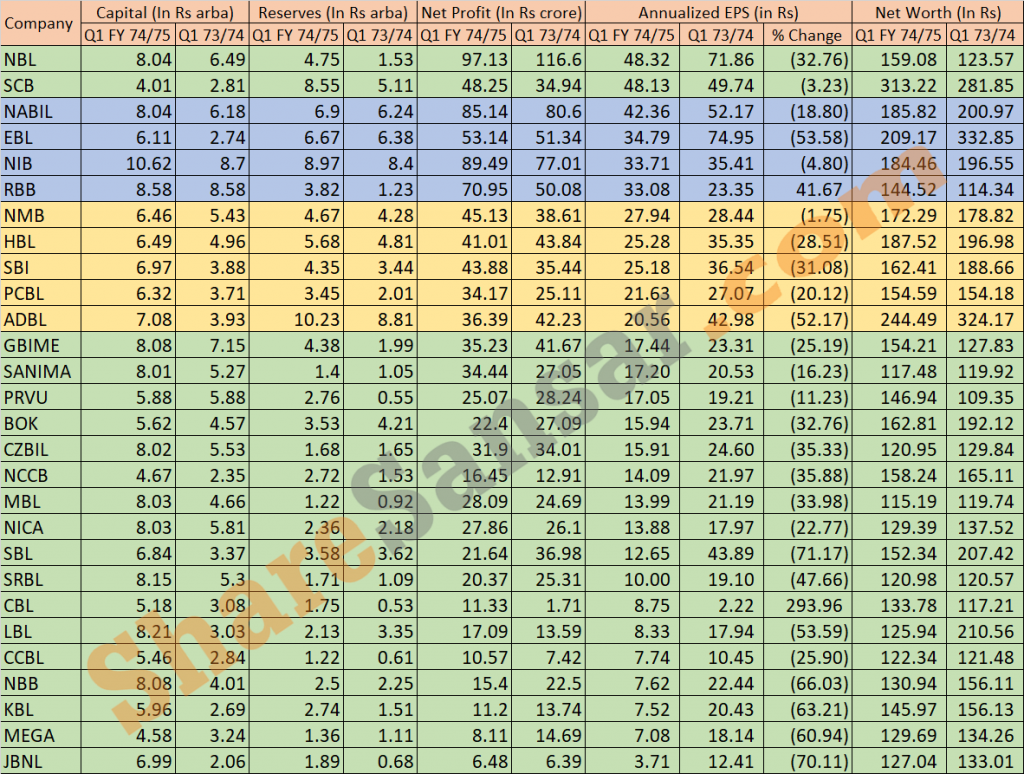

All 28 commercial banks of Nepal have published their financial statements till the end of first quarter of the current fiscal year FY 2074/75. It is the matter of interest of all the investors to analyze the important fundamentals of the commercial banks. Thus, for an ease to investors and all visitors of our website, we have made table with major fundamentals factors like paid up capital, reserves, net profit, earning per share (EPS), net worth per share of Q1 of the FY 2074/75 and Q1 of the FY 2073/74 in the below table:

From the above table, it is concluded that Nepal Bank Limited (NBL) and Standard Chartered Bank Limited (SCB) topped the table in terms of EPS with Rs 48.32 and Rs 48.13 respectively. NBL has already fulfilled the capital requirement of Rs 8 arba by issuing 40% right shares where SCB should hike its capital by Rs 3.99 arba (around 100%). NBL has earned highest net profit among commercial bank of Rs 97.13 crore.

Likewise, there are 4 banks namely Nabil Bank Limited (NABIL), Everest Bank Limited (EBL), Nepal Investment Bank Limited (NIB) and Rastriya Banijya Bank Limited (RBB) whose EPS ranges above Rs 30. They have earned Rs 42.36, Rs 34.79, Rs 33.71 and Rs 33.08 respectively.

Similarly, 5 Commercial banks, NMB Bank Limited (NMB), Himalayan Bank Limited (HBL), Nepal SBI Bank Limited (SBI), Prime Commercial Bank Limited (PCBL) and Agricultural Development Bank Limited (ADBL) succeeded to earn Rs 20 above.

Meanwhile, Janata Bank Nepal Limited (JBNL) and Mega Bank Nepal Limited (MEGA) stood at the bottom of the table with EPS of Rs 3.71 and Rs 7.08 only.

There are 17 commercial banks whose EPS is below Rs 20. Thus, it is concluded that those investors who invest capital by taking loans from Banks and Financial Institution (BFIs) may not be able to make gain from those commercial banks as rate of interest to be paid to BFIs might be higher than the return provided by those banks.

For example, if one invests by taking loan @ 15% p.a., then the return provided by the company with EPS of Rs 20 will not be able to provide dividend more than Rs 16 per share (as 20%, i.e. Rs 20*20% = Rs 4 per share will be transferred to general reserve of the bank). Thus, investor may face loss in such cases and investment in such scrip may not be profitable if one buys in the greed of dividends.