Nepal’s Microfinance Sector: Rapid Expansion Followed by Structural Slowdown

Microfinance in Nepal emerged as an important financial inclusion tool aimed at providing banking and credit access to low-income households, rural communities, small entrepreneurs, and economically marginalized groups. Before the expansion of Microfinance (MFs), a large portion of Nepal’s rural population remained outside the formal banking system and relied heavily on informal lenders charging high interest rates.

The formal development of microfinance in Nepal began after the restoration of democracy in the early 1990s, when financial sector liberalization encouraged the establishment of rural-focused financial institutions. Initially, the government introduced regional rural development banks inspired by the Grameen Bank model of Bangladesh. These institutions mainly targeted women borrowers and low-income households through group-based lending mechanisms.

This article analyzes the status of Nepal’s microfinance sector between 2012 and 2024 based on data available from the IMF Financial Access Survey. During this period, Nepal’s microfinance sector witnessed strong expansion, with sharp growth in deposits, loan portfolios, branches, and borrower size. However, recent years have shown signs of slower expansion and structural adjustment across the industry.

Major Indicators

Outstanding Deposits

Data on outstanding deposits is available from 2019 onward. Outstanding deposits of MFIs stood at NPR 85.61 billion in 2019 and increased to NPR 176.66 billion in 2024. Deposits grew by approximately 106 percent within five years, indicating rising public participation and trust in microfinance institutions.

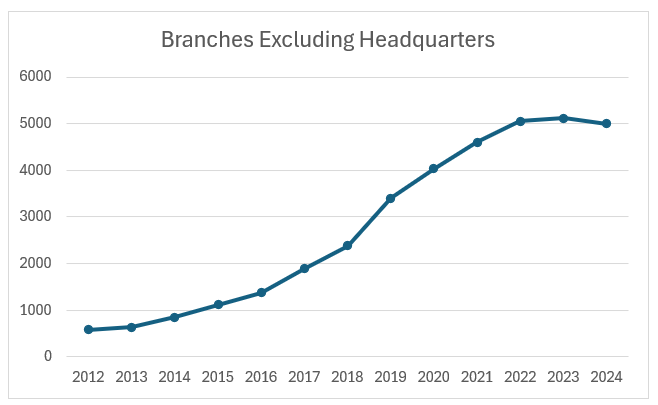

Branches Excluding Headquarters

The number of microfinance branches stood at 580 in 2012 and increased continuously to 5,121 branches in 2023, the highest level recorded during the review period. However, the number declined slightly to 4,994 branches in 2024. This decline could be associated with mergers and acquisitions among MFIs, leading to branch consolidation and operational restructuring.

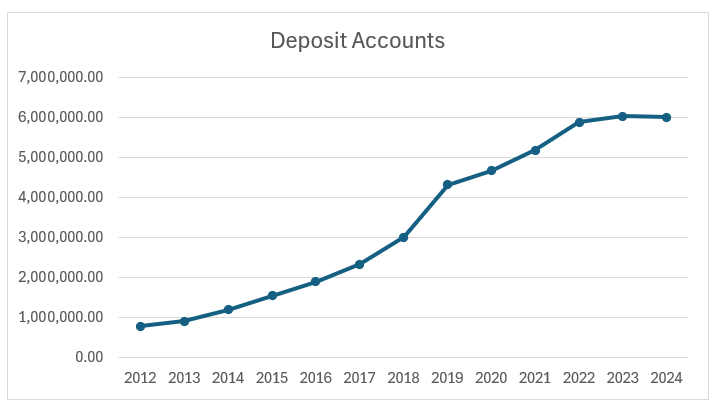

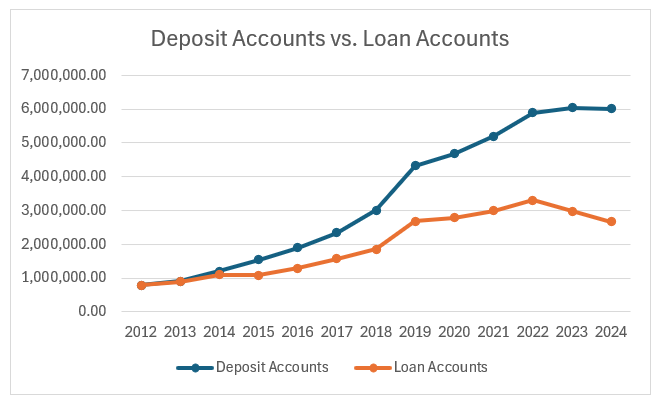

Deposit Accounts

Microfinance institutions maintained 793,362 deposit accounts in 2012, which increased to 6,015,939 by 2024. The number of deposit accounts grew at an average annual rate of around 19 percent during the review period.

The highest yearly growth was recorded between 2018 and 2019, when 1,313,791 new deposit accounts were added within a single year. However, after 2020, the growth rate of new deposit account openings began to slow, indicating signs of market saturation and slower expansion.

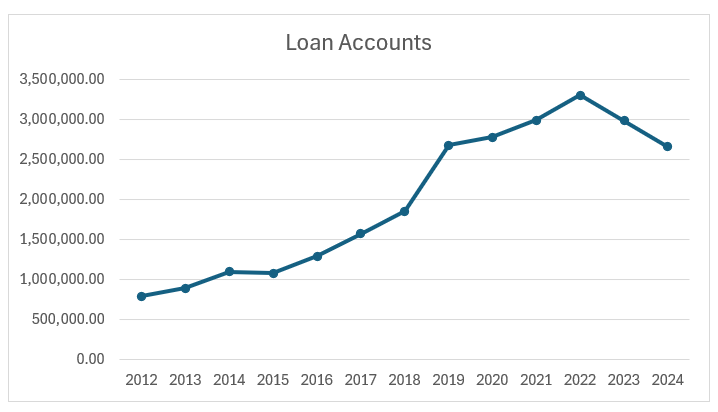

Loan Accounts

In 2012, microfinance companies had 794,195 loan accounts, which increased to 2,663,510 by 2024. The average annual growth rate of loan accounts stood at around 12 percent over the review period.

However, yearly trends show some instability. Between 2014 and 2015, during the period of Nepal’s constitution promulgation and the devastating earthquake, loan accounts declined by around 2 percent. Loan accounts reached their highest level in 2022 at 3,303,100 accounts before declining to 2,663,510 in 2024.

Deposit Accounts vs. Loan Accounts

Both deposit accounts and loan accounts followed a similar increasing trend until 2022. Afterward, deposit accounts remained relatively stable, while loan accounts started to decline. This may indicate slower credit expansion, tighter lending practices, or growing concerns over repayment capacity and multiple borrowing.

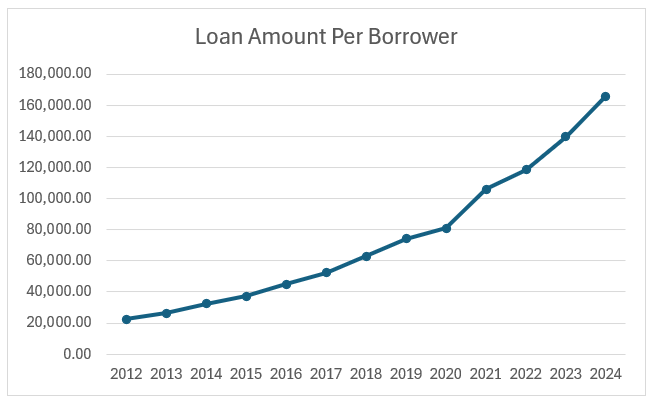

Loan Amount per Borrower

The average loan amount per borrower stood at NPR 22,335 in 2012 and increased significantly to NPR 165,805 by 2024. The average annual growth rate of loan size per borrower was approximately 18 percent.

This indicates that although the number of borrowers has slowed in recent years, the average loan size per borrower has continued to increase steadily.

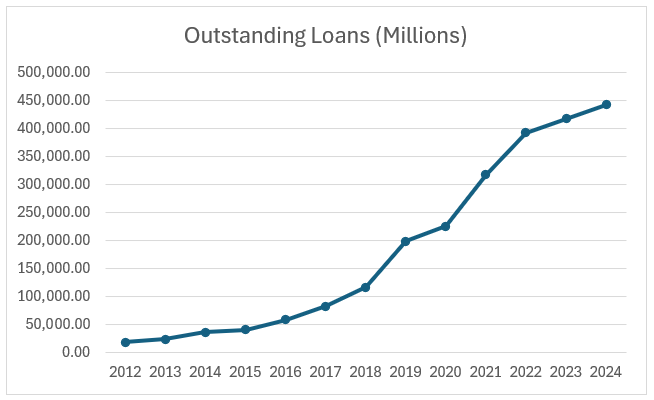

Outstanding Loans

Outstanding loans stood at NPR 17.74 billion in 2012 and increased sharply to NPR 441.63 billion by 2024. On average, outstanding loans grew by around 32 percent annually during the review period.

The trend of outstanding loans remained consistently upward throughout the period, reflecting rapid credit expansion within Nepal’s microfinance sector.

Challenges for Microfinance Institutions

- One of the major challenges for MFs is improving financial literacy among borrowers. The core target groups of microfinance institutions are poor households, marginalized communities, and low-income rural populations. These groups often have limited access to education, financial knowledge, and formal economic systems. As a result, MFs must invest additional effort in improving clients’ understanding of financial services, borrowing practices, and repayment responsibilities.

- Another challenge is geographical outreach. MFs primarily aim to provide financial access in rural and remote areas where infrastructure, transportation, communication, and financial facilities remain weak. Nepal’s scattered settlement pattern and difficult geography increase operational costs and make branch expansion more challenging.

- The slowdown in new deposit account openings suggests that the sector may be approaching stagnation in certain markets. At the same time, competition has increased significantly. Commercial banks, development banks, finance companies, and cooperatives are increasingly providing micro-level financial services and targeting small and medium enterprises (SMEs), which has intensified competition for MFs.

Conclusion

Traditionally, microfinance institutions relied heavily on borrowing from government agencies, commercial banks, and organizations involved in poverty alleviation programs. In recent years, however, MFs have also increased their focus on collecting deposits from customers, which is expected to grow further in the future.

Although the number of branches has slightly declined in recent years, this is largely linked to mergers and acquisitions among MFs, resulting in branch consolidation. At the same time, institutions are becoming more cautious regarding operational efficiency, security, and sustainable branch expansion.

While the number of deposit accounts appears relatively stagnant and loan accounts have started to decline, the average borrowing size per borrower continues to increase. This suggests that lending is becoming more concentrated toward borrowers with larger financing needs rather than expanding rapidly to new borrowers.

Overall, Nepal’s microfinance sector has experienced significant expansion over the last decade and remains one of the country’s major instruments for financial inclusion and grassroots economic participation. However, the sector is now entering a phase of slower growth, consolidation, and structural adjustment.

Note

Data used in this article is sourced from the IMF Financial Access Survey.

The analysis covers the period from 2012 to 2024.

Data for 2025 is currently unavailable and has not been included in this article.

The analysis mainly focuses on the financial indicators of Nepal’s microfinance sector.