Know the growth of non-life insurance industry in major parameters, see which insurance companies have performed better than the industry

Wed, Mar 1, 2017 11:59 AM on Latest, Exclusive, Financial Analysis, Featured, Company Analysis, Stock Market,

After the massive earthquake in 2015, general people have understood the importance of Insurance. The Insurance companies have started to expand their business as they also have understood the need. The overall Insurance sector has shown an amazing growth. With this, the Insurance Index has surged and investors are preferring it for making handsome profit.

Currently there are 17 non-life insurance companies. ShareSansar has analyzed the 2nd quarterly report of 15 listed Non-life Insurance Companies. The growth of these companies in the major parameters are then compared to the Industrial growth. The major parameters for the study are:

In the review period, the non-life insurance companies has hiked the capital by 28.66%. 6 companies were able to grow it more than the industry. Shikhar Insurance has the highest growth in the paid-up capital. After the issuance of FPO and bonus shares of 60%, its capital has almost doubled. It currently has a capital of Rs 81.76 crore. It is then followed by Premier Insurance with a growth of 56%. Lumbini General Insurance grew its capital by 33.62%. 2 Companies had a stagnant capital and it being the same as the last year.

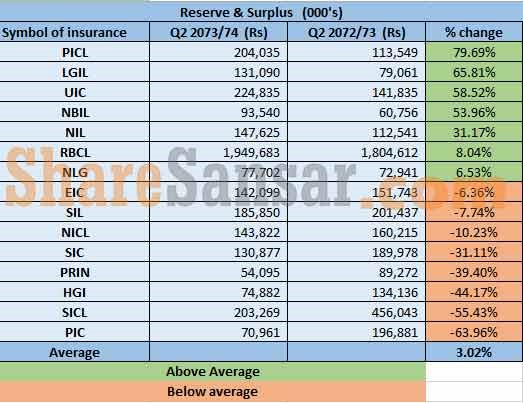

Reserve and Surplus

Huge amount of reserve shows that the company is fundamentally strong and can sustain even in the bad times. The companies can use the reserve and surplus for various purposes including the issuance of bonus shares to its shareholders. Higher growth in the reserve indicates the company will have a high net worth.

In the review period, the non-life insurance companies has hiked the capital by 28.66%. 6 companies were able to grow it more than the industry. Shikhar Insurance has the highest growth in the paid-up capital. After the issuance of FPO and bonus shares of 60%, its capital has almost doubled. It currently has a capital of Rs 81.76 crore. It is then followed by Premier Insurance with a growth of 56%. Lumbini General Insurance grew its capital by 33.62%. 2 Companies had a stagnant capital and it being the same as the last year.

Reserve and Surplus

Huge amount of reserve shows that the company is fundamentally strong and can sustain even in the bad times. The companies can use the reserve and surplus for various purposes including the issuance of bonus shares to its shareholders. Higher growth in the reserve indicates the company will have a high net worth.

In the review period, the industry amplified the reserve by 3.02%. 7 out of 15 companies had a growth more than the industry. Prudential Insurance (PICL) had the highest growth of 79.69.81%, which was closely followed by Lumbini General Insurance (LGIL) with 65.81% .

The reserve of Premier Insurance Company (PIC) dropped by massive 63.96%, 7 other companies along with Premier Insurance (PIC) had a drop in the reserve and surplus. This indicates the company provided a dividend out of its accumulated profits (Reserve and Surplus).

Insurance Fund

A company has to maintain this fund to take higher risk. 50% of net profit earned is kept aside for insurance fund and cannot be used to issue dividends to the shareholders. However, this is still the shareholders’ equity. Higher insurance fund enables the company to take higher risks and ultimately helps the company to maximize profit and shareholders’ return.

In the review period, the industry amplified the reserve by 3.02%. 7 out of 15 companies had a growth more than the industry. Prudential Insurance (PICL) had the highest growth of 79.69.81%, which was closely followed by Lumbini General Insurance (LGIL) with 65.81% .

The reserve of Premier Insurance Company (PIC) dropped by massive 63.96%, 7 other companies along with Premier Insurance (PIC) had a drop in the reserve and surplus. This indicates the company provided a dividend out of its accumulated profits (Reserve and Surplus).

Insurance Fund

A company has to maintain this fund to take higher risk. 50% of net profit earned is kept aside for insurance fund and cannot be used to issue dividends to the shareholders. However, this is still the shareholders’ equity. Higher insurance fund enables the company to take higher risks and ultimately helps the company to maximize profit and shareholders’ return.

In the review period, the Insurance Fund of the industry rose by 55.18%. 6 out of 15 companies successfully performed better than the industry. Premier Insurance company (PIC) being top in the list, rose its Insurance fund by massive 131.53%. United Insurance and Everest Insurance Company (EIC) increased to more than two folds. NB Insurance (NBIL) nearly maintained the pace with the industry.

Net Profit

It is the major indicator used by both the investors and the companies in order to determine the performance. It is the amount earned by the company after deducting all the expenses. It is the amount that helps the investors to predict the dividend and management to evaluate their performance.

In the review period, the Insurance Fund of the industry rose by 55.18%. 6 out of 15 companies successfully performed better than the industry. Premier Insurance company (PIC) being top in the list, rose its Insurance fund by massive 131.53%. United Insurance and Everest Insurance Company (EIC) increased to more than two folds. NB Insurance (NBIL) nearly maintained the pace with the industry.

Net Profit

It is the major indicator used by both the investors and the companies in order to determine the performance. It is the amount earned by the company after deducting all the expenses. It is the amount that helps the investors to predict the dividend and management to evaluate their performance.

(Note: RBCL is not included in the calculation of industrial growth of net profit)

In the review period, the Net profit of the Non-life Insurance companies surged by 97.96%. 6 out of 14 companies were superior to the industry. United Insurance being in the top of the list, increased its Net Profit by a massive 320.93%. 4 other companies along with NB Insurance and United Insurance earned a net profit more than double of its corresponding quarter of last FY.

Earnings per Share (EPS)

Earnings per share (EPS) is the portion of the company’s profit allocated to each outstanding shares of common stock. It serves as an indicator of company’s profitability. It is out of which the investors can estimate their dividend.

(Note: RBCL is not included in the calculation of industrial growth of net profit)

In the review period, the Net profit of the Non-life Insurance companies surged by 97.96%. 6 out of 14 companies were superior to the industry. United Insurance being in the top of the list, increased its Net Profit by a massive 320.93%. 4 other companies along with NB Insurance and United Insurance earned a net profit more than double of its corresponding quarter of last FY.

Earnings per Share (EPS)

Earnings per share (EPS) is the portion of the company’s profit allocated to each outstanding shares of common stock. It serves as an indicator of company’s profitability. It is out of which the investors can estimate their dividend.

(Note: RBCL is not included in the calculation of industrial EPS)

As of 2nd quater, the EPS of the Insurance industry is Rs 31.20 per share, which rose by 57.69% in last 1 year. 5 out of 14 companies has shown a growth more than the Industry. United Insurance (UIC) made it to the top of the list, by making an enormous growth of 250.78%. Its EPS now stands at Rs 25.96. Companies like Everest Insurance (EIC), NB Insurance (NBIL) and Lumbini General (LGIL) have doubled their EPS. However, companies like Shikhar Insurance (SICL) and Himalayan General Insurance (HGI) have shown a drop in their Per Share Earnings. RBCL has an EPS of Rs 420.50.

Net Worth Per Share

Net worth is the amount by which assets exceed liabilities. It is the portion of core capital for each issued shares of the company. A consistent increase in net worth indicates good financial health; conversely, net worth may be depleted by annual operating losses or a substantial decrease in asset values relative to liabilities. Net worth is also known as book value or shareholders' equity.

(Note: RBCL is not included in the calculation of industrial net worth)

(Note: RBCL is not included in the calculation of industrial EPS)

As of 2nd quater, the EPS of the Insurance industry is Rs 31.20 per share, which rose by 57.69% in last 1 year. 5 out of 14 companies has shown a growth more than the Industry. United Insurance (UIC) made it to the top of the list, by making an enormous growth of 250.78%. Its EPS now stands at Rs 25.96. Companies like Everest Insurance (EIC), NB Insurance (NBIL) and Lumbini General (LGIL) have doubled their EPS. However, companies like Shikhar Insurance (SICL) and Himalayan General Insurance (HGI) have shown a drop in their Per Share Earnings. RBCL has an EPS of Rs 420.50.

Net Worth Per Share

Net worth is the amount by which assets exceed liabilities. It is the portion of core capital for each issued shares of the company. A consistent increase in net worth indicates good financial health; conversely, net worth may be depleted by annual operating losses or a substantial decrease in asset values relative to liabilities. Net worth is also known as book value or shareholders' equity.

(Note: RBCL is not included in the calculation of industrial net worth)

In the review period, the net worth of the insurance industry has hiked by 5.53%. The net worth of the industry is Rs 217.33. 6 out of 14 companies have shown a growth more than the industry. NB Insurance has shown a tremendous increase of 54% in the net worth. It was then followed by Everest Insurance, United Insurance and Neco Insurance. Lumbini General Insurance (LGIL) and Prudential Insurance (PICL) have remained above the industry with a growth of 11.51% and 17.23%. 6 companies have got their net worth decreased, Shikhar Insurance being at the bottom. Everest Insurance has the highest net worth of Rs 412.51 per share.

P/E Ratio

P/E Ratio signals how much an investor is willing to pay for a rupees earnings of the company. As such, a stock with a high P/E ratio is better for short benefit. P/E ratio may depend upon the industry. However, higher P/E ratio might signal that the stock price is inflated in proportion to its earnings and is risky to buy. Short-term investors might benefit from this heightened market price, but it is risky.

Diluted EPS was used in the calculation in order to find the appropriate PE ratio.

In the review period, the net worth of the insurance industry has hiked by 5.53%. The net worth of the industry is Rs 217.33. 6 out of 14 companies have shown a growth more than the industry. NB Insurance has shown a tremendous increase of 54% in the net worth. It was then followed by Everest Insurance, United Insurance and Neco Insurance. Lumbini General Insurance (LGIL) and Prudential Insurance (PICL) have remained above the industry with a growth of 11.51% and 17.23%. 6 companies have got their net worth decreased, Shikhar Insurance being at the bottom. Everest Insurance has the highest net worth of Rs 412.51 per share.

P/E Ratio

P/E Ratio signals how much an investor is willing to pay for a rupees earnings of the company. As such, a stock with a high P/E ratio is better for short benefit. P/E ratio may depend upon the industry. However, higher P/E ratio might signal that the stock price is inflated in proportion to its earnings and is risky to buy. Short-term investors might benefit from this heightened market price, but it is risky.

Diluted EPS was used in the calculation in order to find the appropriate PE ratio.

(Note: RBCL is not included in the calculation of industrial PE ratio)

In the review period, the P/E ratio of the insurance industry is 39.79 times. 7 out of 14 companies have their P/E ratio less than the industry. Nepal Insurance (NICL) has the lowest PE ratio of 27.95 times. It is followed by Lumbini General Insurance (LGIL) and Siddhartha Insurance (SIL). Prabhu Insurance (PRIN) had the P/E ratio of 66.53 times. RBCL has a P/E ratio of 25.96 times

Price to Book value Ratio (PB Ratio)

The price-to-book ratio (P/B Ratio) is a ratio used to compare a stock's market value to its book value. It is calculated by dividing the current closing price of the stock by the latest quarter's book value per share. It is a ratio highly used by the long term investors.

(Note: RBCL is not included in the calculation of industrial PE ratio)

In the review period, the P/E ratio of the insurance industry is 39.79 times. 7 out of 14 companies have their P/E ratio less than the industry. Nepal Insurance (NICL) has the lowest PE ratio of 27.95 times. It is followed by Lumbini General Insurance (LGIL) and Siddhartha Insurance (SIL). Prabhu Insurance (PRIN) had the P/E ratio of 66.53 times. RBCL has a P/E ratio of 25.96 times

Price to Book value Ratio (PB Ratio)

The price-to-book ratio (P/B Ratio) is a ratio used to compare a stock's market value to its book value. It is calculated by dividing the current closing price of the stock by the latest quarter's book value per share. It is a ratio highly used by the long term investors.

![pbbbb[38]](https://content.sharesansar.com/photos/wp-content/uploads/2017/03/pbbbb38.jpg) (Note: RBCL is not included in the calculation of industrial PB ratio)

It is seen that the insurance industry has a PB ratio of 5.09 times. 6 out of 14 companies have PB ratio less than the industry. Everest Insurance has the lowest PB ratio of 2.77 times. It was followed by Siddhartha Insurance, NLG Insurance and Sagarmatha Insurance. Lumbini General Insurance (LGIL) and United Insurance (UIC) have a PB ratio slightly less than the industry. Prabhu Insurance (PRIN) had the highest PB ratio of 9.68 times. RBCL has a PB ratio of 4.29 times.

(Note: RBCL is not included in the calculation of industrial PB ratio)

It is seen that the insurance industry has a PB ratio of 5.09 times. 6 out of 14 companies have PB ratio less than the industry. Everest Insurance has the lowest PB ratio of 2.77 times. It was followed by Siddhartha Insurance, NLG Insurance and Sagarmatha Insurance. Lumbini General Insurance (LGIL) and United Insurance (UIC) have a PB ratio slightly less than the industry. Prabhu Insurance (PRIN) had the highest PB ratio of 9.68 times. RBCL has a PB ratio of 4.29 times.

- Paid-up Capital

- Reserve and Surplus

- Insurance Fund

- Net Profit

- Earnings per share (EPS)

- Net Worth

- P/E ratio

- P/B ratio

In the review period, the non-life insurance companies has hiked the capital by 28.66%. 6 companies were able to grow it more than the industry. Shikhar Insurance has the highest growth in the paid-up capital. After the issuance of FPO and bonus shares of 60%, its capital has almost doubled. It currently has a capital of Rs 81.76 crore. It is then followed by Premier Insurance with a growth of 56%. Lumbini General Insurance grew its capital by 33.62%. 2 Companies had a stagnant capital and it being the same as the last year.

Reserve and Surplus

Huge amount of reserve shows that the company is fundamentally strong and can sustain even in the bad times. The companies can use the reserve and surplus for various purposes including the issuance of bonus shares to its shareholders. Higher growth in the reserve indicates the company will have a high net worth.

In the review period, the industry amplified the reserve by 3.02%. 7 out of 15 companies had a growth more than the industry. Prudential Insurance (PICL) had the highest growth of 79.69.81%, which was closely followed by Lumbini General Insurance (LGIL) with 65.81% .

The reserve of Premier Insurance Company (PIC) dropped by massive 63.96%, 7 other companies along with Premier Insurance (PIC) had a drop in the reserve and surplus. This indicates the company provided a dividend out of its accumulated profits (Reserve and Surplus).

Insurance Fund

A company has to maintain this fund to take higher risk. 50% of net profit earned is kept aside for insurance fund and cannot be used to issue dividends to the shareholders. However, this is still the shareholders’ equity. Higher insurance fund enables the company to take higher risks and ultimately helps the company to maximize profit and shareholders’ return.

In the review period, the Insurance Fund of the industry rose by 55.18%. 6 out of 15 companies successfully performed better than the industry. Premier Insurance company (PIC) being top in the list, rose its Insurance fund by massive 131.53%. United Insurance and Everest Insurance Company (EIC) increased to more than two folds. NB Insurance (NBIL) nearly maintained the pace with the industry.

Net Profit

It is the major indicator used by both the investors and the companies in order to determine the performance. It is the amount earned by the company after deducting all the expenses. It is the amount that helps the investors to predict the dividend and management to evaluate their performance.

(Note: RBCL is not included in the calculation of industrial growth of net profit)

In the review period, the Net profit of the Non-life Insurance companies surged by 97.96%. 6 out of 14 companies were superior to the industry. United Insurance being in the top of the list, increased its Net Profit by a massive 320.93%. 4 other companies along with NB Insurance and United Insurance earned a net profit more than double of its corresponding quarter of last FY.

Earnings per Share (EPS)

Earnings per share (EPS) is the portion of the company’s profit allocated to each outstanding shares of common stock. It serves as an indicator of company’s profitability. It is out of which the investors can estimate their dividend.

(Note: RBCL is not included in the calculation of industrial EPS)

As of 2nd quater, the EPS of the Insurance industry is Rs 31.20 per share, which rose by 57.69% in last 1 year. 5 out of 14 companies has shown a growth more than the Industry. United Insurance (UIC) made it to the top of the list, by making an enormous growth of 250.78%. Its EPS now stands at Rs 25.96. Companies like Everest Insurance (EIC), NB Insurance (NBIL) and Lumbini General (LGIL) have doubled their EPS. However, companies like Shikhar Insurance (SICL) and Himalayan General Insurance (HGI) have shown a drop in their Per Share Earnings. RBCL has an EPS of Rs 420.50.

Net Worth Per Share

Net worth is the amount by which assets exceed liabilities. It is the portion of core capital for each issued shares of the company. A consistent increase in net worth indicates good financial health; conversely, net worth may be depleted by annual operating losses or a substantial decrease in asset values relative to liabilities. Net worth is also known as book value or shareholders' equity.

(Note: RBCL is not included in the calculation of industrial net worth)

In the review period, the net worth of the insurance industry has hiked by 5.53%. The net worth of the industry is Rs 217.33. 6 out of 14 companies have shown a growth more than the industry. NB Insurance has shown a tremendous increase of 54% in the net worth. It was then followed by Everest Insurance, United Insurance and Neco Insurance. Lumbini General Insurance (LGIL) and Prudential Insurance (PICL) have remained above the industry with a growth of 11.51% and 17.23%. 6 companies have got their net worth decreased, Shikhar Insurance being at the bottom. Everest Insurance has the highest net worth of Rs 412.51 per share.

P/E Ratio

P/E Ratio signals how much an investor is willing to pay for a rupees earnings of the company. As such, a stock with a high P/E ratio is better for short benefit. P/E ratio may depend upon the industry. However, higher P/E ratio might signal that the stock price is inflated in proportion to its earnings and is risky to buy. Short-term investors might benefit from this heightened market price, but it is risky.

Diluted EPS was used in the calculation in order to find the appropriate PE ratio.

(Note: RBCL is not included in the calculation of industrial PE ratio)

In the review period, the P/E ratio of the insurance industry is 39.79 times. 7 out of 14 companies have their P/E ratio less than the industry. Nepal Insurance (NICL) has the lowest PE ratio of 27.95 times. It is followed by Lumbini General Insurance (LGIL) and Siddhartha Insurance (SIL). Prabhu Insurance (PRIN) had the P/E ratio of 66.53 times. RBCL has a P/E ratio of 25.96 times

Price to Book value Ratio (PB Ratio)

The price-to-book ratio (P/B Ratio) is a ratio used to compare a stock's market value to its book value. It is calculated by dividing the current closing price of the stock by the latest quarter's book value per share. It is a ratio highly used by the long term investors.

(Note: RBCL is not included in the calculation of industrial PB ratio)

It is seen that the insurance industry has a PB ratio of 5.09 times. 6 out of 14 companies have PB ratio less than the industry. Everest Insurance has the lowest PB ratio of 2.77 times. It was followed by Siddhartha Insurance, NLG Insurance and Sagarmatha Insurance. Lumbini General Insurance (LGIL) and United Insurance (UIC) have a PB ratio slightly less than the industry. Prabhu Insurance (PRIN) had the highest PB ratio of 9.68 times. RBCL has a PB ratio of 4.29 times.

.png)